Abstract :

- The U.S. EPU uses the number of articles dealing with economic uncertainty in the press (News Index), tax provisions, and economists’ forecast differences. The France indicator uses only the News Index to measure economic policy uncertainty.

- France is the European country with the highest average uncertainty in Europe since the onset of the financial crisis.

- The construction of the French indicator has its limitations.

- The CAC 40 and the sovereign interest rate may reflect uncertainty in France. However, the causal link between uncertainty and these variables has not been proven.

In a previous article, we saw that the EPU (Economic Policy Uncertainty) measures economic policy uncertainty in the form of an index based on three elements: the number of articles published in the press (News Index), tax provisions, and forecast deviations. Economic policy can be defined as all interventions by public administrations (the State, supranational bodies, local authorities and even central banks) in economic activity to achieve growth and employment objectives.

The indicator for France uses only the News Index, which since 2007 has shown higher average levels of uncertainty than in other European countries. How is this uncertainty measured and what are the possible ways to improve the indicator? To answer this question, we will present the French indicator, its limitations, and the possible reasons for high uncertainty in France, before proposing potential ways to better visualize and estimate levels of economic policy uncertainty.

1. The French indicator: The news index

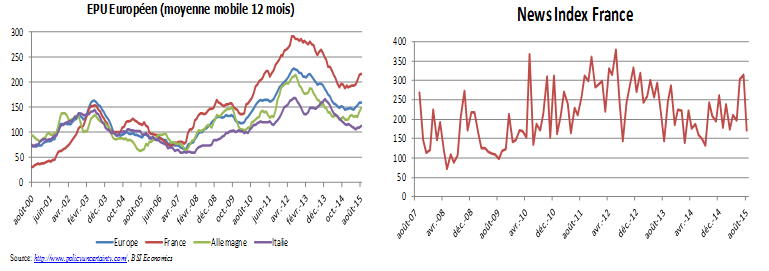

European indicators use only the « News Index » to measure economic uncertainty. In France, this indicator combines the newspapers Le Monde and Le Figaro to quantify economic policy uncertainty. The News Index corresponds to the number of articles published per month in each newspaper in which a combination of the keywords « uncertain » and « uncertainty » appear with « economy » and « economic, » as well as one or more political terms related to political uncertainty. The monthly series from the newspapers are normalized so that they have a standard deviation equal to 1 before 2011, and an average of the different newspapers is calculated for each month to obtain EPU indicators at the European and national levels. These EPU indicators are normalized before 2011 so that their average is equal to 100.

2. The News Index: an imperfect measure of economic uncertainty

The French indicator uses only two newspapers to measure uncertainty, while the US index uses 10[1]. But the French News Index also has specific limitations. Unlike the German and British indicators (the Handelsblatt and the Financial Times), it does not use a newspaper dedicated to economics. Furthermore, Le Figaro is considered a « right-wing » newspaper, and the number of negative articles on economic policy since François Hollande came to power in 2012 may have been higher than in a newspaper considered neutral, without a political slant. The level of uncertainty could be artificially high in France due to the use of negative terms and words, reflecting a certain French pessimism. France regularly ranks at the bottom of tables measuring confidence or optimism. We can take the example of the 2015 « End of Year » international survey conducted by BVA in collaboration with the WIN Gallup network[2] in 65 countries. France ranks63rd in terms of confidence in the economic future. This lack of optimism could translate into more negative articles on the economic situation.

The graph above shows that since 2007, France’s average level of uncertainty has been higher than that of other countries. Between July 2007 and August 2015, France’s index was on average 47 points higher than the European index, 63 points higher than Germany’s and 89 points higher than Italy’s. French uncertainty peaked at 380.2 in June 2012 before beginning to decline, settling at 171.7 in August 2015.

In addition to the limitations outlined above, which may skew the measurement, several factors could explain this high level. The crisis and how it was handled by French governments could be one cause of this uncertainty. The weakness of the stimulus plan (1.4% of GDP, compared with 3.1% for Germany and 6.0% for the United States) and the postponement of deficit reduction targets may have cast doubt on France’s ability to emerge from recession. The French economy contracted by 2.9% in 2009 before growing again in 2010 and 2011 by 2.0% and 2.1% respectively[3]. It has since stagnated since 2012, with average growth of 0.3% from 2012 to 2014. However, Italy and Spain posted average growth rates of -1.7% and -1.0% respectively over the same period, contradicting the argument that weak growth explains the higher level of uncertainty in France. The uncertainty differential could therefore stem from the means rather than the results of economic policies. France has struggled to implement large-scale reforms. The future reform of the labor code, which automatically excludes changes to working hours, the minimum wage, and employment contracts, is one example. Furthermore, the use of Article 49.3 to pass the « Macron » law reflects the uncertainty surrounding the vote on the reforms proposed by the government. This difficulty in reforming does not bode well for greater visibility in the medium term.

3. Potential avenues for improving the measurement of uncertainty: the case of France

We will present two types of solutions that could help to better « visualize » economic uncertainty and quantify it. The first type of solution consists of improving the existing model for the French indicator. The second proposes using the CAC 40 index and the French 10-year sovereign rate to understand the link between uncertainty and economic dynamics.

3.1 Improvements to the construction of the France indicator

The first obvious approach would be to increase the number of newspapers used to calculate the News Index. This would make the measurement more robust by reducing biases related to non-representativeness and political bias. In addition, the French indicator could include Les Echos to measure the occurrence of articles dealing with economic policy uncertainty, as this newspaper is devoted almost exclusively to economic and/or political topics.

The second avenue for improvement is to add other elements in addition to the News Index. The US index is based on three elements (see article « Economic uncertainty: An index to measure it »). The EPU France could adopt these two elements. The first is based on a document that lists the tax provisions set to disappear in the next 10 years. A similar element could be obtained for France by calculating the net amount in euros of tax additions and/or deletions for each year, including temporary tax measures such as the exceptional contribution for high incomes, which is added to income tax and came into effect with the 2015 tax return. Its renewal for the 2016 tax return has not yet been decided. This would make it possible to identify the number of provisions that are set to change and the amount of tax reductions or increases planned for the following year.

The last element uses economists’ forecast differences. For France, we use the Consensus Economics[4] forecasts for inflation (CPI) and budget deficits. This element could be reintegrated into the uncertainty calculation by adding forecast differences for growth rates and/or PMI indices, which are highly correlated with growth. Existing aggregates can be used to refine the measurement of uncertainty or simply to supplement the News Index. These could weight the News Index using the same methodology as the EPU index in the United States.

3.2 Stock market prices as a reflection of uncertainty

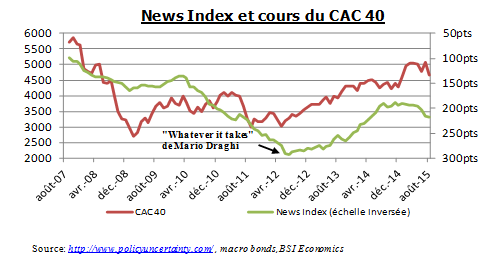

The EPU index and/or the News Index offer an interesting measure of economic policy uncertainty. However, although the CAC 40 is sensitive to variables that have little to do with economic policy in France, it can reflect the prevailing economic uncertainty.

Investors’ skepticism or confidence in this type of event can have an impact on the CAC 40 index. Indeed, investors who believe that the political and geopolitical environment may have an impact on the economy may anticipate low potential for price increases, which would be reflected in the CAC 40 index. The index fell in 2008 due to the financial crisis, then remained between 3,000 and 4,000 points during the rise in uncertainty before beginning to decline in the summer of 2012. This tendency to vary in the opposite direction shows that the stock market index can be a proxy for uncertainty in France, and could therefore support the News Index by weighting the measure of uncertainty.

3.3 The sovereign rate

Initially, the countries on the periphery of the eurozone (Italy, Spain, Portugal, Ireland, and Greece) were hit by a sharp rise in their sovereign borrowing rates. In this scenario, investors, with little visibility on how these countries would emerge from the crisis, reduced their purchases of peripheral debt or demanded higher risk premiums on these securities, causing rates to soar. From the summer of 2012 onwards, France saw its borrowing rates fall. Investors, reassured in part by the ECB’s monetary policy actions, continued to buy French debt. Concerns about a possible French government default subsided, which seems to correspond to a decline in economic uncertainty.

However, it cannot be said that the fall in rates was exclusively due to reassuring announcements by the public authorities, as France has always enjoyed a superior credit rating. Moreover, the downward trend in rates had begun before Mario Draghi’s « whatever it takes » statement. But the announcement of a reduction in US quantitative easing and forward guidance[6] on rate hikes, followed by the ECB’s announcement of quantitative easing, seems to have contributed to the rise in equity markets and the fall in bond yields.

Conclusion

France appears to be experiencing greater uncertainty, with a News Index higher than its European partners. Economic fundamentals may partly explain this difference, but country-specific limitations tend to skew the measurement. The selected newspapers, the difficulties associated with implementing economic reforms, and sluggish growth have contributed to the rise in uncertainty.

The CAC 40 and French borrowing rates may reflect economic uncertainty, and their variations could be incorporated into the UPR to better weight the uncertainty measure. The causal link between uncertainty and these aggregates has not been proven between these indicators and the News Index. Confidence and credit indices or inflation expectations could also be used to supplement and weight the EPU.

References

Scott R. Baker, N. Bloom, and Steven J. Davis (2012 and 2015): « Has Economic Policy Uncertainty Hampered the Recovery? » University of Chicago and Stanford University

Scott R. Baker, N. Bloom, and Steven J. Davis (2015): « Measuring Economic Policy Uncertainty » NBER Working Papers Series

Bloom Nicholas (2009): « Fluctuations in uncertainty » Stanford University, NBER

[1] USA Today, the Miami Herald, the Chicago Tribune, the Washington Post, the Los Angeles Times, the Boston Globe, the San Francisco Chronicle, the Dallas Morning News, the Houston Chronicle, and the Wall Street Journal.

[2] Full methodology and results at http://www.wingia.com/web/files/news/204/file/204.pdf

[3] Source: INSEE, national accounts in volume, base 2010

[4] Consensus Economics is an international company that conducts monthly surveys on numerous economic and financial indicators and aggregates.

[5] To obtain the weighted global index, each element must be normalized by its own standard deviation prior to January 2012. The average value of each element is then calculated using 1/2 for the News Index and 1/6 for the other three measures (the tax provisions indicator and the CPI and budget deficit forecast deviations). For France, ½ is used for the News Index and ¼ for changes in the CAC 40 and the sovereign rate.

[6] A communication tool that guides the expectations of financial market participants on medium- and long-term price developments. Action is not mandatory.