Summary:

- The end of milk quotas in 2015 led to a drop in prices;

- There is a wide disparity between the prices obtained by producers;

- The organization of the sector and the role of farmers are essential to ensure that products are properly valued and that added value is redistributed fairly.

- In the medium to long term, European agriculture must choose between increasing competitiveness to support low prices, or positioning itself in the high-end market with higher profit margins, which would require a reduction in production.

Agriculture is a strategic sector in France, yet it has been in crisis for several decades. The dairy industry has been particularly affected by the opening up of European (elimination of quotas) and international (overhaul of CAP subsidies) competition. The average price of milk is increasingly low and unstable, but some producers manage to obtain a much higher and more consistent price. How can this be explained? Could they all obtain these prices?

The situation in the dairy industry is often highlighted because of: milk prices that are not profitable for producers, an oligopolistic market organization that favors processors (and especially large retailers), and an institutional environment that has deteriorated significantly with the end of milk quotas.

These quotas were introduced in the 1980s following a significant slowdown in regional and global demand. Europe, faced with huge production surpluses, was no longer able to pay subsidies. To ensure the stability of the system, the decision was taken to introduce production quotas. Today, regional and global consumption is high and the European Commission wants to limit its interventions as much as possible.

With quotas eliminated (in 2015), producers increased their output. For their part, buyers, in an oligopolistic situation, exerted downward pressure on prices. The decline was significant: from 2014 to 2016, the average price fell from €450 to €350 per 1,000 liters. Many producers saw their margins decline sharply (or even become negative) and were unable to cope with this decline.

However, this situation is not inevitable. A different vision of European (or at least French) agriculture in the medium/long term could enable producers to take part in the organization of supply chains, move upmarket, and obtain more profitable prices. In this article, we will see that French producers do not all sell their milk at the same price, that some obtain profitable prices, and that different supply chain organizations are possible.

Milk prices

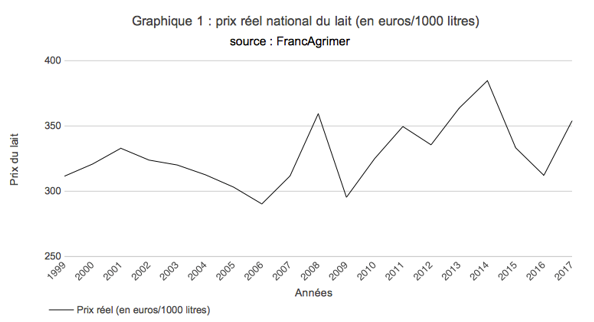

The price of milk in France has fluctuated between €290 (in 2006) and €380 (in 2014) per 1,000 liters of milk, as shown in Figure 1. Then, a very significant drop in milk prices occurred in 2015/2016 following the elimination of milk quotas. The price increase observed in 2017 (as well as in 2018) confirms its general instability, but it is mainly due to a slowdown in production linked to climatic phenomena.

On average, the price of milk is not high enough to guarantee the profitability of small farms, where production per worker and per dairy cow is relatively low. It is only suitable for highly intensive farms, where economies of scale have been achieved through herd expansion and productivity gains have been made through investment in efficient, automated infrastructure. However, these economic approaches are not always accessible to everyone (e.g., farms whose financial health does not allow them to take on debt, farms that are already heavily indebted). Furthermore, they may not suit the choices of producers. They therefore sell at a loss and obtain very low or even zero remuneration.

However, some farmers obtain much more attractive prices for their production. This is the case, for example, for farmers selling milk for certain PDOs (Protected Designation of Origin) or PGIs (Protected Geographical Indication). In Franche-Comté, for example (home of the Comté PDO), farmers in the area sold their milk for a minimum of €480/1000L between 2016 and early 2018, with a maximum price of €560 in 2017. They therefore obtained a price that was 25 to 45% higher. Similarly, farmers in Savoie and Haute-Savoie selling their production to the region’s PDO and PGI[2] obtained a differential according to the AFTalp (Association des Fromages Traditionnels des Alpes Savoyardes) of around 15 to 35% in 2014 (the last year before the end of quotas). Moreover, in 2015, the selling price of milk in these PDO/PGI areas remained stable while the national price collapsed. The differential thus increased to 30% and up to almost 60% for Reblochon milk.

These differentials are virtually constant over the long term. Furthermore, the stabilization of the selling price following the disappearance of milk quotas shows that producers of these PDO/PGI products are partly « protected » from national, European, and international competition. These organizations have enabled the creation of a separate market that is much more stable and profitable, as the entry of new farms is extremely limited, as is the production of existing farms. It is therefore possible to sell milk at a price well above the French average, which is the result of a specific sector organization.

Explanations

The higher-than-average French price is explained by the specific organization of these sectors. As Dervillé and Allaire analyze in their 2014 article, each link in the production chain is important for:

- Obtaining a good return on the finished product (in this case, cheese) and;

- Redistributing this value throughout the chain, particularly to producers.

It is important to understand that in these sectors, it is not only milk that creates value, but first and foremost the finished product, i.e., cheese. Of course, this cheese is of very high quality and is highly valued, partly because the milk used to make it is also of very high quality, and partly because of the organization of the sector, which leads to interesting decisions regarding product differentiation and positioning.

Indeed, the success of the Comté and AOP des Savoies sectors stems from the creation of a certain rarity and a clear focus on quality production. This explains the importance of promoting cheese: these sectors have moved upmarket. This decision could not have been taken without the unity of the players in the sector, particularly the producers. The redistribution of the added value created can be explained by the involvement of producers at every stage of the value chain, particularly in decisions regarding production volumes (tons of cheese produced) and milk quality.

This organization is not found in Cantal, where the Cantal and Saint Nectaire PDOs exist and producers sell their milk at a price very close to the French average (Dervillé and Allaire 2014). Being a PDO or PGI is therefore not enough.

The Comté and Savoie PDO sectors have set up governance institutions involving producers and processors to collectively organize their resources. Although they appear to fall outside European free competition law, they are legal thanks to the regulations on PDOs and PGIs. In 2012, Europe also voted (in anticipation of the end of quotas) for the mini milk package, which gives producer organizations greater bargaining power in the markets when dealing with processors and distributors in an oligopoly situation.

Limitations

These observations are very encouraging for the future of our agriculture in crisis: it is possible to create value and make a living from agriculture. Nevertheless, they have several limitations that are important to point out.

In the PDO sectors mentioned above, the added value of milk is the result of the added value of cheese, which itself has a long history and an extremely strong link to the territory (remember that PDO and PGI cheese can only be produced in very limited areas, using milk from that area).

Not all milk producers in France can sell to PDO and PGI organizations, and even if they could, this would not guarantee the promotion of cheese, let alone the redistribution of value to the price of milk. It is necessary to set up bodies that include a large number of producers and create a certain scarcity of the product. As we have seen above, this is the choice that has been made in the Comté sector and in the Savoyard PDOs. There may be different forms of organization, but they must guarantee at least these two elements:

- Unite the players in the sector to ensure the promotion of the finished product (scarcity and communication) and;

- Ensuring that farmers have a significant say in industry decisions (particularly regarding production quantities and milk quality) to guarantee value redistribution.

Another limitation is consumers’ willingness to pay[3]. This is a fundamental issue because it is not possible to increase the price of a product (cheese, butter, or other) without knowing whether consumers would be willing to pay more for these products. Moving upmarket and making the product scarcer would therefore have no positive impact on the price.

Finally, it is important to take production costs into account. Producing PDO milk means complying with production specifications that can be very strict. This inevitably increases (and sometimes significantly) production costs, which means that a higher price for milk must be obtained. Even if producers benefit from this, it limits the differentials mentioned above.

Conclusion

In conclusion, and despite the limitations we have just outlined, we can conclude that scarcity and upmarket positioning are good strategies for obtaining a higher price and thus better remuneration for producers.

However, the issue is broader than that, because the choice of PDOs and PGIs to adopt strict specifications, combined with consumer expectations that largely determine their willingness to pay, leads to a rationalization of production rather than an increase (at ever lower costs).

The medium/long-term vision for European agriculture is therefore a pressing issue, and with it the potential loss of its position as the world’s leading agricultural economy in terms of quantity produced.

Sources:

AFTalp: presentation for the INAO (National Institute for Origin and Quality) https://www.inao.gouv.fr/content/download/1738/17365/version/1/file/2_impacts%20%C3%A9conomiques%20et%20territoriaux%20des%20fromages%20AOP%20et%20IGP%20de%20Savoie.pdf

Dervillé and Allaire « What prospects for mountain dairy sectors after the abolition of milk quotas? An approach in terms of competition regime, » INRA Prod Anim ? 2014 ? 27(1), 17-30

https://s3.amazonaws.com/academia.edu.documents/44530618/Quelles_perspectives_pour_les_filires_la20160408-30077-1q8v749.pdf?AWSAccessKeyId=AKIAIWOWYYGZ2Y53UL3A&Expires=1531663862&Signature=dwuj0bHTVJyBE%2BcbYqSJozKBtgo%3D&response-content-disposition=inline%3B%20filename%3DQuelles_perspectives_pour_les_filieres_l.pdf

DRAAF (Regional Directorate for Food, Agriculture and Forestry): http://draaf.auvergne-rhone-alpes.agriculture.gouv.fr/

Banoît Rouyer, Director of Economic Affairs at CNIEL: http://www.web-agri.fr/observatoire_marches/article/vers-une-hausse-du-prix-du-lait-grace-au-ralentissement-de-la-production-1929-139251.html

[1] It is important to note that several agricultural unions across Europe have always been opposed to the quota system and therefore played a major role in its elimination.

[2] PDO: Reblochon, Abondance, Tome des Bauges, Beaufort, Chevrotin; PGI: Tomme de Savoie, Emmental de Savoie, Raclette

[3] Largely linked to the history of cheese, consumer perceptions and, of course, investment in marketing.