.jpg)

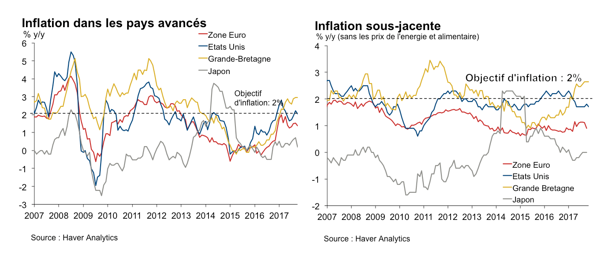

Thanks to accommodative monetary policies, the economies of advanced countries have returned to growth and employment. However, inflation remains low and well below central bank targets (Chart 1). Thus, contrary to the relationship highlighted by Phillips in 1958, a decline in unemployment would no longer lead to higher wages. This poses a problem for central banks such as the Fed, which use the Phillips relationship as one of their guides for conducting monetary policy. In principle, inflation should exceed the central bank’s target when the economy is overheating, indicating that monetary policy is too accommodative. If the Phillips curve has disappeared, how can we ensure that monetary policy does not lead the economy into an unsustainable dynamic?

Chart 1: Core inflation struggles to reach central bank targets

In this note, we observe that low inflation is partly linked to structural trends other than economic activity. Thus, despite historically low interest rates, inflation is likely to remain moderate in the medium term, prompting central banks to rethink their economic model as monetary policy normalizes.

How can low inflation be explained when unemployment is falling?

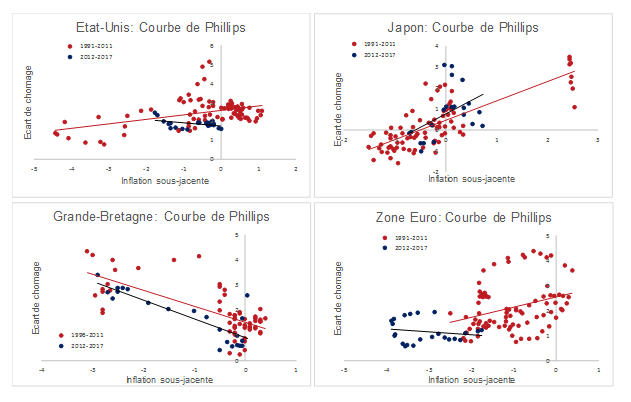

Since 2012, falling unemployment in advanced countries no longer seems to coincide with accelerating wages and inflation. The flattening of this relationship, represented by the Phillips curve, is particularly visible in the United States and the eurozone (Chart 2). For example, in the United States, for every one-point decrease in the gap between cyclical and structural unemployment, inflation now increases by only 0.2%, compared with 0.4% before the crisis. How can this trend be interpreted?

Chart 2: The flattening of the Phillips curve in advanced countries, particularly visible in the United States and the Eurozone

Source: OECD, national statistical institutes, and author’s calculations

Note: The unemployment gap refers to the deviation of cyclical unemployment from structural unemployment (NAIRU). A large gap indicates a tighter labor market, which, according to the Phillips relationship, should translate into inflationary pressures.

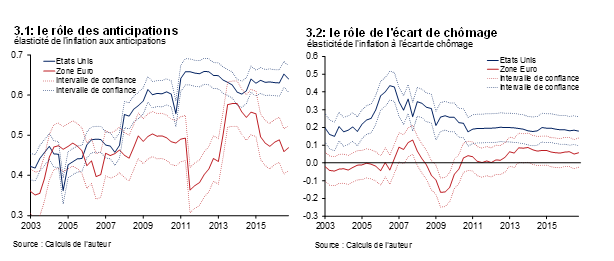

This phenomenon is linked to the fact that the Phillips curve disregards other determinants of price and unemployment dynamics. First, agents increasingly set their prices based on their inflation expectations (Figure 3.1), which are geared toward the central bank’s inflation target. As a result, they vary less with changes in the labor market.

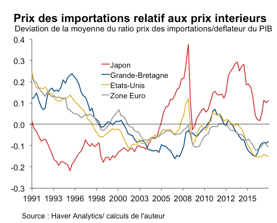

Second, globalization has a greater impact on price dynamics. With a growing share of imported products, price competition and competition between companies and employees is increasingly defined at the international level. As a result, domestic inflation has become more dependent on the global economic cycle. Since the 1990s, import prices have risen on average relatively less quickly than domestic prices (Chart 4), thereby exerting downward pressure on inflation.

Chart 3: Determinants of the Phillips curve: better anchoring of expectations and a weak response of inflation to changes in unemployment

Reading note: We study the determinants of the Phillips curve by estimating inflation based on inflation expectations, the unemployment gap, and import prices relative to domestic prices (a simplified version of the one used by Blanchard 2016). The graphs above show that elasticities (or coefficients) have changed since the 2000s. The higher elasticity of expectations today indicates a stronger impact on the observed inflation rate.

Figure 4: Import prices weigh on domestic inflation

Finally, in the labor market, employees in advanced countries appear to be in a less advantageous position to negotiate their wages. Globalization, technological progress, the increase in part-time work and precarious employment contracts (fixed-term contracts, temporary work, etc.), as well as a decline in union membership are factors that weigh on potential wage increases (IMF WEO 2017). Furthermore, the reduction in the unemployment rate is not following a trend opposite to economic growth. This is explained by an increase in labor force participation rates as people who left the labor market during the crisis return and retirements are postponed.

The flattening of the Phillips curve challenges prevailing analytical theories

Even if the Phillips curve relationship appears to exist when other measures of inflation or the unemployment gap are used (Borio 2017), the link between inflation and unemployment remains weak. This leads to two possible conclusions:

1. Either the imbalance between supply and demand remains too high to lead to higher prices;

2. Either the Phillips curve relationship is no longer able to identify economic imbalances.

To reach the first conclusion, we must consider the neo-Keynesian analysis that currently dominates economic thinking. In this framework, since monetary policy cannot influence long-term equilibrium, its role is to reduce fluctuations in economic cycles. Thus, monetary policy must set its interest rate as close as possible to the neutral rate, which balances savings and investment, in order to bring the economy as close as possible to its long-term trend. Consequently, if inflation is low, this simply indicates that the interest rates set by central banks are higher than the neutral equilibrium rates. A number of structural trends common to advanced countries explain the low equilibrium rates of return. An aging population, growing inequality, the relative price of capital, and low productivity gains would lead to a persistent imbalance between investment and savings (e.g., due to a savings surplus according to Bernanke 2005 or a problem of secular stagnation according to Summers 2014). Central banks would therefore simply need to keep interest rates low for longer to encourage economic agents to draw down their savings. In other words, the exit from accommodative monetary policies should be slow and gradual.

However, while this theoretical analysis seems to be justified by recent trends, it is no longer valid for long-term data and even seems to depend on the monetary regime (Borio et al. 2017). This leads us to our second conclusion: the Phillips curve is not a good guide for identifying economic imbalances and therefore for setting interest rates. If short-term policies influence long-term equilibrium (Blanchard 2017), then seeking to reduce cyclical fluctuations around long-term equilibrium could prove counterproductive, particularly in terms of financial stability (Borio 2017). This observation calls into question the New Keynesian analytical framework, the validity of the Phillips curve, and also the neutrality of monetary policy in the long term (Borio et al. 2017).

Conclusion: Low inflation would require the introduction of new variables to guide monetary policy

At first glance, low inflation in advanced countries suggests that the positive link between inflation and economic activity (the Phillips curve) has been broken. However, we see that better-anchored inflation expectations, globalization, and the decline in workers’ bargaining power are factors that have contributed to low inflation in recent years. This observation poses a headache for central banks at a time of monetary policy normalization. Should we expect a resurgence of inflation as the output gap narrows, or should we choose a theory other than the Phillips curve to justify monetary policy?

At present, central bankers still refer to an inflation target, and therefore more or less directly to the Phillips curve, as a guide for their monetary policy. The flattening of the Phillips curve can thus be explained by the position of the economy in the cycle. However, even if the Phillips curve remains relevant, it ignores financial stability, which is a crucial variable for the health of the economy. As the financial cycle currently appears to be more advanced than the economic cycle, this would suggest that the criteria on which monetary policy is based need to be reviewed.

Bibliography

Borio, C. (2017) « Through the Looking Glass, » OMFIF City Lecture, London, September 22, 2017.

Blanchard, O. (2017) « Should We Reject the Natural Rate Hypothesis? », PIIE, Working Paper 17-14, November 2017.

Blanchard, O. (2016) « The US Phillips Curve: Back to the 60s? », PIIE, Policy Brief No. PB16-1, January 2016.

IMF (2017) « Chapter 2: Recent Wage Dynamics in Advanced Economies: Drivers and Implications, » in World Economic Outlook, Seeking Sustainable Growth: Short-Term Recovery, Long-Term Challenges, IMF, October 2017.

Summers, L. (2014) « Reflections on the ‘new secular stagnation hypothesis’, » in C Teulings and R Baldwin (eds), Secular stagnation: facts, causes and cures, VoxEU.org eBook, CEPR Press.

Bernanke, B (2005): « The global saving glut and the US current account deficit, » Sandridge Lecture, Richmond, March 10.