Summary:

· France has excessive imbalances according to European criteria and remains under surveillance by the European Commission;

· The budget deficit has been reduced but remains above the 3% threshold. The government is maintaining its target of 2.7% of GDP for 2017, based on an assumed growth rate of 1.5%;

· France is in a situation of twin deficits, i.e., a public deficit and a current account deficit. These deficits can weaken a country’s economy, with the risk of increasing its debt, losing the confidence of foreign investors, and implementing austerity policies necessary to achieve a balanced budget.

The financial crisis has brought to light the risks associated with the interconnections between economies. The macroeconomic imbalances of one country can affect the economies of other countries. To better analyze and control the risks associated with this phenomenon, European institutions have put in place an alert mechanism (RMA[1]) in effect since 2012, which aims to detect and monitor imbalances in member states through a scoreboard and an annual report. For countries with significant imbalances, macroeconomic imbalance procedures (MIP) may be triggered, consisting of an in-depth examination of the causes and accompanied by proposals to reduce deficits and/or surpluses.

In 2016, the European Commission conducted an in-depth review of the economies of 19 states. Of the 19 member states monitored, six[2] countries showed no apparent imbalances, seven[3] countries had imbalances, and six[4] had excessive imbalances according to the thresholds set by the European Commission, including France.

In this article, we will focus on the case of France. We will begin by examining the budget deficit and its trajectory over recent years, as well as a comparison with that of other countries. Next, we will look at France’s current account balance, with a focus on the trade balance. We will conclude by discussing the risks associated with these imbalances and the potential consequences for the French economy in the future.

1. Twin deficits

France has structural deficits in several major macroeconomic aggregates, notably a budget deficit and a current account deficit. France is said to be in a situation of twin deficits[5].

1.1 The budget deficit

France had a budget deficit[6] of 3.5% of GDP in 2015 and 3.3% in 2016. The government is forecasting a deficit of 2.7% in 2017, slightly below the 3% threshold set by the Stability Pact, as illustrated in the graph below. For its part, the European Commission had anticipated a deficit of 3.4% in 2016 and confirms that it will fall below 3.0% in 2017.

France’s deficit level in 2016 is comparable to its 2008 level (3.2%), but it rose sharply following the financial crisis, peaking at 7.2% in 2009. The deficit has been contracting since then, but nevertheless remained high, above 4.5% for five years until 2014. This can be explained both by a modest acceleration in growth (+0.2% in 2014 and +1.2% GDP in 2015), leading to an increase in tax revenues (+€2.2 billion in VAT revenues and +€1.9 billion in domestic tax on energy consumption), but also by a reduction in the debt burden thanks to low borrowing rates and a decline in local authority investment spending (€4.1 billion in 2015), following a €11.5 billion cut in government grants. France had previously benefited from several postponements in meeting the European target, but this will no longer be the case in 2017. The government plans to achieve this target through a €1.5 billion effort on social security accounts, the postponement of tax cuts until 2018, and higher growth (estimated at 1.5% of GDP in 2016 and 2017).

As illustrated in the graph above, the 2008 financial crisis and the 2010 debt crisis worsened the deficits of European countries and increased pressure on them to actively reduce these deficits. Germany, meanwhile, has been a model student, running a surplus since 2014.

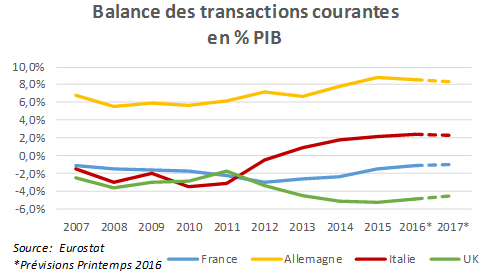

1.2 The current account balance

The current account is one of the three components of the balance of payments, along with the capital account and the financial account.

France’s current account has been in deficit since 2005 but has been improving since 2012, falling from -2.9% of GDP to -1.5% in 2015. The European Commission forecasts a recovery of +0.4% and +0.1% in 2016 and 2017. Germany posted a high surplus of 8.8% of its GDP in 2015 thanks to its largely positive trade balance. Since 2013, Italy has also posted a surplus, which reached 2.2% of GDP in 2015.

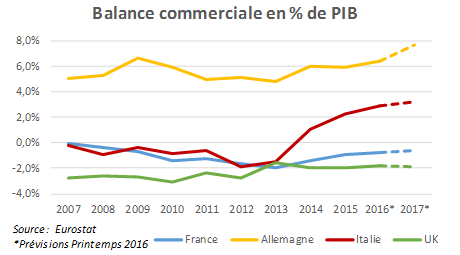

As illustrated in the graph opposite, France’s current account deficit is mainly due to its trade deficit. Indeed, the latter has been in deficit for several years and stood at -1.0% of GDP at the end of 2015, compared with -1.4% the previous year. The balance has been negative since 2002, but has been improving since 2011, when it stood at -€75.4 billion, compared with -€58.3 billion in 2014 and -€45.7 billion in 2015. This deficit costs growth points: 0.3 GDP points in 2015 according to INSEE and 0.5 in 2014.

Such a trade deficit raises questions about France’s competitiveness in terms of both price and added value of products and services (i.e., differentiation through innovation, niche markets, etc.). The dynamic growth of emerging economies, the low geographical diversification of exports, and the weak growth of the euro zone, which remains France’s largest export market, largely explain the decline in France’s market share from 5.1% in 2004 to 3.1% in 2015. Nevertheless, France remains the world’s fifth largest exporter, according to INSEE.

For its part, Germany maintains a high trade surplus, 5.9% of its GDP in 2015, and remains the world’s second-largest exporter. The European Union also has a surplus of 1.3% of its GDP. Italy has had a positive balance since 2014 (1.0%) and appears to be following an upward trend.

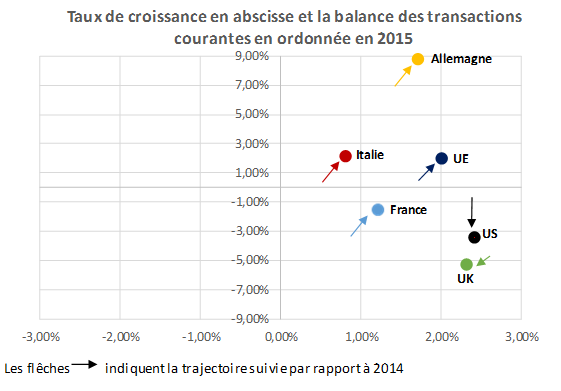

These persistent imbalances are indicative of insufficient growth. Indeed, the amount of imports, income, and transfers paid to other countries exceeds the amount received and exports. France therefore resorts to foreign financing to make up for this deficit and thus boost its growth. This financing, which is investment for growth, should increase GDP and therefore income. However, this is not sufficiently the case.

2. Risks for the French economy

The first risk is an increase in public debt. The budget deficit has led to an increase in public debt because the government has continued to borrow to meet its expenses. According to European Commission figures from 2015, France’s total public debt has continued to rise since 2007, from 64.4% of GDP (€1.2 trillion) to 95.8% of GDP (€2.06 trillion). An excessive increase in French public debt could lead to a loss of confidence among foreign investors, which would cause an increase in the borrowing rates on bonds issued by the French government. An increase in rates would cause an increase in the debt burden, leading to a vicious circle of debt for France. The case of Greece comes to mind, with a partial default by the country, even if this represents the worst-case scenario. It should be noted here that, until now, France has benefited from low borrowing rates, thanks both to the country’s credit rating and to the support of the European Central Bank through its quantitative easing ( QE) policy, which keeps downward pressure on sovereign bond yields.

A second risk concerns France’s trade deficit. In order to reduce the current account deficit, the government could either implement measures to boost exports, with uncertain effects, or reduce imports, notably through protectionist measures, with the risk of retaliatory measures from partner countries. Furthermore, lower imports would reduce growth and could worsen the budget deficit by reducing the government’s potential tax revenues, making it more difficult to achieve the Maastricht budget deficit target of 3.0% of GDP.

The final risk is the possibility of a sudden adjustment in the budget balance through austerity measures made necessary by an excessive and prolonged deficit. Reducing the deficit too quickly would weigh on economic growth and could push France into recession in the short term. This would result in lower tax revenues and a worsening of the budget deficit, leading France into a vicious circle of debt.

These deficits are indicative of a lack of dynamism in France’s economic growth. They could weaken France’s position vis-à-vis its external partners, as its economy is, in a sense, operating on credit. France, despite its deficits, has not experienced a major crisis because investors have continued to buy French debt bonds at low rates (1.14% for 10-year bonds was reached during the session on February 6, 2017, the « highest » in 17 months) and to invest in its companies, proving their confidence in France’s ability to repay its debts.

Conclusion

France suffers from several imbalances, such as public finance deficits and trade deficits, combined with high levels of debt. These imbalances have a short- and long-term impact on debt, foreign investor confidence, and economic growth. On a more optimistic note, the trajectory of a recovery in public finances and accelerating growth are positive signals for economic activity. However, the risks associated with drastic measures to adjust the budget balance or the current account balance could weigh on the French economy in the long term.

[1] Alert Mechanism Report

[2] Austria, Belgium, Estonia, Hungary, Romania, United Kingdom

[3] Finland, Germany, Ireland, Netherlands, Slovenia, Spain, Sweden

[4] Bulgaria, Croatia, Cyprus, France, Italy, Portugal

[5] When a country has a budget deficit and a current account deficit.

[6] Government expenditure exceeds revenue, resulting in a budget deficit.