Usefulness of the article: The current coronavirus pandemic is impacting the metals market, including steel, with global demand in decline. This study analyzes all the factors impacting the steel market and the issues facing this industry.

Summary:

- The steel economy is mainly driven by China, which accounts for more than 50% of global production.

- Europe, the traditional cradle of production, is seeing a decline in its steel industry, with the exception of Germany.

- Demand, historically driven by emerging economies, is expected to slow down between now and 2050 due to a global economic slowdown.

- Protectionist measures could encourage the relocation of production.

- Steel is a very energy-intensive industry, with energy prices being a key factor in the sector’s competitiveness.

- The sector, which is a major emitter of greenhouse gases, is undergoing change through the use of greener energy and a desire to combat climate change.

Steel is a metal alloy composed of iron and carbon, to which nickel, chromium, manganese, and molybdenum can be added to modify the alloy’s properties. To date, there are more than 3,500 types of steel in the world, with different technical characteristics.

The second most traded commodity in the world after oil, steel is mainly used in the construction and infrastructure sectors. The added value of this sector to the global economy is estimated at $500 billion, and the industry generates 6.1 million direct jobs. The steel industry, which had a global production of around 1.8 billion tons in 2018, has gradually shifted from Europe to Asia, particularly China, which alone accounts for more than 50% of global production. Cheap labor, lower energy costs, less restrictive environmental standards, and heavy government subsidies explain the decline in European and North American production in favor of the Asian giant.

This highly strategic sector benefits from considerable support from the Chinese authorities, both upstream during manufacturing and downstream in steel-consuming economic sectors. The ultimate goal is to control and influence global production by exporting surpluses not used by Chinese domestic demand. Western powers would then become dependent on their Chinese imports, echoing the current trade war between the United States and China.

In open markets, such as the United States, or closed markets for steel, such as oil-producing countries with an « artificial« steel industry, this sector, which is highly energy-intensive and dependent on fossil fuels, will have to change its energy mix and reduce its greenhouse gas emissions.

1. From unevenly distributed production to an imbalance between supply and demand

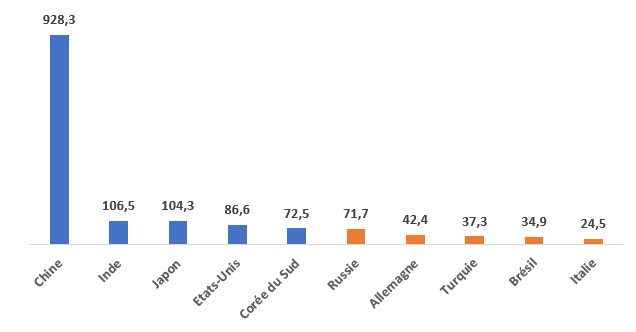

In 2018, global steel production amounted to 1,808 million tons, more than nine times higher than in 1950 (189 Mt). Today, the five largest producers are located almost exclusively in Asia (with the sole exception of the United States), followed by emerging countries (Russia, Brazil, and Turkey) and industrialized European countries (Germany and Italy).

Top 10 steel producers in the world in 2018 (in millions of tons)

Sources: World Steel Association

China alone accounts for 51% of global production, a significant increase from 2000, when the country accounted for only 15% of global production. It is also the world’s leading exporter, with 68.8 million tons exported in 2018. The difference between production and exports is absorbed by the domestic market, which is very dynamic due in particular to the country’s economic growth and subsidies granted to the construction sector.

The United States ranksfourth, but its production is not sufficient to meet domestic demand, and the imported differential comes mainly from Asia or Canada. The US steel sector, which is open and offers little protection from international competition, has slowly declined, which partly explains President Donald Trump’s desire to impose a 25% tax on imported steel. The ultimate goal is to protect the existing industry from the risks of relocation.

While the United States and Russia maintained production levels of around 85 and 70 million tons respectively in 2018, the leading European country, Germany, ranked onlyseventh among global producers with 42.4 million tons in 2018. France ranks only15th in the world with annual production of around 15 million tons, due to a lack of a relevant strategy to preserve its steel industry.

2. A unique supply/demand mechanism, haunted by a crisis of overproduction

Production exceeding demand, putting pressure on producers

The supply/demand mechanism is unique in the steel industry due to production capacity that far exceeds global demand, estimated at 1,712 million tons in 2018, resulting in significant surpluses that put pressure on operators’ profitability. In 2017, it was estimated that around 75% of global production capacity was utilized. These two factors—low capacity utilization and the gap between demand and production— explain the fierce competition that characterizes the steel market.

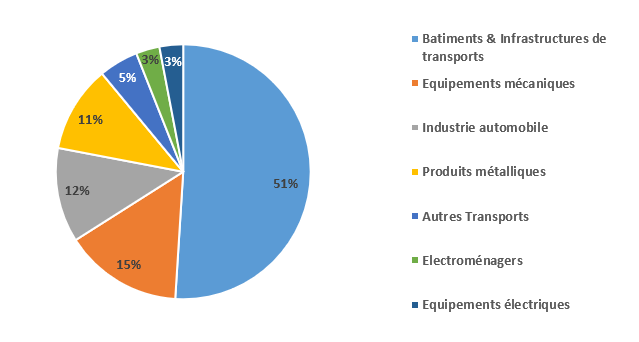

This industry is often considered a barometer for metals due to its use in several industrial activities (mainly in construction). The following graph provides more details on global steel consumption in 2018:

Steel consumption by economic sector in 2018

Sources: World Steel Association

Steel production is particularly sensitive to fluctuations in economic activity. However, between 1950 and 2015, global steel production increased by around 3.4% every five years. Only the period from 1990 to 1995 saw a slight decline (-0.5%), before returning to a growth rate of 6.2% between 2000 and 2005, a figure never before achieved since the post-war period.

However, despite cyclical fluctuations, the long-term trend in global steel production is one of moderate growth.

The Organizationfor Economic Cooperation and Development (OECD) has proposed three scenarios for global steel demand growth:

- A baseline scenario, in which annual demand growth is estimated at 1.4%, reaching a demand of 2 billion tons by 2035;

- A less optimistic scenario, which anticipates a slowdown in global economic activity, with annual demand growth of 1.1%, resulting in total demand of 1.87 billion tons by 2035.

- A radical scenario, which takes into account major technological innovations leading to the widespread use of an alternative to steel, anticipates very low annual demand growth of 0.4%, resulting in global demand of 1.75 billion tons in 2035.

Given the current growth in production compared to future demand estimates, supply is expected to remain higher than demand, which will keep pressure on margins for producers. The sector’s trend toward debt is also a cause for concern: the debt-to-assets ratio, which rose from 25% in 2004 to 41% in 2014, was still 34% in 2017. In addition, one in four companies is indebted to the tune of 50% of its assets or more. Short-term credit is also favored, which can be explained by the difficulty of accessing bank financing and debt financing for operational activities rather than strategic investment decisions, such as R&D. The race for innovation will also play a role in offering high-end products.

An industry dependent on China’s economic health, which practices fierce dumping

The steel industry is therefore highly dependent on the global economic situation, and particularly on dumping by the Chinese authorities. Indeed, the construction and infrastructure sector in China receives significant public subsidies to support its activity, which explains why exports are so low compared to domestic production. Furthermore, China currently only exports low value-added steel, as its industry is not yet capable of producing high-end products, for which the country remains dependent on foreign imports (notably from the European Union, Japan, and South Korea).

In 2016, the Chinese government also changed the VAT on steel products for export: the current system is based on three exemption rates of 5%, 9%, and 13% (compared to 17% VAT for products subject to the general regime). The spirit of this policy is above all to support the export of high value-added products in order to improve the quality (and value) of Chinese steel exports. Chinese state banks offer low-interest loans to public companies in the sector, as well as subsidies to support R&D, compliance with Chinese environmental standards (air pollution control, wastewater treatment, energy savings, etc.), assistance with diversification for companies in the sector, and worker training. This support strategy is beneficial to the sector, in a context where overproduction is weighing on prices. However, the slowdown in Chinese economic growth, which has been evident for several years, could lead to an overproduction crisis.

India has implemented similar measures to support its steel industry. Domestic demand, which has been robust and growing for several years, is expected to continue to reach 230 Mt by 2030. In 2020 and 2021, consumption growth was estimated at 7% per year. In the medium term, India is expected to become the world’s second-largest consumer, thanks to a steadily growing car fleet and the « Make in India » industrial program launched in 2014 by Prime Minister Narendra Modi. It is the country with the best prospects for the steel industry in the world.

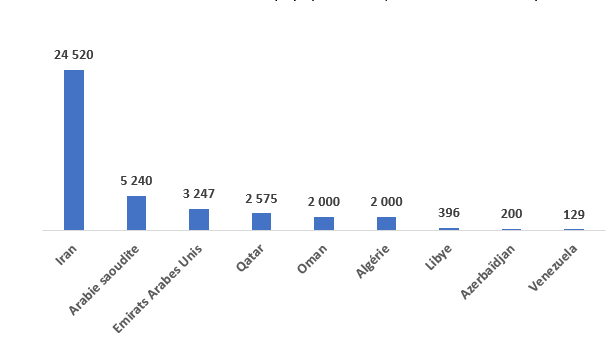

Case study on oil-producing steel-producing countries

Oil-producing countries that have nationalized their oil industry and produce steel have unique characteristics, with « artificial » markets geared towards domestic demand.

The oil industry consumes steel products for onshore and offshore platforms, as well as for pipelines transporting hydrocarbons. Producing countries often impose local manufacturing requirements, forcing manufacturers to open production sites to meet domestic demand. However, these sectors are generally heavily subsidized and not very competitive on the international stage. To ensure the long-term viability of this industry, it will be necessary to move upmarket by encouraging manufacturers to develop high value-added products.

Saudi Arabia is a good example. The Kingdom produces around 5 million tons of steel each year, but the sector benefits from:

- Very cheap energy, thanks to tariffs granted to heavy industry (EUR 0.25/kWh for electricity) and a preferential tariff for hydrocarbons (around USD 6 per barrel for manufacturers, who do not pay the market price);

- A « guaranteed » domestic market for locally produced steel: imported steel that can be produced locally is taxed.

As a result, 65% of Saudi Arabia’s total production is consumed locally and the rest is exported, mainly to neighboring countries (Kuwait, Iraq, Bahrain, etc.). The graph below shows steel production in nine countries that have nationalized their oil industry.

Steel production in nine oil-producing countries (in thousands of tons)

Sources: World Steel Association

The steel industry in oil-producing countries, artificially maintained to meet domestic demand and attempt to diversify the economy, is threatened in the medium term by these countries’ need to move away from oil revenues. They will therefore have to gradually lift energy subsidies and encourage the production of less energy-intensive steel. In fact, 20 to 40% of the cost of producing a ton of steel is attributable to energy (depending on the technology used).

3. A highly energy-intensive sector with constraints related to greenhouse gas emissions

CO₂ emissions still high despite gains made over the last 60 years

Since 1960, the amount of energy required to produce one ton of steel has fallen by 60% thanks to investment in R&D by companies in the sector. With margins under pressure, innovation is therefore key to remaining competitive in a sector threatened by overproduction.

The steel sector accounted for 7.6% of global greenhouse gas emissions in 2018 and 31% of industrial emissions. The production of one ton of steel emits between 1.6 and 2.8 tons of CO₂ equivalent, depending on the technology used and the location of production (environmental standards are stricter in the European Union and North America than in emerging countries).

In addition, this industry remains heavily dependent on fossil fuels to operate. A blast furnace consumes large amounts of electricity, which itself comes from fossil fuels in the main producing countries (the Chinese and Indian electricity sectors remain highly dependent on coal), as well as natural gas.

Large companies in the sector, aware of the environmental impact of their industry, invest an average of 10% of their turnover in developing less energy-intensive production processes.

Since 2003, there has been no further reduction in GHG emissions per ton of steel, prompting manufacturers to look for alternatives to R&D.

To date, producing one ton of steel in France emits five times less GHG than producing the same ton in China, due in particular to France’s highly decarbonized electricity mix.

High energy costs are encouraging manufacturers to opt for less energy-intensive solutions and to recycle steel that has already been used.

To remain competitive, the steel industry is heavily dependent on energy costs, which explains why the United States has been able to maintain high production levels despite strong competition from Asia (the competitive advantage provided by shale gas remains a valuable asset). Competitive energy prices are therefore a determining factor in the investment and site location decisions of steel groups and have an impact on the future of the industry.

Changing the energy mix used in production is a major focus, with the aim of gradually phasing out fossil fuels. Biomethane and hydrogen have been identified as credible alternatives to replace hydrocarbons, but according to estimates by Carbone 4[2], these solutions would only reduce the carbon footprint of steel production by 10%.

The most credible alternative to date is the use of recycled steel, which emits up to four times less GHG than « new » steel. In 2018, 27% of the steel used worldwide came from recycled sources, with disparities between different consumer sectors. The construction industry could use only recycled steel, while the automotive industry has specific requirements for its flat steel, which is difficult to recycle.

According to Carbone 4, aiming for 80% recycled steel by 2050 seems realistic, provided that the collection chain is organized. Production will also need to be reduced by 15% by 2050 compared to 2018 levels in order for the industry to be in line with the objectives of the 2015 Paris Agreement, which aims to limit global warming to well below 2°C by the end of the century.

To date, the solutions recommended above have only been implemented to a limited extent. European countries, having witnessed the decline of their steel industry over the past 50 years, have recently implemented policies aimed at promoting recycling and investing in R&D to move upmarket. Emerging countries still seem reluctant to change their production methods, which, in the long term, could give the European Union a real advantage.

Conclusion

The global steel industry is expected to see moderate growth in demand over the next decade, due in particular to a slowdown in global growth and domestic demand in China. The good health of other markets, such as India, will not be enough to absorb the surplus supply, in a context where the latter will remain higher than demand, driving down prices and thus constraining producers’ margins.

The industry will also have to tackle climate change by drastically reducing its GHG emissions in order to achieve carbon neutrality targets. To achieve this, changes to the energy mix, the development of the recycled steel sector, and a reduction in global production will be necessary.

The steel sector will remain a risky sector for investors, who will have to take environmental standards and energy costs into account when choosing future production sites.

BIBLIOGRAPHY

World Steel Association, Publications Infographics 2018: https://www.worldsteel.org/en/dam/jcr:b5e18bcb-20bc-4d87-b656-dbaabc587fb7/Whole%2520piece_2019.pdf

World Steel Association, Publications Steel Social & Economic Impact 2018: https://www.worldsteel.org/en/dam/jcr:7a759646-a2c6-4f7c-9c54-9710c0eb33e2/Full_steel_impact_infographic.pdf

World Steel Association, Steel Statistics Report 2019: https://www.worldsteel.org/en/dam/jcr:7aa2a95d-448d-4c56-b62b-b2457f067cd9/SSY19%2520concise%2520version.pdf

General Treasury Department, the steel industry in China 2016: https://www.tresor.economie.gouv.fr/Articles/a9ecac25-ada9-47b4-8f86-288f2b0d49cd/files/e976c717-d063-42b0-a590-f6ef871fc70c

General Directorate of the Treasury, Saudi Arabia 2018-2019: https://www.tresor.economie.gouv.fr/Pays/SA/les-notes-du-service-economique-de-riyad

Carbone 4, Case study on the steel sector 2019: http://www.carbone4.com/wp-content/uploads/2019/01/Strate%CC%81gie-dentreprise-analyse-par-sce%CC%81narios-ACIER.pdf

Senate, Senate report on the steel industry in France and worldwide in the21st century 2019: https://www.senat.fr/rap/r18-649-1/r18-649-11.pdf

OECD, Steel Demand Beyond 2030, 2017: https://www.oecd.org/industry/ind/Item_4b_Accenture_Timothy_van_Audenaerde.pdf

EUROFER, the European Steel Association, European Steel in Figures 2019: http://www.eurofer.org/News%26Events/PublicationsLinksList/201907-SteelFigures.pdf

India Brand Equity Fund, Indian Steel Industry Analysis 2019:https://www.ibef.org/industry/steel-presentation

Coface, Economic Studies/Metallurgy 2020: https://www.coface.fr/Etudes-economiques-et-risque-pays/Metallurgie

[1] The term « artificial industry » refers to an industry whose existence is dependent on the presence of another industry (in this case, the oil industry). If the Saudi government did not require steel to be produced locally, the low competitiveness of this industry in the Kingdom would encourage imports.

[2] French consulting firm specializing in energy transition.