Usefulness of the article: In France, the transportation sector is the main source of greenhouse gas emissions, contributing to climate change and air pollution, which is harmful to public health. Hydrogen is emerging as a low-carbon alternative to fossil fuels, but concrete actions to develop the market remain limited. Based on the experience with diesel, demand-side instruments can be found that have a positive effect on the adoption of hydrogen. Supply-side instruments, such as cluster deployment, are also possible.

Abstract:

- In France, the transport sector is the largest contributor to greenhouse gas emissions (31%) and air pollution.

- Hydrogen has great potential as a low-carbon solution for the transport sector. Supply- and demand-side instruments can nevertheless facilitate its deployment.

- On the demand side, the tools used for diesel include energy taxes, product taxes (or subsidies) such as bonus-malus schemes, and « vintage » restrictions.

- On the supply side, the deployment of captive professional fleets in clusters, as well as public transport, can help to reduce the costs of adopting this technology.

- However, in order to achieve the government’s low-carbon strategy objectives, it is necessary to continue current efforts to reduce greenhouse gas emissions.

Against a backdrop of strong growth in the global population and travel flows, the transport sector is associated with numerous negative externalities: pollution, noise, fatigue, stress, and road safety issues. Vehicles are responsible for two types of emissions: i) greenhouse gases (GHGs: carbon dioxide, methane, nitrous oxide, etc.) that contribute to climate change, and ii) gases that are harmful to public health (nitrogen dioxide, fine particles, sulfur dioxide, carbon monoxide, etc.).

According to the Senate, air pollution, which is difficult to reduce in urban areas, is responsible for tens of thousands of deaths each year. In France, the cost of air pollution is estimated at between €70 and €100 billion per year. According to the European Environment Agency (EEA), in 2016, within the EU-28, the transport sector accounted for 27% of greenhouse gas (GHG) emissions. In France, it is the sector that contributes the most to GHG emissions, at around 31%.

Figure 1: Breakdown of GHG emissions by sector (2018)

1. Some background information on the situation in France

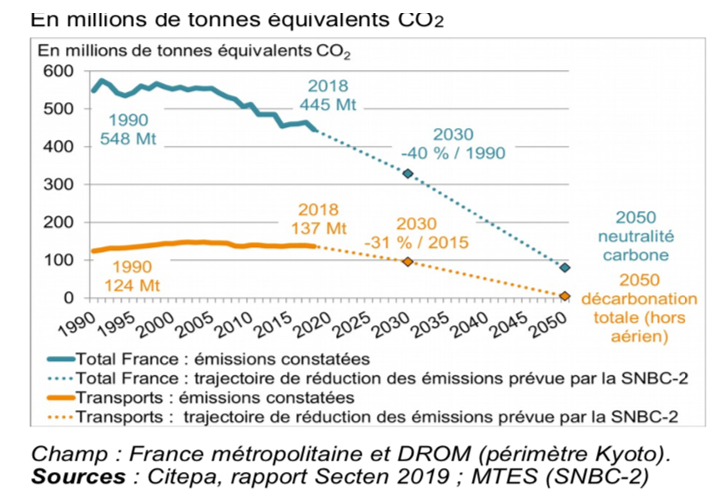

In France, in 2018, after three consecutive years of increasing emissions, a 1.6%[3] reduction was finally achieved. However, in order to continue reducing emissions, greater efforts are needed on the part of the State, public authorities, and private actors.

The transport sector has also been part of the « effort sharing » sectors of European climate policy since 2013, meaning that reducing emissions is the responsibility of each Member State, while the European Commission only sets annual caps for these emissions. This sector is therefore not covered by the carbon market, established by the EU in 2005, which consists of a quota system to control and reduce CO2 emissions. Vehicle emissions depend mainly on three factors: total distance traveled, number of passengers, and type of fuel used. In 2015, the government launched the National Low-Carbon Strategy (SNBC), which aims to eliminate all emissions from the transport sector (except air transport) by 2050.

Figure 2: Evolution of GHG emissions between 1990 and 2018 and SNCB trajectories

The main levers for action include: decarbonization of energy consumption, optimization of vehicle use, use of lower-emission means of transport, and total conversion to new technologies (electric or hydrogen fuel cell cars).

With this in mind, this note presents demand-side policies that have already been tested to encourage the purchase of less polluting vehicles (particularly in the case of diesel), followed by supply-side solutions that facilitate the deployment of hydrogen applications in the transport sector in France.

2. Demand-side instruments inspired by the case of diesel

In the past, several public policies have attempted, on the one hand, to reduce private car travel and, on the other hand, to encourage the purchase of low-emission vehicles (particularly diesel vehicles). There is thus a variety of instruments that can be used to reduce the use of polluting vehicles by influencing prices or quantities.

Instruments that affect prices include taxes and subsidies. For example, Durrmeyer (2018) studies the effects of the 2003 ecological « bonus-malus » system on the purchase of diesel vehicles[6]. This environmental policy consists of encouraging the purchase of « clean » vehicles with a subsidy or « bonus » of €1,000 and discouraging the purchase of polluting vehicles with a tax or « penalty » of €2,600. The result is a reduction in CO2 emissions for newly registered vehicles, but an increase in overall CO2 emissions. This is the result of two effects:

- On the one hand, the subsidy has led to an increase in demand for (French) diesel vehicles, but also in overall demand for vehicles.

- On the other hand, these diesel vehicles appear to be used more than their more polluting counterparts.

Currently, Article 18 of the 2020 Finance Bill presented to the National Assembly proposes to modify this policy by increasing various thresholds and including several types of vehicles. Since 2015, a bonus of €10,000 has been available for electric vehicles. Given the results of this policy, it could be extended to hydrogen fuel cell vehicles in order to encourage consumers to purchase them.

Another example is taxes on gasoline or CO2 emissions, which seek to reduce the use of polluting vehicles and thus CO2 emissions. These gasoline taxes are defined by Allcott and Wozny (2014) as energy taxes that directly affect vehicle usage by reducing it. Furthermore, if the consumers concerned are « forward-looking »[7], then this type of tax could affect their purchasing decisions (Grigolon et al, 2018). However, consumers are not always « forward-looking » and may be « myopic » (Allcott and Greenstone, 2012). In this case, a better alternative is to opt for product taxes or subsidies to encourage the purchase of low-emission vehicles. However, there is no consensus in the economic literature on the degree of consumer myopia. However, Grigolon et al (2018) highlight that high-mileage consumers would be more responsive to energy taxes. These types of taxes effectively increase the price of gasoline and do not seem to be well accepted socially, as illustrated by the « yellow vest crisis » in France.

In terms of instruments that affect quantities, there are restricted traffic zones (RTZs). These are areas in which access is restricted during certain time slots. However, these access restrictions can have « perverse » effects: Barahona et al (2019) show that in the case of a uniform restriction[8], they can lead to the purchase of a second polluting vehicle. This extends the life expectancy of old polluting vehicles. Restrictions based on pollution levels or « vintage » restrictions therefore seem to be more appropriate for encouraging the transition to less polluting alternatives. In 2015, Paris introduced its first restricted traffic zone (ZCR) for heavy goods vehicles, which was extended in 2016 to all vehicles manufactured before 1997. In France, it is planned that by 2020, 15 territories will have low-emission zones (LEZs), i.e., vintage restriction zones.

Barahona et al (2019) define the optimal policy mix for the transition to an emission-free vehicle fleet: a combination of subsidies for non-polluting vehicles and vintage traffic restrictions. To benefit from synergies between the various market players, it is necessary to agree on the vehicle fleet towards which we want to converge.

The results of all the instruments mentioned, used in the case of diesel, seem to be rather positive, facilitating the transition to a lower-emission vehicle fleet. Nevertheless, diesel remains a CO2-emitting vehicle, having also lost a great deal of popularity following the revelation of the Volkswagen Group’s falsified emission levels[9]. To achieve the SNBC’s objectives, these instruments must therefore be geared towards low-emission vehicles such as combustion engine, electric, or fuel cell (hydrogen) vehicles.

3. A willingness to cooperate in the deployment of hydrogen: supply-side instruments

Low-emission vehicles include hybrid, electric, and fuel cell (hydrogen) vehicles. Hybrid vehicles run on multiple energy sources, such as electricity combined with gasoline or diesel, which are CO2 emitters. Therefore, the strategy for decarbonizing the transport sector will rely primarily on fully electric vehicles (EVs) or hydrogen fuel cell vehicles (HFCVs). Moreover, these vehicles offer a considerable advantage over biofuels, eliminating constraints on access to resources or competition for land use.

Hydrogen fuel cell (HFC) vehicles run on electricity produced from hydrogen stored in a tank. They are electric cars that produce their own electricity and emit only water vapor into the atmosphere. According to the IEA (2019), HEVs offer two advantages over EVs. On the one hand, they have a range[10] of over 400 km, compared to 250 km for EVs. On the other hand, they have a short recharge time, similar to that of a fossil fuel vehicle. For EVs, the recharge time is 30 minutes at a fast charging station, while at a home charging station it can take up to 10 hours (Engie, 2016). EVs therefore seem to be more suitable for users with low mileage, while PAHs offer more advantages for high-mileage journeys (e.g., road transport). These two technologies are therefore not competitors, but complementary.

However, both types of vehicles face two types of barriers: the price of the vehicle and the limited number of charging stations. The price of zero-emission vehicles remains high today, as low demand prevents manufacturers from benefiting from economies of scale. On the other hand, the low number of charging stations is also the result of the limited number of vehicles on the road. Consumers will therefore only buy this type of vehicle if there is a minimum number of charging stations, the deployment of which depends on a level of demand that covers their cost (Kotelnikova, 2016).

There are two strategies for resolving this dilemma: deployment by « cluster »[12] and subsidies for charging stations. In order to propose public policies that are consistent with low-carbon mobility projects, it is necessary to agree on the type of vehicle fleet we want to converge towards.

With regard to passenger vehicles, public policies for decarbonizing the sector mainly benefit electric vehicles. Indeed, the Mobility Orientation Bill (2019) proposes subsidies for the installation of charging stations. As charging times are significant, recharging is mainly done at home or at work (Mobility Orientation Bill, 2019). In France, this applies to 90% of charging stations. The Mobility Orientation Bill proposes an energy transition tax credit (CITE), seeking to reduce the cost of home installation. However, other players, such as shopping centers, could also install charging stations (Colesanti Senni and Reidt, 2019), allowing them to benefit from network externalities: consumers would come to recharge their cars while they shop.

With regard to heavy-duty vehicles, public policies focus on the deployment of PAHs. For example, in France, the « Hydrogen Deployment Plan for Energy Transition, » launched by Nicolas Hulot in 2018, focuses primarily on the deployment of captive fleets, benefiting from state and EU subsidies. A captive fleet is a group of vehicles that make regular trips with predictable patterns, so a limited number of stations can provide recharging. What’s more, with heavy-duty vehicles, the station supplying them can be highly profitable due to the high demand for hydrogen.

Current projects are focused on niche markets where various players have shown a willingness to embrace the early deployment of hydrogen. For example, in the public transport sector, there are two major EU-funded projects: « Joint Initiative for Hydrogen Vehicles across Europe » and « 3emotions. » The aim is to develop the commercialization of the first hydrogen buses, in line with the objectives of the Energy Transition Law, which requires a shift towards low-carbon vehicles when renewing public transport fleets from 2020 onwards. In terms of captive professional fleets, there are projects such as Hype (the first fleet of hydrogen taxis) and Zero Emission Valley (a cluster of captive fleets). The latter, located in the Auvergne-Rhônes-Alpes region, with 80% of French players in the hydrogen sector, benefits from synergies between agents. Indeed, along the value chain, there is genuine cooperation between very large historical players and start-ups. Its objective is to offer renewable hydrogen at a cost similar to diesel.

To extend the use of PAH vehicles beyond captive fleets in road and urban transport, various public and private players will need to provide consumers with financial and non-financial incentives. The possible financial instruments used in the case of diesel and mentioned in section 1 are: energy taxes, product taxes, and vintage restrictions. Other possible financial instruments include reductions in tolls and parking fees. One non-financial instrument is the introduction of free public transport (e.g., Niort).

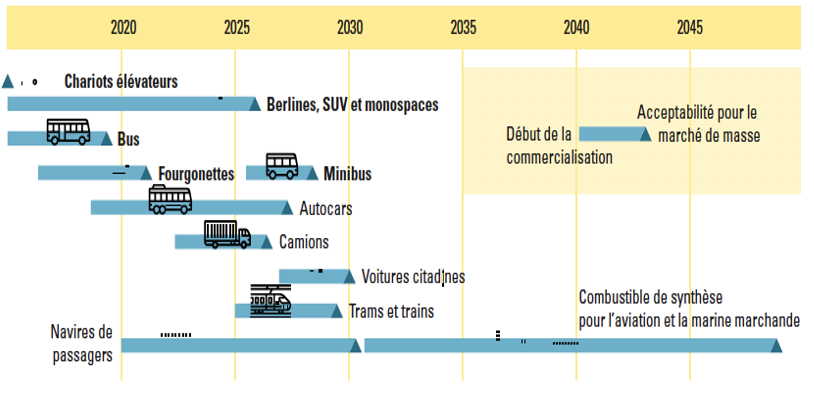

Hydrogen applications for rail, maritime, and air transport are currently being studied or tested. For example, in the aeronautics sector, Airbus is currently studying the adoption of hydrogen solutions (World Energy Council, 2019), but these will only be viable if the price of hydrogen is low enough. However, fleet renewal cycles for these types of transport are slightly longer than those for road transport. So even with technological expertise and a low hydrogen price, we will have to wait a little longer.

Figure 3: Hydrogen mobility deployment schedule in France

Source: AFHYPAC (2018)

Hydrogen as a mobility solution is on its way. Cooperation between public and private actors seems to be helping to overcome barriers in this market. However, the deployment of certain technologies requires more time than others, as fleet renewal cycles are not the same for road, rail, air, and maritime transport. Players in these markets must be patient and continue to invest and collaborate to achieve a competitive market.

Conclusion

In France, the transport sector is the leading source of GHG emissions and contributes significantly to air pollution. Technological solutions to decarbonize this sector exist but are struggling to enter the market. In order to enable a real transition in the transport sector, action must be taken on both supply and demand. On the demand side, effective instruments already used for the adoption of diesel exist. On the supply side, cluster deployment, accompanied by subsidies, seems to be a good solution.

However, fully electric and hydrogen-powered vehicles will only be truly emission-free if the electricity or hydrogen used comes from a renewable energy source. Otherwise, they will contribute to increasing emissions from the energy sector. It remains difficult for consumers to trace the exact origin of the electricity used to power these vehicles. Public authorities should therefore propose a way of effectively tracing whether the electricity or hydrogen comes from a renewable source.

In the case of electric vehicles, when recharging, especially at home, consumers will be limited by dynamic electricity rates. Indeed, as part of the energy transition, the price of electricity will converge towards a price that varies according to actual energy production. It could therefore become quite expensive to recharge your car, given the long recharge time.

With regard to hydrogen vehicles, the cooperation between various private players, which is currently accelerating the deployment of this technology, should not go unnoticed by the competition authorities. Once the market is sufficiently developed, these « benevolent » players could continue to hold far too much market power. However, this remains an issue to be revisited in a few years’ time.

References

ADEME. (2018).Improving performance and successfully transitioning to eco-mobility for public and private decision-makers.

AFHYPAC. (2016). Hydrogen programs in France.

AFHYPAC. (2018). Deploying hydrogen stations in your region.

Allcott, H., Greenstone, M. (2012). Is There an Energy Efficiency Gap?, Journal of Economic Perspectives, 26 (1): 3-28.

Allcott, H., Wozny, N. (2014). Gasoline Prices, Fuel Economy, and the Energy Paradox, The Review of Economics and Statistics, MIT Press, vol. 96(5), pages 779-795,

National Assembly. (2019). 2020 Finance Bill.

National Assembly. (2019). Draft Mobility Policy Bill.

Barahona, N., Gallego, F., Montero, JP. (2018). Vintage-Specific Driving Restrictions, The Review of Economic Studies. https://doi.org/10.1093/restud/rdz031

Citepa. (2019). Secten Report. (Data)

Colesanti Senni, C., Reidt, N. (2019). Transport policies in a two-sided market, Working Paper ETH Zurich.

Durrmeyer, I. (2018). Winners and Losers: The Distributional Effects of the French Feebate on the Automobile Market, TSE Working Paper, n. 18-950.

EEA. (2018). Greenhouse gas emissions from transport in Europe. (Data)

Engie. (2016). How do I charge my electric car?

Grigolon, L., Reynaert, M., Verboven, F. (2018). Consumer Valuation of Fuel Costs and Tax Policy: Evidence from the European Car Market, American Economic Journal: Economic Policy, 10 (3): 193-225.

Insee. (2016). (Data).

International Energy Agency. (2019).The Future of Hydrogen: Seizing today’s opportunities.

HyLAW. (2019).EU Policy Paper.

Kotelnikova. (2016).Analysis of a hydrogen-based transport system and the role of public policy in the transition to a decarbonized economy, Doctoral thesis, Paris-Saclay University.

Ministry for Ecological and Solidarity Transition. (2018).Hydrogen deployment plan for energy transition.

Ministry for Ecological and Solidarity Transition. (2019).Key transport figures.

Ministry of Ecological and Solidarity Transition. (2018). Draft National Low-Carbon Strategy: The ecological and solidarity transition towards carbon neutrality.

Electricity Industry Observatory. (2017). Transport-related air pollution.

World Energy Council. (2019). New hydrogen economy—hope or hype?

[1]The UN estimates that the world population will reach 9.8 billion by 2050.

[2]Key transport figures for 2019

[3]Ministry for Ecological and Solidarity Transition

[4]Encourage carpooling, limit business travel, and implement teleworking.

[5]Public transportation or bicycles

[6]At the time, these were considered a less polluting alternative to gasoline-powered vehicles.

[7]Take into account the future price of gasoline when purchasing a vehicle

[8]That is, without taking into account the level of vehicle emissions

[9]In September 2015, an investigation was launched by the Ministry of the Environment into this issue.

[10]Corresponds to the distance that can be traveled when the energy tank is at maximum capacity.

[11]Three minutes according to the Hydrogen Deployment Plan for Energy Transition.

[12]Multi-client captive fleets around a defined area and one or more service stations (Afhypac).