Usefulness of the article: this article provides an overview of the development of renewable energies in the context of the energy transition and helps readers understand the issues and mechanisms involved. It lays the foundations for a concept that is still vague but is currently a hot topic.

Summary:

- The Paris Agreement set a target for reducing greenhouse gas (GHG) emissions in order to limit global warming to 2 degrees by 2100.

- One of the main challenges lies in changing energy production sources, which are still largely dominated by fossil fuels and polluting energies (34% for oil, 23% for gas, and 28% for coal).

- Numerous investments have been made in renewable energies over the past decade and should increase their share in the energy mix.

- The targets adopted by the Paris Agreement are ambitious but can only be achieved if the current economic model manages to absorb the set trajectory.

- Obstacles remain to ensuring a genuine energy transition, and the current trajectory deviates from the targets set.

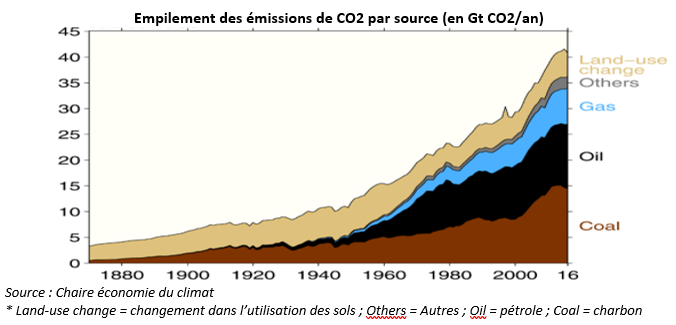

Sustainable development is more than ever at the heart of international debates. While global warming, among other things, is not a new phenomenon, the urgency of the situation is now prompting states and international institutions (IEA, UN, IPCC[1], etc.) to sound the alarm. New targets were set at the COP21 conference in Paris at the end of 2015, with the central objective of limiting global warming to 2 degrees compared to pre-industrial levels by 2100 (the 193 countries involved then agreed on the implementation of the agreement at COP24 in Poland). The reduction in greenhouse gas emissions will be achieved in particular through the development and promotion of renewable energies, since the ultimate goal of the latter is to replace carbon-based energies, which currently make up the majority of the energy mix. For a long time, carbon-free energy sources have been used in a complementary manner with other energy sources, following the « stacking » mechanism. The challenge of the energy transition is therefore to enable renewable energies to replace carbon-based energies and thus follow a » de-stacking » logic .

The energy transition involves a system in which energy consumption is optimized, which is achieved by 1) reducing decarbonized energy consumption for the same result and 2) promoting renewable energies. The challenges of the transition are important for the climate and health and will ultimately ensure energy independence.

1/ Where are we with the energy transition? Current trends and objectives

Current trends

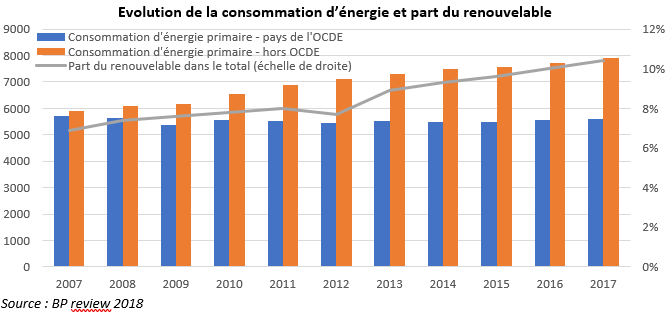

According to the latest statistics published by BP, in 2017, global primary energy consumption (i.e., unprocessed energy products) represented more than 13 billion tons of oil equivalent (TOE, a benchmark for standardizing energy measurement units), double the amount since 1973. Oil accounted for 34% of this share, natural gas 23%, coal 28%, nuclear 4.5%, and renewable energies 11%.

Non-OECD countries (59% of global consumption) in particular saw significant growth in their primary energy consumption over the decade 2007-2017, at 3%, while OECD countries (41% of global consumption) recorded growth of -0.2% over the same period. However, it should be noted that the population of non-OECD countries represents 83% of the world’s population and that the largest share of global poverty is found in these countries (their development reflecting higher energy consumption).

By region, Asia-Pacific accounts for the largest share of global consumption, at 42.5% (with annual growth of 3.5% over the past decade), more than half of which is attributable to China (23.2% of global consumption), while India accounts for 5.6%. North America is the second largest energy consumer with a share of 20.5% (16.5% for the United States; 2.6% for Canada; 1.4% for Mexico). Europe accounts for 14.6% of consumption, with Germany (2.5%) and France (1.8%) in the lead.

France’s primary energy consumption remained fairly stable over the decade 2007-2017, at 238 million TOE in 2017 compared to 260 million TOE in 2007. France’s energy mix is distributed as follows: 38% comes from nuclear power; 34% from oil; 16% from natural gas; 4% from coal; and 10% from renewable energies.

Trends in energy consumption and the share of renewables

There are traditionally three main sectors of energy consumption: (i) electricity consumption, accounting for 20% of total energy consumption; (ii) heating and cooling consumption (housing, industry, and agriculture), accounting for 48% of total consumption; and (iii) transport consumption, accounting for 32% of total consumption.

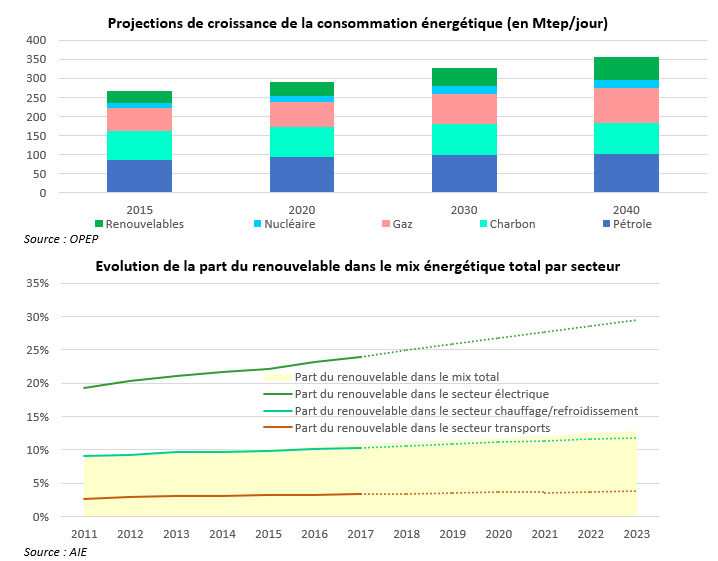

(i) According to figures from the International Renewable Energy Agency (IRENA), of the 24,800 TWh of electricity demand, 73.5% comes from non-renewable energy sources and 26.5% from renewable energy sources (16.4% hydro, 5.6% wind, 2.2% bio, 1.9% solar, and 0.4% other). According to projections by the International Energy Agency (IEA), 70% of the growth in global electricity demand will be supplied by renewable energies by 2023, with photovoltaics (solar) dominating this growth. This would enable renewable energies to account for 30% of electricity demand.

(ii) The share of renewable energy (RE) in heating and cooling (nearly half of global energy consumption) is 10% according to IRENA. Energy consumption in this sector is accounted for by 50% of the heat used in industry and almost as much for housing (cooling accounting for only a marginal share of energy consumption). By 2023, the IEA predicts that the share of renewable energy for heating and cooling will be 12%, driven by the use of solar or geothermal energy, electrical energy (renewable) or biomass (organic matter of plant origin, already used in the sector but presenting health risks).

(iii) Only 3% of the energy consumed in the transport sector comes from renewable energy sources (a sector dominated 95% by oil). Currently, biofuels (ethanol and biodiesel) constitute the renewable energy sources in transport, followed by electricity. The IEA estimates that the share of renewable energy in transport will remain virtually unchanged by 2023 (3.5%). The Paris Agreement has put the sector on the climate agenda and launched a dialogue on the subject. It also led to the creation in 2017 of an Alliance for the Decarbonization of Transport, joined by six countries (including France), six cities, and eight major companies in the sector (including Alstom and Michelin). In addition, five countries have committed to no longer selling new diesel and petrol cars (India, the Netherlands, and Slovenia by 2030, and France and the United Kingdom by 2040).

At the end of 2017, the vast majority of policies implemented focused mainly on the electricity sector (more than 150 countries have committed), highlighting the delay in implementing policies in the transport and heating/cooling sectors (only 48 and 42 countries committed respectively).

Objectives

The Paris Agreement sets out the targets to be achieved to prevent global warming from exceeding 2°C by 2100. Each participating country (193 in total) presented its national contribution on the sidelines of the summit, which subsequently materialized into a commitment. The agreement thus requires countries that have ratified it (currently 183 countries) to regularly update their climate plans in order to monitor the progress of the signatory states. In addition, developed countries are required to support the adaptation efforts of developing countries, which will involve paying USD 100 billion per year from 2020 onwards to assist developing countries in their energy transition. These payments will be channeled through the Green Climate Fund, created in 2009. According to the World Oil Outlook published by the Organization of Petroleum Exporting Countries (OPEC), 95% of the increase in primary energy demand between now and 2040 will be driven by consumption in developing countries, with China and India accounting for 50% of this increase. However, the Paris Agreement has its limitations. The targets presented by the signatory states are currently insufficient, as national contributions will only limit global warming to 3°C rather than 2°C, and there is no guarantee that the targets will be met (and no penalty mechanism).

The countries of the European Union have set a target of 32% for the share of renewables in the energy mix by 2030. A climate and energy framework was established in 2009 with targets set for 2020, then extended in 2014 to cover the period up to 2030 (the desired share of renewables was initially 27% before being revised upwards to 32% at the end of 2018). In addition, a 14% share of renewable energy is planned in the transport sector, thanks to the use of biofuels (vegetable oils).

In its report « Global energy transformation: a roadmap to 2050, » IRENA highlights the inadequacy of current policies and targets for achieving global warming of less than 2°C. While the Paris Agreement sets a target of 25% renewable energy by 2050, IRENA estimates that the share should be 65% by that date. The report highlights the efforts made in the electricity sector, but reaffirms that it is possible to achieve a level close to 100% renewable energy now that it has been proven that the technologies are available and that the cost is low enough and will continue to fall if investment continues.

In the industrial, residential (heating/cooling), and transportation sectors, the use of biomass and geothermal energy should be prioritized, with the former providing nearly two-thirds of renewable energy for heating and fuel. To achieve the targets set by COP21, total investment in energy efficiency must increase by 30% and represent 2% of global GDP each year, which will also have positive spillover effects on GDP, employment, and well-being, according to the same report. The IEA estimates that by 2040, if progress continues at the current pace, the share of renewable energy will be only 18%, well below sustainability targets of around 28% (and 25% under the terms of the Paris Agreement).

Projections for France

In 2017, France launched a €20 billion (US$24 billion) Grand Investment Plan (GIP) for the period 2018-2022 to accelerate the investment transition. Of this amount, nearly half (€9 billion) will be allocated to improving the energy efficiency of low-income households and public buildings; €4 billion to reducing transport-related GHG emissions (responsible for one-third of GHG emissions); and €7 billion to finance a 70% increase in renewable energy production capacity.

France’s objectives are set out in the Energy Transition for Green Growth Act (LTECV), which aims to achieve a 32% share of renewables in final consumption by 2030. Two action plans have been put in place to achieve the objectives set at the end of COP21 in Paris: the multi-year energy program (PPE) and the national low-carbon strategy (SNBC). The national action plan targets 27% renewable energy in final energy consumption by 2023, then 32% by 2030, translating into 15% renewable energy in transport consumption, 40% in electricity consumption, and 38% in heating and cooling consumption. Thanks to the falling cost of renewable energies, the last coal-fired power plants will have to be closed by 2022 and renewable electricity capacity will have to double by 2028, with the aim of reducing the share of nuclear power[3] to 50% by 2035 (currently 75%).

However, investment in renewable energy remains below what it should be according to the guidelines set by the PPE and the SNBC, according to the Institute for Climate Economics (I4CE) report » Panorama des financements climats » (2018). For example, the investment gap in renewable electricity is between €1.1 billion and €2.3 billion for the period 2016-2020, or more than a quarter of what is actually invested (€4 billion in 2017). More broadly, France has increased its climate investments in energy efficiency (which includes building renovation and transport infrastructure) from €14.4 billion in 2014 to €19.8 billion in 2020, while investments in renewable energies have stagnated, from €6.3 billion to €6.6 billion over the same period.

2/ Economic model for the energy transition

Investments

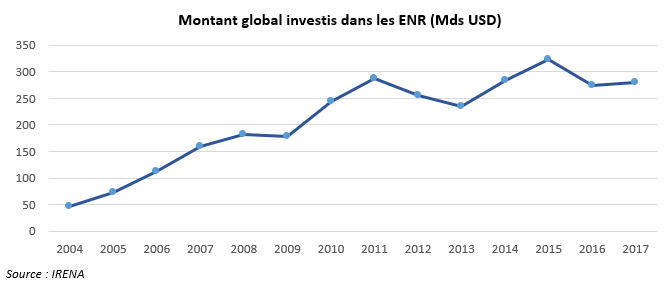

According to IRENA, global investment in renewable energy increased by 2% in 2017 compared to 2016, reaching $279.8 billion, bringing the cumulative investment since 2010 to $2.2 trillion.

Nearly 58% of the total amount invested in 2017 went to solar energy and 38% to wind energy (investments were therefore concentrated almost exclusively in the electricity sector). China remains the leading investor, with USD 127 billion in 2017, double the amount invested in 2013, followed by Europe with USD 41 billion and the United States with USD 40.5 billion. These investments enabled the installation of 157 GW of renewable energy, compared with 143 GW in 2016, representing an increase of 9.3%, while net additional fossil fuel energy production capacity was 70 GW.

Types of financing

(i) Asset financing is the primary source of investment in renewable energy, amounting to USD 216 billion in 2017 (as in the case of China’s USD 65 billion solar project[4] ). More than half of the financing (USD 122 billion in 2017) is provided directly by energy companies (on-balance-sheet financing), while 45% is provided through project financing, i.e., a mix of debt and equity capital for the project itself. The source of project financing is mainly debt from commercial banks, followed by the issuance of bonds (« green bonds ») and, to a lesser extent, national and multilateral development banks.

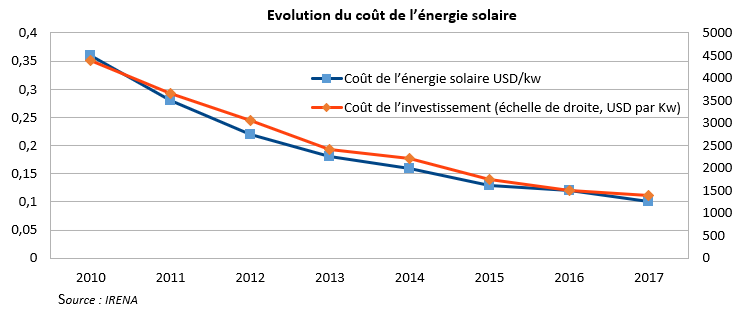

(ii) Investments in small-scale solar panels (less than 1MW) accounted for USD 49 billion (+15% compared to 2016) and represent the second largest type of investment in renewable energy. However, this amount is well below the average for the period 2010–2014 (USD 65 billion in annual investments on average). This decline is mainly explained by the fall in installation costs (see below): a dollar invested in 2017 generates much more capacity than a dollar invested at the beginning of the decade. For example, the average cost per watt for a photovoltaic (solar) system in Germany fell from $3.9 in 2010 to $1.7 in 2017. This has led to a doubling of small installed capacity since 2013, to 173 GW in 2017 according to Bloomberg New Energy Finance statistics (+28 GW compared to 2016).

(iii) Investment in R&D increased for the fourth consecutive year, by 6% in 2017 to a record level of nearly $10 billion, growth largely explained by the increase in the private sector’s share (to $4.8 billion, or nearly 50% of the total amount invested in R&D). Europe was the leading investor in R&D in 2017 (USD 2.7 billion), followed by the United States (USD 2.1 billion) and China (USD 2 billion).

Costs

Investments in renewable energies mainly benefited solar and wind power installations. This concentration of investment in solar and wind power can be explained in part by a decline in the cost of installing photovoltaic solar panels and wind turbines: the overall price of solar installations has fallen by an average of 73% since 2010 and now stands at an average of $100 per MWh (prices vary from region to region[5]). This price level is becoming competitive with that of fossil fuels. The Renewable Energy Policy Network for the 21st Century (REN21) explains this decline in cost by i) increased competition and technology in components; ii) lower capital costs due to a decrease in perceived risk; and iii) « rock-bottom » bids explained by low operating costs in countries with abundant solar resources (this has been the case in Argentina, India, Mexico, etc.).

Public policy

To support projects that increase the share of renewable energy in electricity consumption, 113 countries (EU, China, India, etc.) have adopted systems establishingfeed-in tariffs for renewable energy producers. These electricity tariffs are set in advance by electricity suppliers (mainly EDF in the case of France) and guaranteed over a long period (between 15 and 25 years) to renewable energy producers. These operations are generally governed by power purchase agreements. For renewable energy investors, these long-term contracts offer a purchase guarantee, transparency on operations, and easier forecasting, substantially reducing the risk and cost of investment, thereby encouraging investment in renewable energy and the achievement of energy transition objectives. In 2017, 113 countries adopted this type of policy to encourage investment in renewable energy, according to REN21. However, this method has certain disadvantages, notably the setting of the right price per unit of renewable energy produced. If the price is too low, projects will be less attractive; if it is too high, profits will be excessive and the costs of renewable energy will also be high. Experience has shown that there is a significant information asymmetry with this method, prompting governments to find other solutions to promote the growth of renewable energy.

Another, more competitive system of calls for tenders has been set up in 29 countries to promote the growth of renewable energy, with costs reflecting those of the market. Governments are generally the issuers of calls for tenders, which specify the capacity to be installed, the technology to be used, and the location of the installation. Renewable energy producers submit their bids, with the price and capacity they can produce. This allows competition to play its part, with the government choosing the best bids that will meet the initial capacity demand (several bids may be selected). In 2017, 29 countries were using the tender system (including France, Germany, India, Israel, Mexico, etc.).

- The two systems described above are now gradually complementing each other, with small-scale projects benefiting from subsidized tariffs while large-scale projects are subject to public tenders, encouraging competition. It is these subsidies that have enabled the development of small-scale installations in many countries. Another system used in several countries allows consumers who generate their own electricity to sell what they do not use on their site (farms or schools, for example).

Other measures can support the energy transition, including tax incentives and/or public funding. These measures can take the form of tax credits on investments or production, reductions on certain taxes, or preferential-rate loans. In France, for example, there is an energy transition tax credit (CITE) on expenses incurred to make a home more energy efficient (tax credit representing 30% of the expenses incurred for renovations). These mainly concern energy efficiency, rather than renewable energies. A parliamentary information report on public tools encouraging private investment in the ecological transition was published in January 2019. In particular, it recommends estimating public and private investment needs in relation to the SNBC and the PPE; placing environmental taxation at the heart of tax reform in order to give full effect to the « price signal »; strengthen and renew public support mechanisms for household investment in energy-efficient home renovation and the purchase of clean vehicles; strengthen and accelerate the process of developing green finance (transparency on the environmental impact of investments, etc.).

3/ Obstacles

According to energy experts (IEA, IRENA, I4CE, etc.), the investments made to date in renewable energies may not be sufficient to achieve the objectives of the Paris Agreement. Obstacles remain to the more rapid development of renewable energies in the energy mix.

Despite their falling costs, renewables are still seen as a complement to fossil fuels rather than a substitute.We have seen in the previous paragraphs that the cost of investing in photovoltaic or wind turbine installations has fallen sharply over the past decade and is now close to the cost of fossil fuels. In fact, the prices of renewable energy production and storage have fallen by a factor of six on average between 2010 and 2018 (from $180 per kWh to $30). These declines are expected to continue with the stimulation of investment in renewable energy production, while fossil fuel prices, primarily oil, are set to rise due to limited resources. However, as highlighted in the article « The energy transition in the face of the climate clock » by the Paris Dauphine Climate Economics Chair, the favorable price trend (rise in fossil fuels, fall in renewable energy) is part of a stacking pattern in which renewable energy complements rather than replaces fossil fuels. The article takes the example of oil and shows that when the price per barrel is high, consumption in importing countries tends to decrease, which is beneficial for the development of renewable energy and the reduction of CO2 emissions. However, exporting countries will still become richer and will be able to invest in the extraction of unconventional resources (shale oil), potentially causing an increase in GHG emissions in the long term. Conversely, when the price per barrel is low, it directly competes with the price of renewable energies. Governments will then need to put in place stronger incentives to promote renewable energies, for example through higher taxation on carbon-based products (Sweden is an example of this), or the establishment of a permit market, etc. Price plays a fundamental role in any market in finding its equilibrium, and the energy market is no exception.

The energy subsidies applied in many countries, particularly oil-producing countries, do not encourage investment in renewable energies. Low consumer prices for fossil fuel-based energy products (such as gasoline from oil or electricity from gas) lead to (i) a lack of incentive to invest in low-carbon energy and (ii) excessive consumption of these products. Heavy subsidies on gasoline are found in most countries in the Gulf, North Africa, Central Asia, and others such as the United States. Conversely, it can also be difficult to apply new taxes on these products, such as the carbon tax in France, which is still proving difficult to implement. Energy subsidies (particularly for fossil fuels) therefore mask the real price and benefits of an energy efficiency project.

Other economic and non-economic barriers are hindering the faster development of renewable energies. There is still an information asymmetry between investors and the market, for example on feed-in tariffs, which can sometimes be higher than actual market prices, making investment projects less attractive. Public authorities must provide impetus through information campaigns and incentives for both consumers and producers. Indeed, for many energy efficiency investment projects, the benefits may accrue to those who have not invested (e.g., GHG reductions or improved energy security), just as polluting investments cause damage to those who do not benefit from them. These externalities should therefore be incorporated into project assessments, which is primarily the responsibility of public authorities.

Conclusion

The development of renewable energies remains a global climate challenge, but it is a long and costly process. It must enable a transition from a model dominated by carbon-based energies to one in which renewables play a major role. The current economic model and available technologies have made it possible to achieve a significant share of renewable energy in electricity consumption, but it remains low in the most polluting sectors, namely transport and heat sources in industry and housing. The Paris Agreement signed in 2015 crystallized climate objectives by setting out the goal of limiting global warming to less than 2°C, but the national efforts of the participating countries have so far proved insufficient to achieve these objectives. Efforts will have to be stepped up, politically, economically, and technologically, in order to achieve a share of renewable energy that meets sustainability targets. Beyond the development of renewable energy, the energy transition must involve energy efficiency, which translates into a reduction in per capita energy consumption for the same result.

[1] The IEA (International Energy Agency) was created by the OECD in 1974 and regularly publishes outlooks on energy markets. The UN (United Nations) has a United Nations Environment Program, which sets global trajectories and recommendations. Together with the World Meteorological Organization, this Program is behind the creation of the IPCC (Intergovernmental Panel on Climate Change), which provides (neutral) scientific and economic expertise on global warming. In its latest report, the IPCC assessed the impact of global warming of 1.5°C and the corresponding GHG emissions.

[2] Energy independence is also an important aspect of the energy transition. Indeed, an economy constantly needs access to a cheap source of energy to function properly. The scarcity of fossil fuels could lead to high energy prices and could have strategic and military consequences.

[3] Nuclear power is an energy source that emits almost no GHGs, but the technology involved presents dangers, which is why France wants to phase it out.

[4] China generated USD 103 billion in asset financing on its territory (+14% compared to 2016).

[5] In the United States, for example, the price per MWh fell below USD 60 before rising again this year due to increased trade taxes.