DISCLAIMER: The opinions expressed by the author are personal and do not reflect those of the institution that employs him.

Abstract :

- Benoît Coeuré (ECB) recently stated that central banks will have to play a role in the fight against climate change by adapting their monetary policy to physical and transition risks.

- The financial sector will be affected by the ecological transition mainly because of its exposure to economic actors (operating in carbon-intensive sectors) whose investments would become insufficiently profitable or whose business model would be challenged by the innovations required in a context of transition.

- The ECB’s unconventional policies, in particular the corporate bond purchase program, have favored carbon-intensive sectors due to the influence of the existing economic structure, the choice of asset classes, and asset eligibility criteria.

- Despite the difficulties associated with their mandate and operational framework, Benoît Coeuré’s speech highlights the need for central banks to take action on climate change (role in developing a regulatory framework that promotes the greening of the financial sector; adaptation of collateral policy; adoption of ESG practices in the management of their own portfolios).

This article reviews the consequences of climate change risks on monetary policy, the effects of unconventional monetary policies on climate change, and the courses of action available to central banks to « green » their monetary policy.

In a speech[i] delivered on November 8 in Berlin at a conference organized by the Bundesbank on green financing, Benoît Coeuré, member of the Executive Board of the European Central Bank (ECB), stated: « Climate change is not a theory. It is a fact. » He went on to say: « While it is widely recognized that environmental externalities should primarily be corrected by effective policies such as taxation, all public authorities, including the ECB, must consider appropriate measures in response to climate change. »

Achieving the objectives of the Paris Agreement requires adjustments in economic policy and, in particular, a reorientation of investments—and therefore capital—to make them compatible with a transition to a low-carbon economic model that is resilient to the consequences of climate change. In this context, the role of monetary policy in financing the ecological transition is the subject of significant debate among economists, in line with the European Climate Finance Pact[ii] presented in March 2018 by climatologist Jean Jouzel, a member of the IPCC, and economist Jean Larrouturou, which proposes to channel the ECB’s money creation towards the energy transition. Indeed, given the independence of the ECB and the pursuit of monetary policy objectives (the first of which is price stability) based on the principle of neutrality, greening the ECB’s monetary policy remains a limited exercise today —which Benoît Coeuré sought to clarify in his speech with a view to suggesting areas for improvement.

In this context, it is useful to revisit:

- The effects of climate change on the conduct of monetary policy, by studying the materialization of physical and transition risks and their consequences for the financial sector;

- The impact of the ECB’s quantitative easing program on the climate; before highlighting; and

- The channels through which central banks participate in financing the fight against climate change.

1) What are the risks of climate change to financial stability?

Climate change can pose a range of risks to financial stability (see BSI Economics note, « Climate change, a systemic challenge for the financial system, « published in May 2018):

- Physical risks, which are the uncertain financial impacts on socio-economic systems and asset portfolios resulting from the effects of extreme weather events and rising average temperatures and sea levels (bearing in mind that the degree of vulnerability to physical risk currently varies significantly across different regions of the world (it is highest in sub-Saharan Africa, Southeast Asia, and China)).

In the event of a delayed adjustment followed by a hard landing of the financial system, the physical costs induced by climate change will be exacerbated (ESRB, 2016). A hard landing remains a plausible scenario today[iii] due to the short-term political cost of the low-carbon transition, the necessary technological advances, the instability of price signals, and the difficulties of international coordination in reducing emissions. The value at risk, which depends on the degree of global warming, is estimated at USD 4.2 trillion in financial assets (EIU, 2015).

- Transition risks, which are uncertain financial impacts resulting in the sudden revaluation of certain assets, or even their collapse (the « Minsky moment »). This revaluation results from the effects of the implementation of a low-carbon economic model on economic agents, particularly in sectors that are overly exposed to global warming or unprofitable in the context of its limitation (transition risks must then be considered within the value chain (suppliers, customers) in which each company operates). These assets are better known as « stranded assets, » i.e., investments or assets that are depreciating in value due to market developments, particularly in the fossil fuel sector; and

- Litigation risks, i.e., the financial consequences of potential legal action seeking to establish liability for climate change.

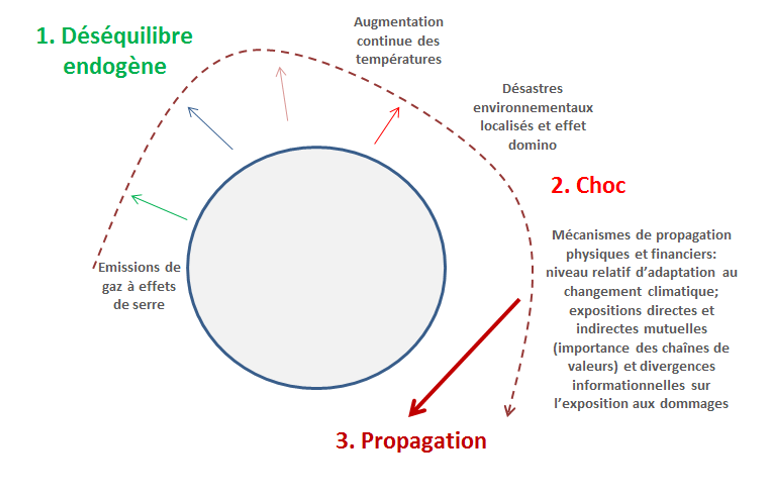

In this sense, Aglietta and Espagne (2016) introduced the concept of systemic climate risk: climate change is generally considered, assuming market efficiency, as a negative externality requiring the introduction of a carbon tax or an emissions trading market. However, the authors highlight the systemic nature of climate change, given its consequences for economies and societies (which are inherently systemic and endogenous) (Weitzman, 2009, 2015[iv]) and the uncertainty surrounding the timing and speed of emissions reductions. According to the authors, these characteristics justify the implementation of specific and appropriate monetary policy and financial regulation, both ex ante andex post.

Figure 1 – The main characteristics of the concept of climate systemic risk

Source: Aglietta and Espagne (2016); BSI Economics

Although these risks appear remote and uncertain at first glance, they are gradually materializing around the world[v] (they are at the heart of Mark Carney’s « tragedy of the horizon » (2015)) and have direct consequences on the need to assess the potential vulnerabilities associated with climate change (ACPR, 2018).

2) What are the effects of climate change on monetary policy strategy?

This section aims to highlight the materialization of the risks described above, particularly in the banking and financial sector, and their impact on the conduct of monetary policy.

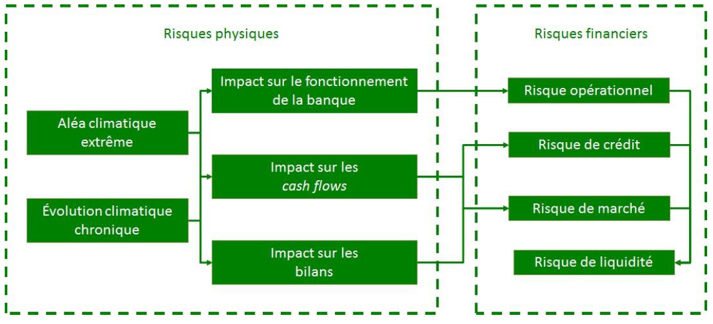

2.1. Physical risks

The consequences of physical risks for the financial sector include the macroeconomic consequences of the materialization of these risks and the exposure of banking institutions and investment funds to vulnerable counterparties. Although the negative impact of natural disasters on short-term economic growth has been widely proven, academic literature on the long-term effects of these same disasters remains limited at this stage and faces methodological difficulties, particularly in relation to the construction of an appropriate counterfactual (Cavallo and Noy, 2010).

However, there are several transmission channels, in particular the deterioration of the financial situation of households and non-financial companies in sectors directly linked to land and biosphere use (agriculture and food industry, chemical industry, mineral extraction, etc.) and other sectors dependent on raw materials (real estate, construction, transport). This deterioration can be explained by several factors: fluctuations in supply and demand, reduced efficiency and performance of physical capital, the need for additional investment, higher operating and maintenance costs, as well as asset depreciation and the weakening of the financial balance sheets of the companies concerned.

The banking sector also remains subject to operational risks resulting from extreme weather events. In particular, Dell et al. (2014) explained the impact of climate change on the growth potential of the labor force due to lower labor productivity resulting from the decline in the physical and cognitive performance of human capital.In addition, Stern (2013) highlighted the reduction in the rate of productive capital accumulation due to climate change (due to long-term damage to capital and land), resulting in a lower rate of growth in total factor productivity.

The indirect effects of physical risks on the financial sector remain dependent on the presence or absence of insurance coverage for losses(Batten et al. 2016). For insured losses, their spread to bank balance sheets is closely linked to the financial strength of the insurance sector. Uninsured losses, on the other hand, lead to a deterioration in borrowers’ financial situation, an increase in their probability of default and therefore a credit risk for exposed banking institutions. Banks are also exposed to market risk (i.e., a sharp decline in the value of securities held in their portfolios) and liquidity risk (i.e., following a possible reassessment of the quality of the balance sheet by investors) in more extreme cases (ACPR, 2018).

Figure 2 – Mechanisms for the transmission of physical risks to the banking sector

Source: French Treasury and ACPR (2018)

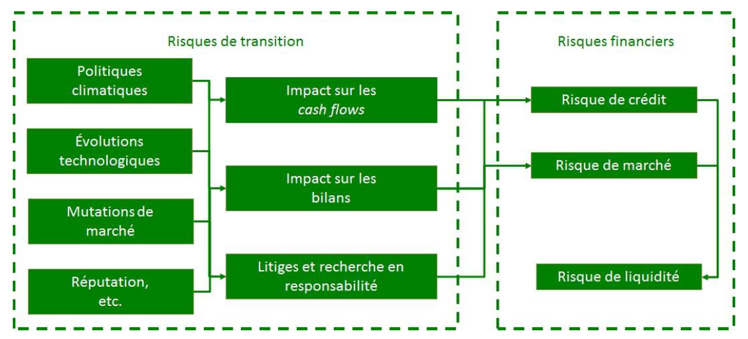

2.2. Transition risks

In order to limit the rise in temperatures to 2°C, approximately 35% of current oil reserves, 50% of gas reserves, and nearly 90% of coal reserves would be unusable (McGlade and Ewins (2015)). The implementation of national low-carbon transition strategies by a growing number of countries with a view to reducing their emissions (and the resulting reorganization of certain activities) thus has significant consequences for fossil fuel producers (i.e., potentialloss of revenue) and for the value of assets associated with the use and exploitation of these resources ( » stranded assets « )[vi]. Investment projects aimed at developing and exploiting these resources would also be likely, in a decarbonization scenario, to present significant risks for the sponsoring companies by not generating economic returns ( » stranded investments « ). Finally, as highlighted by the International Energy Agency (IEA, 2015), uncertainty surrounding the success of technological advances in the energy transition (renewable energies and carbon capture and storage technologies) may give rise to a number of transition risks[vii] (adjustments between supply and demand, efforts to adapt the electricity market, slow technological progress, etc.).

However, the gas and oil industries account for a significant share of the market capitalization of non-financial companies worldwide ($5 trillion in 2014). In this context, banks’ counterparties (non-financial companies and households) are highly exposed to the energy transition process due to the significant impact on energy expenditure, increased operating costs and capital expenditure, and asset depreciation. This exposure is particularly evident in the energy production and processing sectors and among greenhouse gas producers.

The transition can therefore affect bank balance sheets in two ways:

- through carbonpricing (banks’ exposure to carbon-intensive assets); and

- through rapidlyrising energy prices (ESRB, 2016).

Indeed, the fossil fuel and electricity industries are heavily financed by debt, which further exacerbates the impact on financial stability in the event of a sudden revaluation of stranded assets (in the form of debt repricing and credit losses) (Brunnermeier and Schnabel, 2015). Weyzig (2014) estimates that the exposure of the European financial sector (banks, pension funds, insurers) to the fossil fuel industry exceeds $1 trillion. Even in a scenario of gradual transition, the losses for these players could therefore amount to between $350 billion and $400 billion. Furthermore, given the financial system’s exposure to carbon-intensive sectors (other than fossil fuels and electricity), a sharp revaluation of assets could have second-round effects on corporate bond andleveraged loan markets (ESRB, 2016).

Figure 3 – Transmission mechanisms of transition risks to the banking sector

Source: French Treasury and ACPR (2018)

2.3. What are the implications for monetary policy strategy?

Climate change shocks are primarily supply shocks (McKibbin et al. 2017), which are difficult for central banks to counteract given that they pull output and inflation in roughly opposite directions (Coeuré, 2018), increasing price levels (upward pressure on food and energy prices, for example) while significantly reducing production capacity. This type of shock also makes it particularly difficult for central banks to interpretthe output gap and inflationary pressure.

These difficulties are compounded by:

- the difficulty of identifying climate change-related shocks (Coeuré, 2018): what are the causal relationships between a climate event and its economic consequences? Uncertainty about the effects of environmental reforms and the timing of climate events thus leads to a deterioration in the signal-to-noise ratio; and

- the impact of climate change on the distribution of shocks and their persistence (with consequences for the production/inflation trade-off to be found).

3) What has been the impact of the ECB’s quantitative easing on the fight against climate change?

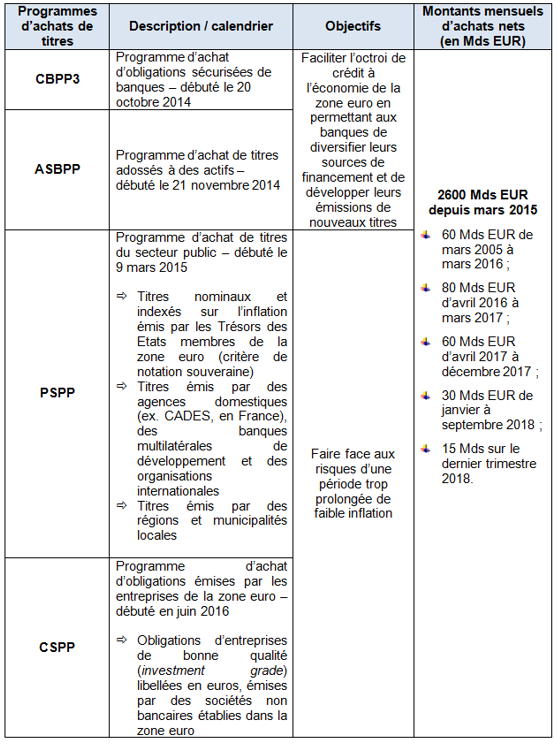

To examine the role of monetary policy in combating climate change, we need to look at the impact of recent European Central Bank policies on the financing of the fight against climate change, in particular the policy of purchasing securities (Quantitative Easing – QE ) aimed at addressing the risks of an overly prolonged period of low inflation and signaling an abandonment of the separation between monetary stability and financial stability objectives (see PSPP and CSPP programs described below).

Figure 4 – Securities purchase policies by the ECB and the Eurosystem since 2014

Source: Banque de France, BSI Economics

The ECB’s securities purchase policy has had a significant impact on the financing of the fight against climate change.

3.1) Influence of the existing structure of economies, the choice of asset classes, and central bank eligibility criteria on the environmental impact of asset purchase programs

Matikainen et al. (2017) pointed out that, in theory, QE is supposed to act as a lever on the economy as a whole. According to the hypothesis of liquid and efficient markets, asset purchases by a central bank should lead to a rebalancing of investor portfolios, thereby increasing asset prices and reducing borrowing costs, thus encouraging debt issuance, with an upward effect on investment, inflation, and economic growth.

However, given market frictions and the lack of substitutability between assets, the ECB’s QE would have significant sectoral effects. The authors have highlighted the environmental consequences of the asset classes chosen by central banks (sovereign bonds, covered bonds, asset-backed securities), despite the principle of neutrality followed by the ECB ( which aims to limit the potentially distorting effects of purchases on the functioning of financial markets, while allowing monetary stimulus to be transmitted to the economy).

The environmental impact differs depending on the asset class:

- for purchases of sovereign bonds, it depends on the ability of governments to support the ecological transition. For purchases of bonds issued by multilateral development banks, it depends on the environmental objectives of lending decisions.

- For purchases of equities through listed index funds (ETFs) ( Bank of Japan program), the impact depends heavily on the sectoral distribution of the indices and their carbon intensity.

- For purchases of asset-backed securities (ABS), legal constraints governing the issuance of covered bonds limit, for example, the possibility of granting loans to companies specializing in renewable energy, while green ABS are currently not eligible under the ECB’s collateral eligibility criteria.

- As for purchases of high-quality corporate bonds, academic studies have shown that they reflect the non-financial corporate bond market, which is itself particularly oriented towards high-carbon sectors (compared to the average carbon intensity of European non-financial companies), particularly utilities (gas, electricity, etc.), which accounts for the largest share of assets purchased by the ECB and the Bank of England.

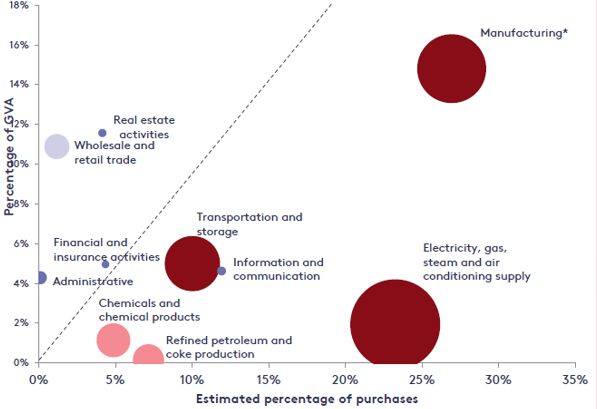

The study by Matikainen et al. (2017) thus showed that the ECB’s CSPP program (corporate bonds) has largely favored carbon-intensive economic sectors whose contribution to the gross value added of the euro area[xii] is insignificant (with the exception of the manufacturing sector, which has high carbon intensity and a high contribution to gross value added). This effect is largely due to the ECB’s asset eligibility criteria[xiii], in particular: (i) limitations on the maturity of securities (minimum residual maturity of 6 months and maximum of 31 years at the time of purchase by the central bank); and (ii) the » investment grade » status of securities (which companies specializing in renewable energy do not have).

Figure 5 – ECB CSPP purchase program – Importance of assets in terms of contribution to euro area gross value added and carbon intensity

Source: Matikainen et al. (2017)

The size of the bubbles indicates the relative contribution of different sectors to greenhouse gas emissions in euro area countries. The colors indicate the most carbon-intensive sectors (red) and the least carbon-intensive sectors (light blue). Note that the « Manufacturing » category does not include the oil and chemical industries, which are shown separately in the graph.

In this regard, it should be noted that Benoît Coeuré acknowledged in his November 2018 speech that the CSPP has favored carbon-intensive economic sectors, while pointing out that nearly 80% of the ECB’s total net purchases since 2015 remain in the form of securities issued by governments and their agencies (i.e., the PSPP program).

Furthermore, it is important to note that despite the absence of an explicit environmental objective in the conduct of asset purchase programs, the ECB has acquired green bonds under the CSPP and PSPP[xiv]. As such, the Eurosystem holds around 20% of the outstanding amount of corporate green bonds eligible for the CSPP (€31 billion): green bonds thus represent around 4% of the total securities eligible for the CSPP, and their yield spread has steadily narrowed since 2016. As for the PSPP, the Eurosystem has purchased green bonds issued by sovereign issuers, agencies, and supranational institutions since the program began: however, the volume of eligible green bonds issued by these public entities remains relatively low (less than 1%) compared to all securities eligible for the PSPP. Furthermore, although the amount of green bonds held by the Eurosystem remains relatively low, the Banque de France has pointed out that through its purchases, the Eurosystem has lowered green bond yields and encouraged their issuance by non-financial companies ( Economic Bulletin No. 7 – 2018).

3.2) Influence of the ECB’s asset purchase programs on the financing of the European Investment Bank (EIB)

A study by Michel Lepetit (2017) highlighted the role of the Public Sector Purchase Program (PSPP) in financing the EIB (the world’s leading multilateral financial institution in terms of lending and borrowing volume and one of the institutions eligible for this program). It should be noted that the EIB is now a major player in financing the fight against climate change[xv]. The author’s estimates of the outstanding amount of EIB bonds purchased by the ECB and the climate share of EIB operations lead to the conclusion that in 2017, the ECB would refinance (i) directly and indirectly climate-friendly actions via the EIB to the tune of €15 billion and (ii) directly EIB « climate-responsible bonds » for more than €2 billion.

These factors thus show the more or less direct consequences of the ECB’s monetary policy—and, a fortiori, that of the world’s major central banks (Fed, BoE, Bank of Japan)—on the fight against climate change. However, in view of the gradual normalization of monetary policy in the eurozone recently described by the Governor of the Banque de France in a speech delivered on November 19, 2018, it remains important to examine the extent to which it is possible to green its implementation.

4) How can monetary policy implementation be made greener?

4.1) Benoît Coeuré’s proposals

It should be remembered that the ECB’s monetary policy is guided by European texts (Article 127(1) of the TFEU and Article 3 of the TEU), which state in particular that the European Union is working towards the sustainable development of Europe, based on a high level of protection and improvement of the quality of the environment. It is on the basis of the founding texts of the European Union that central regulators point out that the objective of monetary policy is not to achieve sectoral objectives but the macroeconomic objective of price stability, especially since central banks do not have a clear informational advantage over private agents when it comes to resource allocation[xix].

Despite these limitations (with which a number of economists disagree), Benoît Coeuré highlighted several ways to strengthen the role of monetary policy in financing the fight against climate change in his November 2018 speech:

- The ECB can contribute to defining the regulatory framework aimed at strengthening the role of the financial sector in the low-carbon transition, in the context of (i) the implementation of the European Commission’s Action Plan for Sustainable Finance (work on transparency of information on carbon emissions; introduction of climate stress tests; revision of credit rating methodologies); (ii) the work of the Central Banks and Supervisors Network for Greening the Financial System[xxi]; and (iii) the work of the Financial Stability Board’s Task Force on Climate-related Financial Disclosure on the disclosure of climate-related financial information. The implementation of these regulatory measures will be reflected in the ECB’s collateral policy(i.e., the eligibility of securities in terms of climate risk pricing by markets and credit rating agencies).

- The ECB may adopt « best practices » within its own activities, particularly portfolios without monetary policy objectives, namely:

- the pension fund portfolio, for which the ECB pursues a sustainable investment policy (sectoral exclusion of certain assets; proxy voting guidelines for managers who have signed the UN Principles for Responsible Investment[xxiv]); and

- the equity portfolio, for which Benoît Coeuré points out that the ECB has begun work to include environmental criteria (at a minimum, the purchase of green bonds).

- For portfolios held for monetary policy purposes, Benoît Coeuré highlights in his speech the ECB’s principle of neutrality and the objective of price stability, while emphasizing that, as part of the PSPP and CSPP asset purchase programs, the ECB has purchased green bonds (€48 billion and €31 billion, respectively). In his speech, he also stated: « The principle of market neutrality does not, however, preclude support for environmental objectives, » paving the way for greater consideration of environmental objectives as part of the gradual normalization of the ECB’s monetary policy.

- 4.2) What about the other proposals?

Nevertheless, several avenues for deepening the contribution of central banks to the fight against climate change have been proposed in recent years.

Of particular note is the possibility of « green »quantitative easing (Campiglio et al., 2016; Dafernos et al., 2017), whose asset eligibility criteria would exclude high-carbon financial assets. However, this proposal remains controversial given the high risk of green assets and the resulting reduction in the universe of assets that can be acquired. Giving greater weight to purchases of green bonds issued by supranational institutions under the PSPP program remains a possible alternative. Other avenues (Matikainen et al. 2017), in line with the TCFD recommendations, concern greater transparency on the part of central banks in terms of asset eligibility criteria and the consideration of climate-related risks.

On the other hand, taking climate change risks into account in the ECB’s collateral policy and portfolio management policy (particularly for financial stability purposes) is a key factor. Mésonnier et al. (2017)[xxvii] have shown that collateral eligibility can influence banks’ lending supply due to their demand for collateral used as security: loans to eligible companies can then benefit from a relative reduction in interest rates (« eligibility discount »). In addition, the inclusion of an asset in the list of eligible assets may encourage financial institutions to acquire these assets, which would then benefit from more favorable financing conditions (Van Bekkum et al., 2017)[xxviii].

Finally, it should be noted that,beyond unconventional monetary policies, several proposals to strengthen the role of central banks in the fight against climate change have recently been supported in academic literature (Aglietta and Espagne (2018); Guttmann (2018)), to which the Director of Financial Stability at the Banque de France, Laurent Clerc, responded in June 2018[xxix].

Conclusion

Given the risks that climate change poses to financial stability, monetary policy cannot ignore climate change. However, there are still many difficulties in adapting monetary policy and the operational framework of central banks to climate change. These difficulties stem primarily from the independence of central banks and the political acceptability (accountability) of strengthening their action, especially since monetary policy should not be a substitute for strong environmental policies on the part of governments. They also stem from the uncertainty that remains regarding the level of risk of « green » financial assets.

Nevertheless, it is now essential that central banks play a role in developing a financial regulatory framework that promotes the greening of the financial sector, which could have a significant influence on collateral policy. This work complements efforts to deepen understanding of climate risks and their impact on financial stability, as well as to develop a taxonomy of green assets (which will play an important role in the potential adaptation of asset eligibility criteria).

Selective bibliography

- Aglietta, M., Espagne, E., Climate and finance systemic risks, more than an analogy? The climate fragility hypothesis. CEPII Working Paper No. 2016-10, 2016

- Anderson, V., Green Money: Reclaiming Quantitative Easing Money Creation for the Common Good. Green/EFA group in the European Parliament, 2015

- Bank of England, The impact of climate change on the UK insurance sector: a climate change adaptation report by the Prudential Regulation Authority, 2015

- Bank of England, The Bank of England’s response to climate change, Quarterly Bulletin, 2017

- Batten, S., Sowerbutts, R. and Tanaka, M., Let’s Talk about the Weather: the impact of climate change on central banks. Bank of England Staff Working Paper No. 603, 2016

- Bernanke, B S. and Gertler, M., Should Central Banks Respond to Movements in Asset Prices? American Economic Review, 91(2): 253-257, 2001

- Bernanke, B. S., The Taylor Rule: Benchmark for Monetary Policy?, Brookings, 2015

- Bernanke, B. S., Monetary Policy in a new era, Brookings, 2017

- Bowen, A., Dietz, S., The Effects of Climate Change on Financial Stability, with Particular Reference to Sweden, 2016

- Campiglio, E., Beyond carbon pricing: the role of banking and monetary policy in financing the transition to a low-carbon economy. Ecological Economics, 121, 220-230, 2016

- Campiglio, Dafernos, Monnin, Collins, Schotten, Tanaka, Finance and climate change: what role for central banks and regulators?, Nature Climate Change, Volume 8, June 2018

- Carney, M., ‘Resolving the climate paradox.’ Speech, September 22, to the Arthur Burns Memorial Lecture, Berlin, 2016

- Carney, M., ‘Breaking the Tragedy of the Horizon–climate change and financial stability’. Speech, September 29, to Lloyd’s of London, 2015

- Coeuré, B., Monetary Policy and Climate Change, Speech at the conference “Scaling up green finance: the role of central banks”, Berlin, November 8, 2018

- Dafermos, Nikolaidi and Galanis, Climate change, financial stability and monetary policy, Post Keynesian Economics Study Group, Working Paper 1712, September 2017

- Dietz, S., Bowen, A., Dixon, C., Gradwell, P., “Climate value at risk” of global financial assets.’ Nature Climate Change 6 , 676–679, 2016

- European Parliament, The effects and risks of ECB collateral framework changes, July 2018

- European Systemic Risk Board, Too late, too sudden: Transition to a low-carbon economy and systemic risk, No. 6, February 2016

- Lepetit M., Estimation of the impact of the European Central Bank’s Quantitative Easing on the financing of the fight against climate change, The Shift Project, September 20, 2017.

- Matikainen, Campiglio, and Zenghelis, The climate impact of quantitative easing, Grantham Research Institute on Climate Change and the Environment, Policy Paper, May 2017

- McGlade and Ekins, The Geographical Distribution of Fossil Fuels Unused when Limiting Global Warming to 2 Degrees, Nature, 517(7533), 2015

- McKibbin W. A New Climate Strategy Beyond 2012: Lessons from Monetary History,The Singapore Economic Review, Vol. 57, No. 3, 2012

- McKibbin et al., Climate Change and Monetary Policy: Dealing with Disruption, Brookings, November 30, 2017

- Pindyck, R. S., Climate Change Policy: What Do the Models Tell Us?’. Journal of Economic Literature, 51(3):860–872, 2013

- UN Environment Inquiry, On the Role of Central Banks in Enhancing Green Finance. UN Environment Inquiry into the design of a sustainable financial system, Geneva, 2017

- Vinals, J., Olivier Blanchard, Bayoumi, T., Unconventional Monetary Policies – Recent Experience and Prospects. Washington D.C, 2013

- Villeroy de Galhau, F., ‘Climate Change: The Financial Sector and Pathways to 2°C.’ Speech by the Governor of the Banque de France to COP21, Paris, November 30, 2015

- Zenghelis, D., Building 21st century sustainable infrastructure: Time to invest. Policy Brief. London: Grantham Research Institute on Climate Change and the Environment, 2016

[ii]European Climate Finance Pact, available online: https://www.pacte-climat.eu/fr/l-appel-detail/

[iii]It should be noted that there is a high degree of uncertainty surrounding the timing and speed of greenhouse gas emission reductions in line with the provisions of the Paris Agreement. In this regard, the arguments put forward by Stern (2005), who advocated for a rapid start to the implementation of political agreements to combat global warming—allowing for a gradual transition—have been confirmed by Acemoglu et al. (2012), who highlight the virtuous cycle of rapid and gradual intervention on endogenous technical progress and growth, particularly if fiscal policies (such as carbon taxes) are accompanied by adequate support for research and development.

[iv]Weitzman also highlights the thicker tails of the distribution of damage caused (« fat-tailed distribution »).

[v]Coeuré, 2018: » It is fair to say that most weather-related shocks have been short-lived and contained […] As a result, the ECB, in its short history, has never yet been compelled to take action in response to climate-related shocks […] But this may change. Indeed, I would argue that the horizon at which climate change impacts the economy has shortened, warranting a discussion on how it affects the conduct of monetary policy. »

[vi]Reserves that cannot be exploited given the « carbon budget » to be consumed by 2050 in order to stay below a temperature of +2°C (i.e., oil, gas, coal). Their value is therefore likely to depreciate significantly, as will that of companies planning to exploit them. A significant example today is coal in the United States: due to the development of the shale gas industry, the financial prospects of the coal industry have deteriorated significantly, leading to the bankruptcy of these companies.

[vii]According to the ESRB (2016), uncertainty surrounding technological progress in the fields of renewable energy and carbon capture and storage technologies would exacerbate the scenario of a « hard landing » for the financial system.

[viii]In particular, the transport, agriculture, industry, and real estate sectors.

[ix]The reasons whyasset repricing has not yet taken place are difficult to identify: unobservable counterfactuals; credibility of environmental policies; combination of cognitive biases, a certain regulatory culture, and divergent incentives among market participants (Matikainen et al. 2017).

[x]Given institutional investors’ preference for sovereign bonds and investment-grade corporate bonds, the rebalancing towards other asset classes – such as equities – is much less significant in reality.

[xi]This principle of ECB neutrality was highlighted by Jens Weidmann, President of the Bundesbank and Chairman of the Board of Directors of the Bank for International Settlements, in a speech on green bonds delivered on July 13, 2017 (available online: https://www.bis.org/review/r170728c.htm): » Neutrality is an important principle of the Eurosystem’s operational framework. In a monetary union with 19 national financial systems, which differ in various ways, it is important not to favor certain financial instruments over other forms of financing. Any type of privileged treatment would increase national differences in the transmission of our single monetary policy. » See also: Dalbard, Nguyen, August 28, 2018, « QE in practice: what does market neutrality mean? »: https://blocnotesdeleco.banque-france.fr/en/blog-entry/qe-practice-what-does-market-neutrality-mean

The Banque de France noted in its Economic Bulletin (No. 7, 2018) that: « The asset purchase program (APP) aims to promote a sustainable adjustment in the inflation path in line with the ECB’s primary objective of price stability, which is defined as an inflation rate below, but close to, 2% in the medium term. The eligibility criteria for the APP are deliberately broad in order to offer a wide range of securities that can be purchased. This enhances the effectiveness of the program and avoids distortions in specific market segments. The implementation of the APP is governed by the principle of market neutrality and does not discriminate positively or negatively on the basis of environmental or any other criteria. In the specific case of the corporate sector purchase program (CSPP), which aims to further strengthen the transmission of the benefits of asset purchases to the financing conditions of the real economy, purchases of securities issued by non-bank corporations proportionally reflect the market value of all eligible bonds in terms of economic activity sectors or rating groups.

[xii]Gross value added represents the balance of the production account in national accounts (i.e., value of production minus intermediate consumption).

[xiii]See Article 2 of the ECB Decision of June1, 2016 on the implementation of the corporate sector purchase program: https://www.ecb.europa.eu/ecb/legal/pdf/celex_32016d0016_fr_txt.pdf

[xiv]Banque de France Economic Bulletin No. 7 (2018): Green bond purchases under the Eurosystem asset purchase program (De Santis et al., 2018)

[xv]European Investment Bank (EIB), « Financing Climate Action, » 2017: http://www.eib.org/attachments/thematic/climate_action_fr.pdf

[xvi]Villeroy de Galhau F., Speech at the 2018 Paris Europlace International Financial Forum, Tokyo, November 19, 2018: https://www.banque-france.fr/intervention/paris-europlace-forum-financier-international-2018-tokyo-19-novembre-2018. In this speech, the Governor of the Banque de France emphasized that three instruments from the » quartet of unconventional instruments » (excluding net asset purchases) will enable the ECB to continue its monetary stimulus from early 2019, namely: (i) the full reinvestment of the stock of assets acquired in order to maintain favorable liquidity conditions; (ii) maintaining interest rates at their current levels at least until summer 2019; and (iii) considering new liquidity and credit supply operations for banks.

[xvii]Article 127(1) of the Treaty on the Functioning of the European Union states that « the primary objective of the European System of Central Banks shall be to maintain price stability. Without prejudice to the objective of price stability, the European System of Central Banks shall support the general economic policies of the Union, as defined in Article 3 of the Treaty on European Union. »

[xviii]Article 3.3 of the TEU: « The Union shall establish an internal market. It shall work for the sustainable development of Europe based on balanced economic growth and price stability, a highly competitive social market economy, aiming at full employment and social progress, and a high level of protection and improvement of the quality of the environment. It shall promote scientific and technological advance. »

[xix]Villeroy de Galhau F., « Climate change: the financial sector and the path to two degrees, » November 30, 2015: https://www.banque-france.fr/sites/default/files/medias/documents/discours_2015-11-30_cop-21-fvg.pdf

[xx]Such as the signatories of the European Climate Finance Pact cited in the introduction, who would like to see quantitative easing go further by helping to finance the energy transition.

[xxii] Collateral policy refers to the quality of assets that the ECB requires from a commercial bank as collateral for the loan it grants it, as well as the haircut it applies to the value of the asset in the event of counterparty default. The OFCE reviewed the evolution of the ECB’s collateral policy in an article published on July 5, 2018, on its blog: https://www.ofce.sciences-po.fr/blog/la-bce-et-sa-politique-de-collateral/

[xxiii]In this regard, it is worth noting the publication by the Banque de France of a « Responsible Investment Charter » in March 2018: https://www.banque-france.fr/sites/default/files/media/2018/03/13/charte_ir_bdf_vf.pdf

[xxv]The ECB’s own funds portfolio is invested in euro-denominated assets with a view to maximizing returns. It consists of: (i) the invested counterpart of the ECB’s paid-up capital; amounts held on an ad hoc basis in its general reserve fund; and provisions for foreign exchange rate, interest rate and gold price risks.

[xxvi]As for the foreign exchange reserves portfolio, Benoît Coeuré points out that, given its composition and the liquidity and security requirements arising from the portfolio’s objective, there is little room for maneuver in environmental matters.

[xxvii]Mésonnier J-S, O’Donnell C., Toutain O., The Interest of Being Eligible, Banque de France Working Paper Series, No. 636, August 23, 2017.

[xxviii]Van Bekkum (S.), Gabarro (M.) and Irani (R. M.) (2017), “Does a larger menu increase appetite? Collateral eligibility and bank risk-taking, ” working paper.

[xxix]http://www.chair-energy-prosperity.org/wp-content/uploads/2018/01/event2018_monnaie-transition-bas-carbone_clerc.pdf

[xxx]Coeuré, 2018: » More imminently, the ECB will concentrate its efforts on supporting market participants, legislators and standard-setting bodies in identifying the risks emerging from climate change and providing a clear framework to reorient financial flows and reduce such risks. A unified framework is the gravitational force needed to finance the greening of our economy. And it is the preoccupation for central banks themselves to expand the use of ESG criteria in the build-up and management of their own asset portfolios. »