Should we be concerned about renewable energies?

Part 1: Are renewable energies « linked » to oil prices?

Summary :

· Empirically, no slowdown was observed in the renewable energy sector during the period when oil prices fell sharply.

· The link between oil and new energies is particularly complex, if not virtually non-existent, given that these two products do not compete in the same markets (with the notable exceptions of the automotive industry and electricity production in certain low-income countries);

English version

French version

Whatever the underlying causes, the fall in oil prices observed since mid-2014[1]—and their continued low level since then—should intuitively cause collateral damage: a slowdown in the development of renewable energy sources. This « intuition » stems from the idea that low oil prices should encourage direct consumption of fossil fuels (fuel, electricity, etc.), thereby dampening the enthusiasm of those who already saw the success of COP21 as the promise of a « greener » future. In this regard, the Financial Times uses nothing less than the image of « kryptonite » to describe the effect of falling oil prices on the cleantech sector and renewables in general.

However, it is interesting to ask whether there is a real negative link (both conceptually and empirically) between oil prices and the development of clean energy.

An « epiphenomenon »?

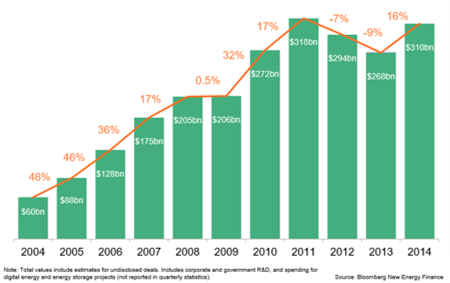

Analysis of the data shows that during the period when oil prices fell by half (2014-2015), there was no wave of major bankruptcies in the renewable energy and cleantech sector, nor were there any colossal losses in « green » funds. On the contrary, new investments (globally) in green energy increased by 16% (to a total of USD 310 billion), after two consecutive years of decline[3] (see graph below).

In addition, capital investment in the sector rose by 54% in 2014, clearly showing that the market is becoming increasingly attractive, albeit in a sector that is well supported by public subsidies, which are enabling it to gradually gain market share and generate profits in order to become more competitive with fossil fuel competitors (although, as we will show later, the role of subsidies in the competitiveness of renewable energies is becoming less and less significant).

Figure 1: Global capital investment in the renewable energy sector (source: BNEF)

However, there was a slight underperformance in the returns of the largest cleantech companies during the second half of 2014, but longer-term data clearly shows that this was only a temporary phenomenon, mainly due to an overreaction by the markets (see below) typical of the renewable energy sector.

There are many examples of this « epiphenomenon, » starting with the Danish wind power leader Vestas, whose share price fell sharply between July and December 2014, before returning to its initial value in 2015 and rising steadily since then. The same is true for the hybrid vehicle sector, starting with its flagship Tesla Motors.[5]. For most other companies in this sector, the period 2014-2015 even saw an acceleration in investment and revenues[6]. All these examples show us that companies in the renewable energy sector have demonstrated strong resilience, or even a total lack of reaction to the fall in oil prices. Let us now explain the reasons behind this lack of correlation.

A complex link in theory but in practice…

In theory, intuitively asserting a clear link between oil prices and the development of renewable energies is much more complex than one might think. On the one hand, high oil prices could be a catalyst for the development of clean energy, as consumers would seek other energy sources (solar, wind, biomass) that are cheaper than fossil fuels. However, on the other hand, high oil prices could encourage investment in this sector, particularly in costly extraction processes (oil sands, shale oil, etc.), which would ultimately reduce the price ofoutput. Obviously, this paradox is reversed when prices are low, but it is still impossible to say which effect would prevail over the other.

The most important factor to consider when explaining the virtual absence of a link between oil prices and the development of renewables is the fact thatthey operate in different markets: oil is mainly used in the transport sector (as fuel) but very little in electricity generation (5% worldwide), while renewables are mainly used for electricity generation. From an economic point of view, oil and renewables are therefore not substitutes: when the price of one falls, demand for the other is not expected to fall. If there is a link between the price of renewables and the price of oil, it would therefore be via electricity prices, and more specifically via gas prices, which is the main source of electricity production in many countries (27% in the US and 19% in Europe) and therefore the « floor » price in these same markets. Since gas prices are also often linked to oil prices (particularly in Europe) via spot contracts, it is possible to imagine a link between oil and renewables via the gas markets.

However, a drop in spot gas prices does not pose an immediate risk to green energy:

1. Because gas is replacing coal (which is even more polluting);

2. Because a permanent energy source is needed to support production from renewables, which is intermittent by nature;

3. And finally, because most of the cost of electricity is used to cover transmission and distribution costs, not the cost of the input[7].

In addition, renewables are « largely insulated » fromfossil fuel prices, as the energy they produce is sold back through long-term contracts at fixed costs; capital, operating, and financing costs also represent a significant portion of these fixed costs.

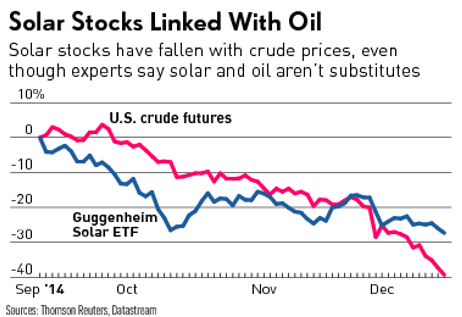

The conclusion of this « separation » theory is that fossil fuels and renewables have completely different roles and drivers. However, this absolute separation is not so clear when we look at the correlation between renewable energy share prices and oil prices, particularly when the latter began to fall in Q3 2014—the example (graph below) of Guggenheim Solar ETF shares vs. US crude oil futures is characteristic of this phenomenon. This irrational and purely psychological correlation can in fact be explained by the widespread belief that the price of oil represents the price of energy in general, which can discourage investors, politicians, and consumers from supporting the renewable energy sector because they believe that all energy is cheap when oil is cheap[9].

Graph 2: Solar sector share prices (example of Guggenheim Solar ETF) vs. oil prices

Apart from this « psychological » correlation, there is no link between oil and renewable energies, and therefore no reason why the price of the latter should be linked to the price of the former. The only direct link that could exist between the two products would be within the automotive industry, where sales of hybrid and electric vehicles could suffer from a resurgence in sales of gasoline-powered vehicles (due to lower fuel prices). Similarly, the existence of numerous mutual funds and exchange-traded funds that include both renewable energy and oil products could explain a certain correlation between the two products.

Conclusion

We can therefore conclude that there is no fundamental link between fossil fuels and renewable energies. However, several factors can help explain the unprecedented and significant growth of green energies during this period of low oil prices. These factors will be analyzed in the second part of this article.

[3]http://about.bnef.com/presentations/clean-energy-investment-q4-2014-fact-pack/content/uploads/sites/4/2015/01/Q4-investment-fact-pack.pdf

[6]The American private equity firm KKR acquired the Spanish photovoltaic panel manufacturer Gestamp, Siemens acquired the Danish wind power producer Dong Energy (for $1.2 billion), and SunEdison acquired Vivint Solar.