Usefulness of the article: This article reviews the motivations behind the adoption of crypto-assets, whether through the introduction of digital currencies by central banks or through the legalization of traditional crypto-assets.

Summary:

- The COVID-19 crisis and the popularity of Bitcoin have increased governments’ interest in crypto-assets.

- Central Bank Digital Currencies (CBDCs) can counter the development of crypto-assets that could undermine national sovereignty.

- Countries with low financial inclusion and high inflation make the most use of « traditional » crypto-assets.

The last two years have seen growing demand for crypto-assets from both the public and institutional investors[1]. This strong demand from institutional investors is reflected in particular by an increase in assets under management[2] and a radical change in the way crypto-assets are perceived.

Alongside these investors, another group of « crypto-optimists » is emerging: governments. Depending on the goals of each government, interest in crypto-assets will vary. It may be a desire for the state to provide national crypto-assets to the public in order to counter the advance of crypto-assets, such as Bitcoin or stablecoins, which would threaten their sovereignty (Central Bank Digital Currencies); but it may also reflect a desire to break free from international currencies such as the US dollar or the euro.

What are the reasons for a state to adopt crypto-assets? Why would a state give its population the opportunity to use crypto-assets legally?

In this article, we will analyze the motivations that could lead a country to take an interest in crypto-assets and/or give them legal status. We will examine the case of Central Bank Digital Currencies (CBDCs) and the adoption of Bitcoin in countries such as El Salvador and the Central African Republic.

1. Central Bank Digital Currencies

A Central Bank Digital Currency (CBDC) is « a digital object that has a value expressed in the currency of the country in which it was issued and a claim on the relevant central bank » (Sveriges Bank, 2021).

Since 2018, many central banks have been studying the design of their own digital currencies. Negative discourse about digital currencies has given way to positive discourse, showing central bankers’ interest in this technology (see Figure 1). With the growing popularity of Bitcoin and distributed ledger technology, as well as the spread of Covid-19, many central banks have launched internal projects to better understand these technologies and their applications (Bank of England, Bank of Canada, Sveriges Bank, People’s Bank of China, etc.).

The first publicly announced study on retail CBDCs was conducted by the Swedish Central Bank (Riksbank/Sveriges Bank), as the use of cash has declined significantly in recent years. This gave rise to the idea of an « e-krona, » a payment instrument offered by the Central Bank and accessible to the public.

The most advanced CBDC project is that of the People’s Bank of China (PBC). It is a digital currency electronic payment (DC/EP) system accessible to the public and foreign visitors in China. Since 2020, with the pandemic, more and more central banks have become interested in CBDCs, leading to a proliferation of projects (Japan, Ecuador, Ukraine, Uruguay, Bahamas, Cambodia, Eastern Caribbean Monetary Union, Korea, European Union, etc.).

Figure 1: Communications on CBDCs

Source: Auer et al. (2020)

1.1 Different types of CBDCs

Before discussing the reasons for using CBDCs, it is necessary to review the different types of CBDCs that are currently available. There are four types of CBDCs (Auer and Boehme, 2020):

• Direct CBDCs: a payment system operated by the central bank, which offers retail services like a retail bank: the central bank records all retail transactions and the digital currency is a public claim against it;

• Hybrid CBDCs: retail banks manage payments and the digital currency remains a claim on the central bank, which also records all transactions and manages a backup infrastructure to restart the payment system in the event of intermediary failure;

• Intermediate CBDCs: an architecture similar to the hybrid CBDC, but in which the central bank only keeps a wholesale ledger (interbank trading only), rather than a central ledger of all retail transactions. Again, the CBDC is a claim on the central bank and private intermediaries execute payments;

• Indirect or synthetic CBCCs: consumers have claims on intermediaries that resemble narrow payment banks[3] and handle all retail payments. These intermediaries must therefore fully guarantee all debts to retail customers with claims on the central bank;

More generally, in the literature, a distinction is made between retail CNBC (the central bank replaces retail banks by managing transactions for individuals) and wholesale CNBC (only interbank transactions).

1.2 Motivations for using CNBCs

Auer et al. (2020) and Lis and Gouveia (2019) identify several motivations for the growing use (or implementation) of CBDCs:

– Level of development and financial inclusion: developed countries may face increased demand for new digital payment methods. In addition, countries with underbanked populations may have a great need for retail CBDCs.

– Institutional quality: countries whose government action is considered effective are more likely to initiate CBI projects. In addition, central banks in jurisdictions with large informal economies also have an interest in creating an environment that is better suited to recording transactions, and therefore in promoting the use of digital currency;

– Digital infrastructure: this point concerns countries that make extensive use of mobile phones or the internet, have a highly developed informal system, and therefore have the desire to replace cash with a more efficient and secure means of payment.

– Capacity for innovation: the population of a country (where the level of innovation is already high) that has the ingenuity and R&D potential to help central banks design a new CBDC ecosystem[4] will be more inclined to demand the introduction of a CBDC.

– Cross-border transactions: there could be CBCCs with a particular international focus (cross-border interbank settlement projects or migrant remittances). CBCCs can improve the functioning of wholesale payment and cross-border transfer systems thanks to distributed ledger technologies that will enable transactions to be carried out securely, transparently, and instantly.

– Strengthening monetary policy instruments: central banks facing the zero lower bound (zero lower bond) could use a universal, anonymous CBDC with an interest rate (positive or negative) to gain room for maneuver in monetary policy.

– Reduce the likelihood and destabilizing impact of banking crises: With CBDCs, central banks provide alternative means of payment to the traditional banking model, which relies primarily on access to financial services in exchange for opening bank accounts and making deposits. As a result, in the event of a banking crisis, households and even businesses using CBDCs would be less vulnerable.

– Public interest in CBI: When public internet searches focus more on CBI and related topics, this may indicate that the public is aware of CBI in general or of their own national central bank’s plans in this area.

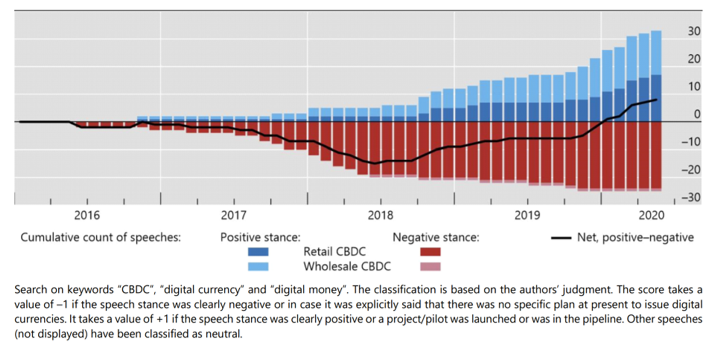

The drivers cited above correspond in particular to the Bank of England’s projects (2020). According to its studies, the introduction of an CBI should increase the availability and facilitate the use of digital money, thereby helping to support monetary policy and financial stability and helping to avoid the risks of new forms of private money creation, such as stablecoins. An CBDC would also help create a resilient, innovative, and competitive payment landscape to meet future payment needs. The CBDC would help address the consequences of declining cash usage and provide a better channel for cross-border payments (see Figure 2).

The Eurosystem, through the European Central Bank (ECB), is not standing idly by in the face of numerous studies on CBDCs. The ECB (2020) lists scenarios that could accelerate the creation of a digital euro:

- The ECB will issue a digital euro if it is proven to promote the digitization of the economy and support the development of innovative European solutions in all types of industries.

- It could also resort to the digital euro if it finds itself in the same situation as the Swedish Central Bank, with a significant decline in the use of cash as a means of payment, or to defend the sovereignty of the euro in the face of the rise of a form of currency other than the euro (central bank money, commercial bank deposits, or electronic money) becoming a credible alternative as a medium of exchange and store of value in the euro area.

- It could issue a digital euro if this is necessary or beneficial from a monetary policy perspective, if it mitigates the likelihood of a cyber incident, natural disaster, pandemic, or other extreme events that could hamper the provision of payment services.

- Finally, it could also opt for a digital euro to reduce the environmental footprint of monetary and payment systems.

Figure 2: The Bank of England’s motivations for creating a CBDC

Source: Bank of England (2020)

2. Use of a crypto-asset such as Bitcoin or a stablecoin

The main motivations for using crypto-assets other than CBDCs are:

- Financial inclusion;

- The share of cross-border transfers in GDP

- Portfolio diversification and inflation hedging;

In this section, we will distinguish between the regulation of crypto-assets and granting these assets legal tender status. Several countries have legalized crypto-assets without making them officially recognized currencies (United States, Canada, France, etc.). To date, only El Salvador and the Central African Republic have authorized Bitcoin as legal tender.

2.1 Financial inclusion

In 2017, approximately 1.7 billion people did not have a bank account, according to Global Findex. In addition, approximately 30% of unbanked adults live in the BRICS countries. The issue of financial inclusion is critical for countries with a highly developed informal sector, limited banking infrastructure, but very high penetration of communication tools such as mobile phones and internet connections. These countries are ideal candidates for the use of crypto-assets, as they are the preferred means of accessing a wide range of financial services.

The widespread use of the internet and mobile technologies in emerging and developing countries has created an environment conducive to interest in crypto-assets among governments and populations. As a result, several emerging or developing countries (Brazil, India, South Africa, Venezuela, Rwanda, Ethiopia, Kenya, etc.) and even developed countries have introduced regulations or various initiatives to promote the adoption of crypto-assets.

For example, in France and other European Union countries, the regulations currently being formalized are based on the recognition of certain players in the crypto-asset market and increased monitoring of exchanges in order to prevent money laundering and terrorist financing.

On March 5, 2020, South Korea passed a law allowing the holding, exchange, and sale of crypto-assets by institutions recognized by the regulator. Finally, we have the examples of El Salvador and the Central African Republic, which have granted Bitcoin legal tender status.

In general, it appears that countries with the most advanced or « forward-thinking » regulations on the adoption of crypto-assets are subject to embargoes or high inflation (Venezuela and the Central African Republic in particular).

According to the IMF (2021): » Crypto-assets are unlikely to gain traction in countries with stable inflation and exchange rates and credible institutions. Households and businesses would have little incentive to price or save in a parallel crypto-asset such as Bitcoin, even if it had legal tender or currency status. Their value is simply too volatile and unrelated to the real economy. »

Finally, the main benefits of digital financial inclusion are: faster and wider dissemination of financial services with equal access to these services for all; and the possibility of economic empowerment for women, young people, and vulnerable sections of society, including small businesses.

2.2 Cross-border transfers

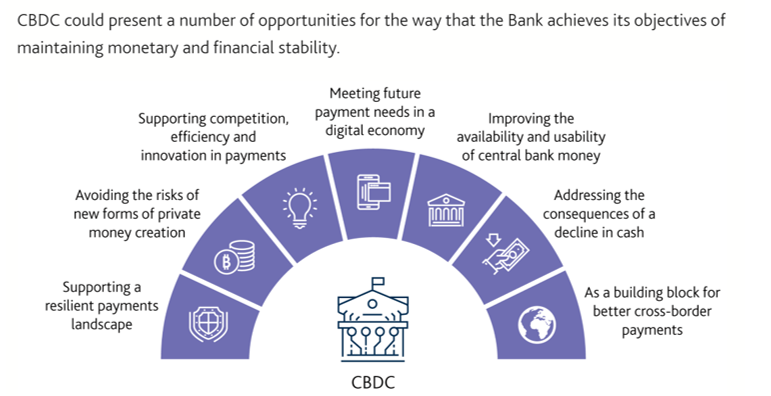

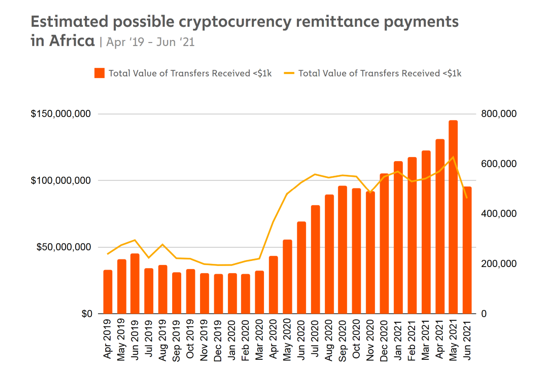

The adoption or regulation of crypto-assets may be accelerated by the desire to increase the share of cross-border transfers in GDP and reduce the costs associated with traditional international remittance services such as Western Union and Orange Money. For example, remittance flows to sub-Saharan Africa amounted to $48 billion in 2019 (see Figure 3). Alongside these large volumes of funds, there are transaction costs, which average 7% of the amount sent (see Figure 4). Furthermore, the funds are not always immediately available (remote withdrawal facilities, public holidays, etc.). The populations of countries that make the most use of cross-border transfers should therefore take a greater interest in crypto-assets, but also and above all in their legal framework.

Chainalysis (2021) shows that peer-to-peer exchange platforms are very popular in Africa compared to other regions studied, as they are a tool for sending funds and engaging in commercial transactions. » Interregional transfers also account for a larger share of the crypto-asset market in Africa than in any other region, with 96% of total transaction volume, compared to 78% for all regions combined. » Crypto-assets are becoming increasingly popular because transfers are instantaneous and inexpensive. For example, in El Salvador, cross-border remittances from one Chivo wallet to another are commission-free, and when there is a difference between the wallets hosting the crypto-assets, the commission is 1%.

Figure 5: Estimated value of cross-border transfers sent in crypto assets in Africa.

Source: Chainalysis (2021)

2.3 Portfolio diversification and inflation hedging

The numerous economic crises that have occurred since the birth of Bitcoin have raised questions about the ability of crypto-assets to serve as safe-haven assets. During the 2012 sovereign debt crisis in the eurozone and the post-2013 crisis in Venezuela, crypto-assets were highly sought after, contributing to the rise in Bitcoin prices between 2013 and 2017.

During the 2012 crisis in Italy and Spain, for example, the number of downloads of apps for tracking Bitcoin prices exploded in 2013 and 2015, propelling these apps to the top of the Playstore and Apple store download charts. With regard to the Cypriot crisis of 2012-2013, the announcement of a tax on bank accounts and capital controls contributed to the peak in Bitcoin prices in 2013. In Greece, the main crypto-asset exchange platform, BTCGreece, was forced to ration its customers’ daily Bitcoin purchases to $250 (compared to the usual $1,000). The number of accounts opened per day had risen by more than 600%, with an average of 150 accounts opened every day[13]. Crypto-assets could therefore be seen by the populations of these crisis-hit countries as a means of maintaining their purchasing power.

Beyond this potential safe-haven quality, crypto-assets are considered attractive assets for portfolio diversification because they have very little or negative correlation with traditional assets( Brière et al., 2015; Dyhberg, 2016; Gil-Alana et al., 2020, etc.). In addition, crypto-assets provide a gateway into finance for populations that were previously excluded from traditional finance. They give them access to new gains or sources of income through decentralized finance, for example.

Several studies have also shown that the price of Bitcoin, for example, tends to rise when anticipated inflation increases (Choi and Shin, 2021; Blau et al., 2021). However, these studies currently only cover the United States. It is therefore difficult to estimate the impact of Bitcoin on the wealth of populations facing hyperinflation.

Nevertheless, the idea of Bitcoin as a hedge against sustained high inflation is « popular » because the supply of Bitcoin is limited, transparent, and part of a « deflationary process. » Unlike fiat currencies or other traditional assets, the value of Bitcoin is not currently negatively affected by the issuance of new Bitcoins, given the significant gap between demand and supply. This quality therefore makes Bitcoin an attractive asset in a context of anticipated high inflation.

Conclusion

This article has outlined the motivations for adopting Central Bank Digital Currencies and more traditional crypto-assets such as Bitcoin or stablecoins. These crypto-assets offer new opportunities that could improve the well-being of economic agents.

However, certain factors must be taken into account. Central banks wishing to introduce a CBI must ensure that it is protected from technical problems that could jeopardize the payment system. Users’ private data must also be protected. Central banks should therefore not use unauthorized blockchains such as Bitcoin. The CBI should be accessible to everyone, even tourists. In addition, it would be necessary (perhaps in the early stages of implementation) to give the public the choice of having access to cash so that they do not completely reject the CBI, as people may see it as a means of total control by central banks.

Finally, users of « traditional » crypto-assets must be wary of their correlation with traditional markets, particularly ultra-speculative assets, in order to avoid significant losses of their assets. In some cases, the use of crypto-assets could be motivated by increased demand for alternative means of payment (in the event of international sanctions, for example, as in Iran with the risk of extraterritoriality) or, at the very least, serve as safe havens, at least temporarily, in the event of a major economic crisis leading to significant inflation and a fall in the value of a currency.

References

Auer, R. A., Cornelli, G., & Frost, J. (2020). Rise of the Central Bank Digital Currencies:

Drivers, Approaches and Technologies (Working Paper No. 8655). CESifo Working Paper.

Auer, R., & Boëhme, R. (2020). The technology of retail central bank digital currency.

Auer, R., Cornelli, G., & Frost, J. (2020). Taking stock: Ongoing retail CBDC projects.

Bank of England (2020). Central Bank Digital Currency: opportunities, challenges and design.

BFM Patrimoine. (2015). When the Greek crisis gives Bitcoin a second life.

Blau, B. M., Griffith, T. G., & Whitby, R. J. (2021). Inflation and Bitcoin: A descriptive time-series analysis. Economics Letters, 203, 109848.

Brière, M., Oosterlinck, K., & Szafarz, A. (2015). Virtual currency, tangible return: Portfolio diversification with bitcoin. Journal of Asset Management, 16(6), 365–373.

Chainalysis. (2021). The 2021 Geography of Cryptocurrency Report: Analysis of Geographic Trends in Cryptocurrency Adoption and Usage.

Choi, S., & Shin, J. (2022). Bitcoin: An inflation hedge but not a safe haven. Finance Research Letters, 46, 102379.

Dyhrberg, A. H. (2016b). Hedging capabilities of bitcoin. Is it the virtual gold?Finance Research Letters, 16, 139–144.

Flore, C. (2021). How do bank transfers work?, Copilote.

IMF. (2021). Global Financial Stability Report.

France 24. (2013). Is the dematerialized currency bitcoin feeding off the Cypriot crisis?

Gil-Alana, L. A., Abakah, E. J. A., & Rojo, M. F. R. (2020). Cryptocurrencies and stock market indices. Are they related?Research in International Business and Finance, 51, 101063.

Oeconomicus. (2021). The challenge of crypto-assets: from a single, indivisible currency to diverse and multiple assets.

Siècle Digital (2020). MNBC: understanding everything about the digital currency of tomorrow.

Sveriges Bank. On the possibility of a cash-like CBDC. Sveriges Riksbank, 16.

University of Anger. (2021). Fintech in Africa: a growing sector despite disparities.

[1]According to Chainalysis (2021), the volume of crypto-asset use increased by 880% in 2021 thanks to the heavy use of peer-to-peer exchange platforms in emerging countries.

[2]Globally, assets under management corresponding to crypto assets rose from around $18 billion in the first quarter of 2020 to $59 billion in thefourth quarter of 2021 (Cryptofund Research, 2021).

[3]« Banks whose deposits are covered by 100% reserves held by central banks. A portion of the interest paid by central banks may be returned to depositors, who can use these accounts as a safe savings option. » Narrowbanking.org.

[4]Auer et al. (2020) cite this motivation for the countries ranked highest by the World Intellectual Property Organization (WIPO). Countries with highly sophisticated means of production (infrastructure and businesses) are increasingly interested in CBIEs (Canada, France, Sweden, Japan, etc.).

[5]CBDCs would be more efficient than SWIFT, a slow system for entering and executing high-volume transactions.

[6]« Cash currently provides a useful contingency for electronic payment systems in the event of a disruption to card payment networks. However, as the use of cash in payments declines, the possibility of using it in a payment system emergency will also decline » Bank of England (2020).

[7]Brazil, Russia, India, China, South Africa.

[8]Venezuela has introduced a crypto-asset based on oil resources, the « Petro, » in order to better manage fund transfers and also the mining of crypto-assets.

[9]The relatively lower costs of digital platforms compared to physical models; availability of products/services tailored to the needs, personalized and at better prices for various customers; reduction of risks and costs associated with handling cash;

[10]Electronic wallet used to store Bitcoins used in El Salvador.

[14]However, this is becoming less and less true in Europe and the United States. For African assets, for example, crypto-assets are very weakly correlated, allowing them to be used as hedging and diversification assets (Shahzad et al., 2019; Colon and Gee, 2020; Omane-Adjepong and Alagidede; 2021).