Usefulness of the article: Before municipal elections, voters may be tempted to compare the fiscal policies of different municipalities. This behavior creates complex incentives for local elected officials, which can make the policies of municipalities (and local authorities) interdependent. This article presents the mechanisms that create such interdependencies between fiscal policies, as well as some empirical studies focusing on France.

Abstract:

- Several mechanisms can create interdependence between the fiscal policies of local authorities. The mechanism highlighting the fact that voters can compare the performance of local elected officials in neighboring communities is sometimes highlighted in the literature.

- Numerous studies have documented the existence of these interdependencies. In France, for example, studies have detected them at the municipal, departmental, and regional levels.

- Without questioning the relevance of these mechanisms, recent studies have nevertheless cast doubt on previous empirical findings. These interdependencies may be weaker than previously estimated.

Tax competition between countries and its consequences are widely discussed in the media. Although it attracts less attention, such competition can also exist within countries, for example at the departmental or municipal level. Through their tax policies, local authorities may seek to attract wealthier businesses or residents. Economists generally address this issue by integrating it into the broader issue of the interdependence of local government tax policies. The question then is whether the tax policies of two « close » local authorities (e.g., two neighboring municipalities) will be more similar than those of two distant local authorities (e.g., two municipalities far apart), and to seek to understand the reasons for this.

The aim of this article is to briefly present this literature, highlighting some studies focused on France. The first part of this article summarizes the reasons why the tax policies of local authorities may be interdependent. Some empirical results are then presented in the second section. The conclusion qualifies the previous results, as the methodology used by economists to study these fiscal interdependencies has been partly called into question over the past decade.

Theoretical reasons

There is a vast body of theory highlighting the strategic dimension of the interdependencies between local government tax policies. [1] However, before examining this, it should be noted that non-strategic reasons can also lead to this result. Local taxes are primarily used to finance local public services (such as road construction and maintenance), and the cost of these services can be largely dependent on geographical factors that are relatively continuous in space. Two nearby municipalities (of similar size) will therefore have relatively similar public service costs, while two distant municipalities may have different costs. Consequently, the amount of taxes levied (and the tax rates voted) to finance these services will also be similar for nearby municipalities. A caricatural example can illustrate this situation: suppose we are interested in the taxes voted by four municipalities, two neighboring municipalities located in the Alps and two others located in Finistère. Furthermore, suppose that the only local public service considered is a road snow removal service. In this example, it seems obvious that the two Alpine municipalities will need this snow removal service and will therefore vote for local taxes high enough to finance it, while the two Breton municipalities will be able to do without it. Thus, although there is no strategic behavior in this example, the taxes of nearby municipalities will be at roughly equivalent levels.

This first « geographical » reason is reinforced by the very nature of local public goods, which can be consumed by people outside the community [2]. For example, if a municipality builds a municipal swimming pool, it will benefit not only the residents of that municipality, but also the residents of neighboring municipalities. Therefore, a community that wishes to provide the best service to its residents (or, in economic terms, maximize their utility) must take into account both the fact that the service may have been provided by nearby communities and the fact that residents of other communities may consume the local public good and lead to its congestion. This leads to a situation where the level of public spending by one community depends positively or negatively on that of its neighbors. Once again, the municipality’s taxation will partly reflect the public services offered, leading to interrelated tax policies among communities [3].

The third reason that can lead to correlated community tax policies is the mobility of the tax base. Certain actors, particularly the wealthiest businesses or households, may choose their location or place of residence based on local taxes. This possibility (generally associated with Tiebout, 1956), usually summarized by the expression « voting with your feet, » would lead neighboring communities to choose relatively similar tax levels so as not to be deserted in favor of their neighbors [4]. Although rarely highlighted in Europe, this explanatory mechanism is relatively popular in the United States, where populations are more mobile [5].

Finally, a last explanatory mechanism can be put forward, this time based on information asymmetries between politicians and voters [6]. Suppose that voters in a municipality know less than mayors about the real costs of local public services. Let us also assume that some « bad » politicians may wish to « divert » part of the local taxes or, at the very least, not make the necessary efforts to finance public goods at the lowest cost (for a given quality). This situation gives rise to complex strategies on the part of « bad » politicians who want to both « extract » as much money as possible by raising taxes and maintain a reputation as « good » politicians so they can be re-elected. The ability of « bad » politicians to divert part of the taxes will depend crucially on the information available to voters. However, for a « bad » politician, convincing their electorate that they are a « good » one is more difficult when voters are able to compare their elected representative with another in a similar jurisdiction. Consider, for example, two mayors of neighboring and relatively similar municipalities; if one levies low local taxes while the other chooses a high tax rate, then the residents of the second municipality may think that they are being led by an ineffective mayor. This mechanism (known as yardstick competition ) can lead local elected officials to align themselves with each other on local taxes for fear of being considered « bad » politicians.

Some empirical facts

These different mechanisms have led researchers to study the level of taxation of local authorities and to determine whether it depends on that of neighboring authorities. Methodologically, authors often use spatial econometric tools [7] because they allow them to directly estimate empirical models where the level of taxation of one authority is explained by that of its neighbors.

Several studies have examined the French case and concluded that there is a form of positive spatial autocorrelation (i.e., the tax level of a local authority evolves in a similar way to that of neighboring local authorities) at the municipal level (Jayet et al., 2002; for municipalities in Nord-Pas de Calais), departmental (Leprince et al., 2005) and regional (Feld et al., 2002) levels.

Two other studies, both focused on the departmental level, shed further light on this issue of the interdependence of fiscal policies by highlighting the importance of political factors. First, Dubois et al. (2007) explain that, despite strategic interactions, political competition and the partisan sensibilities of politicians continue to play an important role. Second, Elhorst and Fréret (2009) show that spatial interaction between departments is itself a function of political competition. This latter finding suggests the importance of the last explanatory mechanism (yardstick competition) as a source of these interdependencies, since it is the most dependent on the degree of political competition within local authorities.

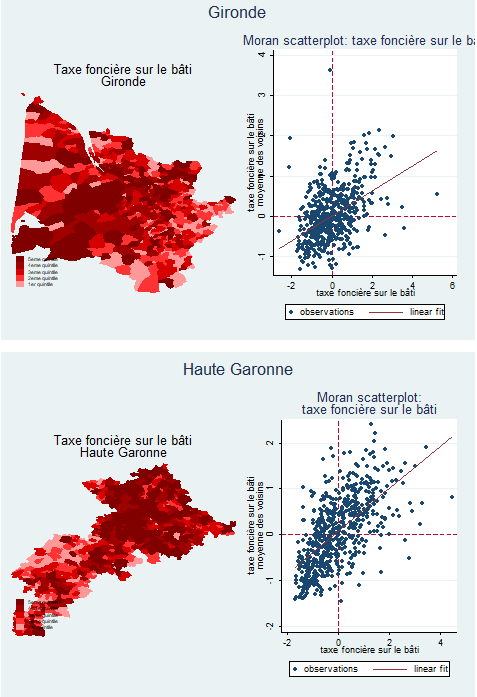

Is there still a form of interdependence between the tax rates chosen by municipalities today? Without going so far as to reproduce the above studies, it is possible to explore graphically the presence of spatial autocorrelation and, therefore, perhaps, strategic interdependencies in tax levels. One way to do this is simply to draw a map and color the municipalities according to their tax level (for example, the 2019 property tax rate). We can then see whether the lightest points (municipalities with low tax levels) are close to each other and whether the same phenomenon is apparent for the darkest points (municipalities with the highest tax rates). Another methodology is to plot Moran’s map. This involves placing the municipalities on a grid where the x-axis ranks the municipalities according to the level of property tax on buildings[9]. The y-axis indicates the average property tax rate in the municipalities neighboring the municipality in question. By doing so, it is possible to construct a graph where it is easy to see whether municipalities with high tax rates are surrounded by municipalities that, on average, also choose a high tax rate.

The following graph illustrates these methodologies for the department of Yvelines. This choice is purely arbitrary, and similar graphs can be found in the appendix for Bouches-du-Rhône, Haute-Garonne, and Gironde. Moran’s map and graph reveal positive spatial autocorrelation. The municipalities with the highest tax rates seem to be concentrated in the east and north of the department. Although it is impossible to test the mechanisms at work with this type of analysis, the interdependencies of fiscal policies cannot be ruled out.

Conclusion

At the end of this article, it appears that several mechanisms can explain the similarity of tax rates between local authorities. At the local level, however, one explanatory mechanism seems to emerge: yardstick competition, or the idea that voters can « gauge » the performance of elected officials by comparing their decisions to those of their neighbors. For the politicians concerned, particularly when political competition is intense, this would create incentives to align themselves with the decisions of neighboring local authorities.

However, a word of caution is in order. The empirical methods used in this literature have recently been criticized (see, in particular: Gibbons, S. and Overman; 2012). Therefore, while the correlations identified are real, it is difficult to rule out the possibility that they may ultimately be due to unobserved factors [11]. Furthermore, one of the few studies that attempts to take these methodological criticisms into account (Lyytikäinen; 2012) [12] seems to conclude that there is little or no interdependence between the local taxes set by Finnish municipalities.

Therefore, while fiscal interdependencies may be real, they remain difficult to measure. Furthermore, they are not necessarily limited to competition between local authorities to attract wealthy households or businesses. Many mechanisms, sometimes involving the interests and strategies of local elected officials, may explain these interdependencies.

References

Timothy Besley and Anne Case. “Incumbent Behavior: Vote-Seeking, Tax-Setting, and Yardstick Competition.” The American Economic Review, 1995 vol. 85, no. 1, 1995, pp. 25–45.

www.jstor.org/stable/2117994

Jan K. Brueckner and Luz A. Saavedra. “Do Local Governments Engage in Strategic Property—Tax Competition?” National Tax Journal, 2001, vol. 54, no. 2, pp. 203–229.

www.jstor.org/stable/41789546

Dubois, E., Leprince, M., & Paty, S. The Effects of Politics on Local Tax Setting: Evidence from France. Urban Studies, 2007, 44(8), 1603–1618.

https://doi.org/10.1080/00420980701373487

Elhorst, J.P. and Fréret, S., Evidence of political yardstick competition in France using a two-regime spatial Durbin model with fixed effects, Journal of Regional Science, 2009, 49, pp931-951.

https://onlinelibrary.wiley.com/action/showCitFormats?doi=10.1111%2Fj.1467-9787.2009.00613.x

Marcel Gérard, Hubert Jayet, and Sonia Paty, Tax interactions among Belgian municipalities: Do interregional differences matter?, Regional Science and Urban Economics, 2010, Volume 40, Issue 5, pages 336-342.

http://www.sciencedirect.com/science/article/pii/S0166046210000190

Gibbons, S. and Overman, H.G., Mostly pointless spatial econometrics? Journal of Regional Science, 2012, 52: 172-191

https://onlinelibrary.wiley.com/doi/full/10.1111/j.1467-9787.2012.00760.x

Jayet Hubert, Paty Sonia, Pentel Alain, « Are there strategic fiscal interactions between local authorities? », Économie & prévision, 2002/3 (no. 154), pp. 95-105.

https://www.cairn.info/revue-economie-et-prevision-2002-3-page-95.htm

Feld Lars, Josselin Jean-Michel, Rocaboy Yvon, « Fiscal mimicry: an application to French regions, » Économie & prévision, 2002/5 (no. 156), pp. 43-49.

https://www.cairn.info/revue-economie-et-prevision-2002-5-page-43.htm

Matthieu Leprince, Sonia Paty, and Emmanuelle Reulier, « Taxation choices and spatial interactions between local authorities: A test on French departments, » Recherches économiques de Louvain, 2005, Volume 71(1), pp. 67-93.

https://www.cairn.info/revue-recherches-economiques-de-louvain-2005-1-page-67.htm?contenu=article

Teemu Lyytikäinen, Tax competition among local governments: Evidence from a property tax reform in Finland, Journal of Public Economics, 2012, Volume 96, Issues 7–8, pages 584-595.

http://www.sciencedirect.com/science/article/pii/S0047272712000230

Ronan Le Saout and Jean-Michel Floch, « Spatial econometrics: a practical introduction, » INSEE, working paper , 2016.

https://www.insee.fr/fr/statistiques/2408659

Thierry Madiès, « Tax competition between local authorities. Tax competition and horizontal and vertical externalities: a framework for understanding strategic behavior between local authorities, » Regards croisés sur l’économie, 2007/1 (no. 1), pp. 218-230.

10.3917/rce.001.0218. URL: https://www.cairn.info/revue-regards-croises-sur-l-economie-2007-1-page-218.htm

Albert Solé-Ollé, “Expenditure spillovers and fiscal interactions: Empirical evidence from local governments in Spain,” Journal of Urban Economics, 2006, Volume 59, Issue 1, pp. 32-53.

http://www.sciencedirect.com/science/article/pii/S0094119005000604

Charles M. Tiebout, “A Pure Theory of Local Expenditures.” Journal of Political Economy, 1956, vol. 64, no. 5, pp. 416–424.

www.jstor.org/stable/1826343

[1] Madiès (2007) also provides an introduction to this literature, focusing on the French case. He also examines vertical interactions, for example between municipalities and intermunicipal bodies, between municipalities and departments, etc.

[2] This paragraph is based in particular on Solé-Ollé (2006).

[3] It should be noted that in this case, the policies implemented are not necessarily effective from the point of view of society as a whole. This may provide a theoretical justification for the creation of inter-municipal bodies.

[4] Although Tiebout’s theory (1956) is not limited to the idea of tax competition alone, in the present discussion, the mechanism developed functions in a manner quite similar to those more widely publicized on tax competition between countries.

[5] Brueckner and Saavedra (2001) present a theoretical model to illustrate this type of mechanism. Furthermore, an article published on the Forbes website presents tax competition between cities as one of the main reasons why New York City is losing residents: Jack Kelly, « New Yorkers Are Leaving The City In Droves: Here’s Why They’re Moving And Where They’re Going, » Forbes, September 2019.

https://www.forbes.com/sites/jackkelly/2019/09/05/new-yorkers-are-leaving-the-city-in-droves-heres-why-theyre-moving-and-where-theyre-going/#3ff6506741ac

[6] Generally speaking, information asymmetry means that one of the actors (in this case, the politician) has information that another actor (in this case, the voter) does not have. This paragraph is based on the model proposed by Besley and Case (1995).

[7] Spatial econometrics is a branch of econometrics that explicitly incorporates the spatial aspects of data. Ronan Le Saout and Jean-Michel Floch (2016) provide an introduction to these methods.

[8] France is obviously not the only country studied. See, for example, Brueckner and Saavedra (2001) for a study of US data, Solé-Ollé (2006) for a case study of Spain, Gérard et al. (2010) for a study of Belgium, etc.

[9] More precisely, the variable « property tax rate on buildings » is centered and reduced.

[10] Once again, in practice, the centered and reduced variable is used instead.

[11] Poor control of geographical factors and voter preferences, for example, or changes in municipalities that researchers were unable to incorporate into their models.

[12] Lyytikäinen (2012) uses a tax reform to obtain « exogenous » variations in the tax levels of surrounding municipalities.