Usefulness of the article: The public consultation on pension reform invites French citizens to express their views on the direction they would like to see their future pension system take. Before deciding on the direction to take, it is important to understand where we have come from. This article aims to report on the changes that France has undergone in this area over the past half-century.

Summary:

-

The current pension financing system is threatened by at least four changes:

-

the explosion in the number of retirees;

-

the lengthening of retirement;

-

the increase in contributions from the working population; and

-

improvements in the standard of living of senior citizens.

© Monica Silvestre – Free to use

The government’s public consultation on pensions invites French citizens to express their views on the overhaul of one of the pillars of their social model. Some see it as an alarming increase in the pension system deficit, while others view it as a government maneuver to move toward a capitalization system. Many citizens are already engaged in heated debate, without always bearing in mind the profound changes that have been shaping French society for several decades. Here is a look back at four of these recent developments that are prompting the government to defend a reform that is considered unpopular by many professions.

Explosion in the number of retirees

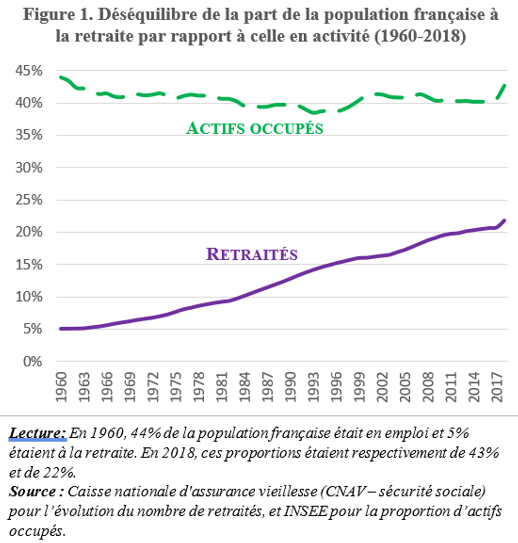

In terms of pensions, France today bears little resemblance to the France of a few decades ago. In 2019, there were more than 14 million recipients of pensions from the general scheme in mainland France (the number of direct (contributors) or derivative (spouses) retirees in France and abroad stands at 17.2 million). This means that there are twice as many retirees as in 1989, four times as many as in 1972, and six times as many as in 1960[1]. In 1960s France, one in twenty French people were retired, compared to one in four today.

This dramatic demographic change is illustrated in Figure 1, which shows that while the proportion of the working population in mainland France has remained broadly unchanged, the proportion of retirees has exploded, rising from 5% in 1960 to 22% today.

As a result, the burden of financing the pension system on the shoulders of the working population is at an all-time high. The contributor-to-retiree ratio, which compares the number of working people financing pensions to the number of retirees, is one of the most unbalanced in the world: only 1.7 people in employment for every retiree with direct entitlement (all schemes combined) [2].

This contributor-to-retiree ratio is projected to continue to decline, reaching 1.5 working contributors per retiree in 2040. Contrary to popular belief, this situation is not solely the result of the baby boom. By 2070, after the baby boom generation has retired, the number of contributors per retiree is expected to fall to 1.3. France is certainly the country where the post-World War II baby boom was the highest in Europe, but the baby boom was even more vigorous in the United States. Yet that country currently has three working people per retiree. With such a ratio, the burden on French workers would be almost half as heavy. Among the causes of this gap, which include immigration and unemployment (8.6% in France compared to 3.6% in the United States), it is noteworthy that French people have a life expectancy at age 60 that exceeds that of Americans by more than two years, but retire six years earlier.

Longer retirement

Not only is the number of retirees skyrocketing, but retirement periods are now much longer. This is because the life expectancy of seniors is increasing rapidly while the retirement age remains stagnant. In 1968, French people retired at age 64. At that time, life expectancy at age 60 was 16 years for men and 20 years for women. Today, French people are generally retiring two years earlier (the minimum retirement age is set at 62 and the actual age is 61.7 due to early retirement schemes), and life expectancy at age 60 has increased by seven years (for both men and women) [5].

The fact that the number of years spent in retirement has increased by nine years in half a century is excellent news. France thus holds the record for the amount of time spent in retirement among developed countries [6]. With an expected duration of around 25 years for new retirees, this exceeds the average for other OECD countries by five years and that of other European countries by six years.

Increased burden on the working population

As might be expected, the cost of this system weighs heavily on the shoulders of the working population. Social security contributions to finance pensions increase the cost of labor and weigh on unemployment to such an extent that France is one of a small group of European countries that have still not regained their pre-crisis employment momentum (along with Greece, Spain, and Italy). Social security contributions also erode the purchasing power of workers much more significantly than other compulsory levies (VAT, CSG, income tax, etc.).

An employee on the minimum wage pays the equivalent of a quarter of their total salary (net salary plus employee and employer contributions) in social security contributions. This proportion rises rapidly with salary. A school teacher with five years’ seniority (whose net salary is €1,750) pays the equivalent of their net salary solely to finance pensions. A certified teacher at the end of their career (whose net salary is €2,900) pays more than €3,000 per month into pension funds [7].

Improved standard of living for retirees

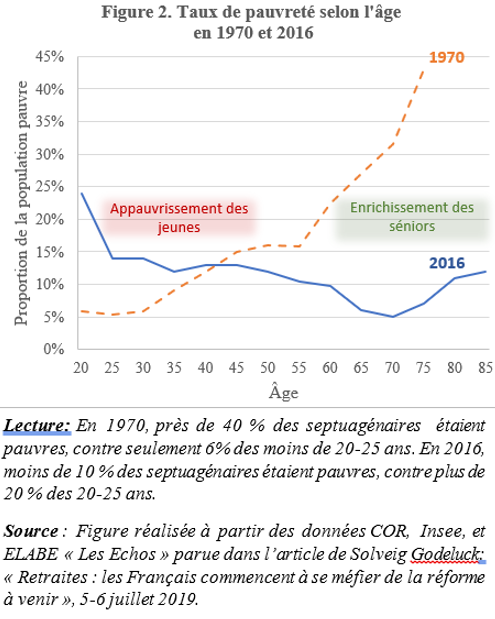

Current pensions also offer a more comfortable standard of living than in the past. In the 1970s, the older people were, the more they were exposed to poverty. This phenomenon is illustrated in Figure 2, which shows the proportion of the French population considered poor according to age. The hatched curve for 1970 depicts the grim reality of the time: around 40% of people in their seventies were poor. Their situation has improved considerably since then, with less than 10% living in poverty in 2016, as shown by the second curve (solid line).

Our current system is a legacy of the concerns of that era, when there was an urgent need to strengthen solidarity between generations. This solidarity has since taken an unexpected turn. The standard of living of retirees has not only caught up with that of the working population, it has surpassed it (by 6 to 7%). Today, less than 8% of people in their seventies are poor, compared to more than 20% of 20-25 year olds, whose unemployment rate has increased fivefold (from less than 4% in 1970 to more than 20% today). Three-quarters of retirees own their primary residence, compared to less than half of non-retirees. They bought cheaper properties and have already paid off their mortgages. As a result, their wealth is greater and is growing faster than that of the rest of the population.

Many young retiree households have two respectable pensions. This was uncommon in the days when women’s access to the labor market was restricted.

However, not all seniors are wealthy. The minimum old-age pension (a solidarity measure that will reach €900 in 2020, or 79% of the poverty line) still benefits more than half a million of the 17.2 million retirees with direct or derived rights.

Conclusion

Our pay-as-you-go system has already been watered down to the point where employee and employer contributions now finance only two-thirds of pensions. The remaining third, as well as the Old Age Solidarity Fund, are financed by the CSG and other various taxes. The burden on taxpayers is constantly increasing and, quite legitimately, many citizens are sensitive to the overhaul of a pension system that absorbs more than a quarter of annual public spending, which is more than health insurance and more than four times the budget for sovereign functions (defense, security, justice) [8].

Whether for or against the reform proposed by the current government, everyone should be able to express their opinion. But it would be wise to do so with an awareness of recent changes, such as the explosion in the number of retirees, the lengthening of retirement, the increase in contributions from the working population, and the improvement in the standard of living of senior citizens.

Author: Jérôme Mathis is a professor of economics at Paris-Dauphine University and author of the blog La Finance au cœur de nos vies(Finance at the heart of our lives).

References

[1] Source: National Old Age Insurance Fund (CNAV – social security). Change in the number of retirees in mainland France by payment fund (1960-2018).

[2] Annual report of the Pension Advisory Council: « Évolutions et perspectives des retraites en France » (Pension trends and outlook in France), June 2017. See Figure 2.2b – « Ratio of contributors to retirees, » p. 60.

[3] General Secretariat of the Pension Advisory Council (2019): « Historical and projected changes in the retirement age, » Working Paper No. 4.

[4] Aline Désesquelles (2011): « Demographic aging in France: current situation, trends, and comparison with some European neighbors, » INED

[5] General Secretariat of the Pension Advisory Council (2019): « Recent changes in life expectancy in France, » Working Paper No. 9.

[6] General Secretariat of the Pension Advisory Council (2019): « International overview of effective retirement ages, » Working Paper No. 11, Figure 4. « Average expected duration of retirement, » p. 6; and OECD (2018): « Pension Panorama 2017. » Graph 1.6. « Average effective age of exit from the labor market by country, » p.4.

[7] Net salaries are expressed here before income tax. According to the French Ministry of Education scale, a senior teacher in the fifth grade (salary index 756) receives a net salary of €2,872 before income tax. Their pension contributions are €3,014 (€383 in employee pension contributions and €2,631 in employer pension contributions).

[8] Eurostat, calculations by the Directorate General of the Treasury (2019): « Taxation and public spending, » summary sheet prepared for the great national debate.