DISCLAIMER: The opinions expressed by the author are personal and do not reflect those of the institution that employs him.

Summary:

- Climate risk has increasingly emerged as one of the main risks weighing on the current financial system, in line with the famous speech given in 2015 by the Governor of the Bank of England, Mark Carney, on the « tragedy of horizons »;

- In this context, public intervention is essential in order to align existing private initiatives with the climate change objectives set out in the Sustainable Development Goals and the Paris Agreement of December 2015.

- The role of the regulator (banking, insurance, and financial) is threefold: (i) to encourage the financial sector to finance the low-carbon transition; (ii) to compensate for the existing failure of financial institutions to understand and assess climate risk; and (iii) to align horizons in terms of risk management.

- Several initiatives, both at international and European level, have recently emerged and illustrate the need for an ambitious and coordinated approach between states in terms of sustainable finance, which distinguishes climate risk from other so-called ESG (environmental, social, and governance) risks.

Recognizing the systemic impact of climate risk, the role of regulators is both to promote incentives for financing the energy transition and to establish an adequate risk management framework for financial institutions. Recent international initiatives must now take stock of the colossal task of adapting financial regulations to climate change and achieving the objectives of the Paris Agreement, with a view to establishing a structured and incentive-based framework.

Since 1990, IPCC[1] publications have revealed both the accumulation of greenhouse gases in the atmosphere (i.e., a doubling of emissions since 1990) and the global warming this causes, with numerous consequences for the world’s economies, biodiversity, oceans, and soils. Societies have gradually become aware that a laissez-faire approach to climate change would cost humanity much more than the preventive measures required to control and reduce greenhouse gas emissions (provided, however, that these measures are designed to minimize the economic cost). Governments have therefore embarked on the path to low-carbon transition: not only with a view to limiting global warming to 2°C by 2100 compared to pre-industrial levels and achieving a carbon-neutral society in the second half ofthe 21st century (targets set by the Paris Agreement of December 2015), but also in order to limit the economic consequences of global warming.

In this context, climate change has financial implications for economic actors, particularly due to the potential deterioration in the financial performance of companies in many sectors (including, in particular, energy, real estate, and transportation) and the sharp decline in the value of financial securities linked to fossil fuels. The mutual reinforcement of the fragilities of the financial system and those caused by climate change has thus led the financial sector and regulators to take into account the emergence of systemic climate risk (Aglietta and Espagne, 2016)[3]. As a result, a number of private and public initiatives have recently emerged with a view to mitigating the effects of climate change on the financial sector and, at the same time, strengthening the latter’s role in financing the transition to alow-carbon economy. What role should the financial sector play in this context? What measures can be put in place to follow the 2°C trajectory of the Paris Agreement? What international cooperation is needed to achieve sustainable finance?

-

Climate change and the financial sector: a systemic challenge

The financial system has a dual role to play in the context of the low-carbon transition.

On the one hand, while one of the United Nations Sustainable Development Goals, which came into force in January 2016, focuses on measures to combat climate change, the Paris Agreement (see BSI Economics article: « COP21: between reality and illusion » ) to mobilize at least $100 billion per year by 2020 to meet the needs of developing countries. Such a mechanism should, in particular, help mitigate natural disasters linked to climate change. Finance must not only help to bridge the green investment gap needed to achieve the Paris Agreement’s objective, but also contribute to aligning financial flows with climate objectives (Article 2 of the Agreement).

Furthermore, it now appears necessary to take into account the impact of climate change on financial actors, which will translate into a range of risks (liquidity, credit, counterparty, market, and operational) that could potentially be significant (see the report on the assessment of climate change risks in the banking sector, published by the French Treasury in February 2017).

To the tragedy of the commons (Hardin, 1968), Mark Carney, Governor of the Bank of England and Chair of the Financial Stability Board, added a second tragedy in his speech entitled « The Tragedy of the Horizon » delivered in September 2015: that of « distant horizons.« These go far beyond the political timeframe or that of financial supervisors. In this sense, Mark Carney highlighted three ways in which climate change can undermine financial stability:

- Physical climate risks, i.e., the uncertain financial impacts on economic agents and asset portfolios resulting from the effects of extreme weather events (the frequency and intensity of which are set to increase exponentially) and from rising average temperatures and sea levels. The insurance sector is likely to remain the most affected by these risks (note that according to Swiss reinsurer Swiss Re, the cost of natural and man-made disasters in 2017 amounted to $337 billion, with insurers covering losses of nearly $144 billion).

- Transition risks, i.e., uncertain financial impacts, materializing in the form of a sudden revaluation of certain assets (or even their collapse: the « Minsky moment ») resulting from the effects of the implementation of a low-carbon economic model on economic agents (such as regulatory reforms and technological developments). These risks mainly affect sectors that are overly exposed to global warming or unprofitable in the context of its mitigation, i.e. , stranded assets (i.e., investments or assets that have depreciated in value due to market developments, particularly in the fossil fuel sector); and

- Litigation risks, i.e. the financial consequences of potential legal proceedings seeking to establish liability for climate change (including failure to take sufficient account of climate risks). For example, in January 2018, the city of New York sued five oil companies in federal court for their responsibility for climate change. On February 6, 2018, the Paris City Council decided to study the feasibility of suing oil companies, raising the question of the legal recognition of « climate crimes. »

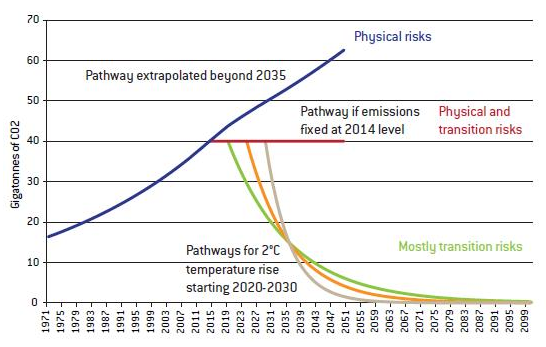

Climate risks according to greenhouse gas emission trajectories[6]

Source: Schoenmaker & van Tilburg (2016), UK Prudential Authority (2015)

The financial sector is thus gradually becoming aware of the systemic impact of climate change, which is both non-linear and unpredictable. First, the major public financial institutions (European Investment Bank; European Bank for Reconstruction and Development; Caisse des Dépôts), then the UNEP Finance Initiative[7] and the financial institutions themselves have taken up the issue. Noteworthy developments include the rise of green bonds; the divestment movement from certain fossil fuels; exponential investment in renewable energies; the creation of green investment funds; the rise of socially responsible investment; the » Finance for Tomorrow » initiative launched by the Paris Financial Center in June 2017; etc.). Establishing a « green » financial system now involves a range of fundamental challenges (pursuing sustainable economic growth; addressing systemic climate risk; responding to investor expectations; and, more anecdotally, the issue of competitiveness among global financial centers; etc.).

2. What role does financial regulation play in the context of a low-carbon economic transition?

In this context, financial regulation plays a key role: it is not only a question of reconciling horizons (i.e., the short-term horizon of the financial sector, the medium-term horizon of the regulator, and the long-term horizon of the climate), but also of providing the financial sector with the tools to redirect capital in order to increase the profitability of green assets and improve understanding of climate-related risks.

As described by the Governor of the Bank of France, François Villeroy de Galhau, in a speech delivered ahead of COP21 in November 2015, public intervention is threefold in order to align the private initiatives described above with the fight against global warming. It involves:

- encourage the financing of the low-carbon transition, in particular by redirecting long-term savings. What is the role of prudential regulation? Of asset management and investment advice regulation?

- compensating for the current market failure represented by a lack of awareness of climate-related risks. In this sense, the role of information is crucial, in line with the strengthening of requirements for the disclosure of environmental risks permitted by Article 173 of the French Energy Transition Law, promulgated in August 2015; and

- to reconcile the medium- and long-term time horizon of climate change with the risk management of financial institutions, in particular by implementing climate stress tests in the banking, insurance, asset management, and market infrastructure sectors (clearing houses, in particular).

In this context, several international initiatives have emerged and interest from the financial sector is now growing.

2.1 The work of the Task Force on Climate-related Financial Disclosure

At the international level, the G20 Financial Stability Board (see BSI Economics article: » The institutional architecture of international financial regulation » ) set up a working group at the end of 2015, the Task Force on Climate-related Financial Disclosure (TCFD), composed of private sector actors and chaired by Michael Bloomberg. Tasked with developing principles applicable to all sectors for the disclosure of climate-related financial information, it published its final report in June 2017. Its recommendations enable companies to identify the relevant information to include in their climate reporting and thus define a climate risk management strategy. These recommendations are divided into four guidelines:

- Governance (oversight by the board of directors of climate-related risks and opportunities; role of management);

- Strategy (how the company measures the impact of climate change risks and opportunities on its strategy and financial plan in the short, medium, and long term);

- Risk management;

- The indicators, metrics, and targets that the company uses in this context.

The TCFD therefore recommends conducting forward-looking analyses (of both risks and opportunities for companies’ financial performance) based on scenario analysis (including a +2°C scenario). Furthermore, this analysis must ultimately be quantitative and provide a comprehensive presentation of the assumptions used in all of the scenarios.

The TCFD’s work is particularly important in that it encourages the necessary harmonization of current climate-related disclosure frameworks and pushes financial and non-financial institutions to implement robust methodologies and data collection practices. At the One Planet Summit in December 2017, 237 companies (representing $6.3 trillion in capital, including 20 of the 30 largest banking groups) committed to integrating the TCFD’s recommendations (which will continue its work until 2019 to guide stakeholders in implementing the recommendations).

2.2 The European Commission’s action plan for sustainable finance: one of the priorities of the Capital Markets Union

Following the work of the High-Level Expert Group on Sustainable Finance, whose final report was published in February 2018, the European Commission published its action plan on March 8, 2018.

This action plan aims to achieve three objectives:

a) Redirecting capital flows towards a more sustainable economy

As a prerequisite, establish a common classification of green assets and sustainable activities

The Commission first plans to establish a taxonomy, i.e., a unified European-wide framework for sustainable assets and activities, in line with the Sustainable Development Goals and the provisions of the Paris Agreement. This classification will aim to facilitate investment decisions in favor of « green » initiatives, channel capital flows towards activities that contribute to sustainable development, and enable the development of sustainable indices, European standards and labels, and green prudential regulation (see below).

Broken down by sector, the taxonomy will include thresholds, metrics, and selection criteria, as well as eight different levels (from investments directly aimed at mitigating climate change to those with broader objectives, such as pollution prevention). The backbone of the Action Plan, the taxonomy is nonetheless the most difficult exercise (definition of the « sustainable » nature of an activity; rapid technological change; degree of granularity).

Creating European standards and labels for sustainable financial products

Given the diversity of existing labels, the Commission considers it necessary to create European standards and labels, starting this year with the development of a European green bond standard (EU Green Bond Standard), which will clarify and strengthen the impact of the green bond market and increase the volume of issuances. The European Commission also wishes to explore the use of the European eco-labeling framework for financial products intended for individuals, once the taxonomy has been adopted.

b) Integrating sustainability into the risk management of financial institutions

Financial institutions need to integrate climate and environmental risks into their day-to-day risk management and investment strategies. The Commission is considering three actions in this regard:

- Require rating agencies to explicitly integrate the sustainability of investments into their market research and credit ratings of financial institutions;

- Clarify the « duties » of investors, insurance companies, pension funds, and asset managers in terms of investment strategy, asset allocation, risk management, and governance;

- Require asset managers to provide clear information to end clients on how sustainability factors are integrated into investment decision-making processes and the assessment of material risks.

- Integrate sustainability into the prudential requirements for banks and insurance companies by incorporating climate risks into risk management policies and calibrating the capital requirements applicable to banks (introduction of a potential » green supporting factor » consistent with the taxonomy and justified from a risk perspective). This proposal is far from unanimous, particularly among prudential regulators (see Bruegel article, » Climate change adds to risk for banks, but EU lending proposals will do more harm than good , » January 2018).

c) Promoting transparency and long-term thinking within financial institutions

To this end, the Commission plans to revise existing legislation on non-financial reporting in line with the TCFD recommendations. It also wants to promote corporate governance that disseminates all the standards and values necessary for the development of a more sustainable financial system (i.e., the role of the board of directors and senior management of financial institutions). The European Commission’s proposal also includes extending the mandate of European supervisory authorities to monitor environmental and social risks, including in particular the monitoring of « mismatched time horizons » and « short-termism » within the financial sector.

The European Commission’s Action Plan thus remains an ambitious roadmap with a tight schedule (2018-2019) that gives climate change a prominent place within the broader set of « ESG » (environmental, social, and governance) risks.

However, the financial sector’s commitment and the redirection of long-term savings towards the low-carbon transition must also ensure, in line with the recommendations of the Lemmet-Ducret report of December 2017:

- increased investment by individuals in the low-carbon transition (extending the transparency of investors and asset managers to products intended for individuals; providing individuals with more information on the climate impact of their life insurance, Livret A savings accounts, and sustainable development savings accounts; strengthening financial education in line with sustainable finance objectives); and

- exponential strengthening of public investment in the ecological transition (reorientation of the European budget and consistency of French public investments (operators; state budget programs; companies in which the state is a shareholder) with a 2°C trajectory, etc.).

In addition, both in international and European work, vigilance will be required regarding how « unsustainable » activities are treated, particularly in taxonomy, index methodology, and the » Sustainable Infrastructure Europe » plan plan (i.e., under the terms of the Action Plan of the European Commission, the body responsible for supporting public authorities in setting up and financing green projects).

Conclusion

Climate change is now recognized as a systemic risk for the financial sector. Ten years after the 2008 financial crisis, it is also important to recognize the financial sector’s essential role in financing a low-carbon economy. That is why, in December 2017, several prudential supervisors created the Network of Supervisors and Central Banks for the Greening of the Financial System. The French Financial Markets Authority (AMF) has also made the promotion of sustainable finance and the investment of long-term household savings one of the priorities of its five-year strategic plan. In any case, the political momentum generated by the diplomatic success of the Paris Agreement in 2015 and the One Planet Summit in 2017 must now be followed by the concrete implementation of regulatory incentives, the development of innovative financial tools, and increased investment in the energy transition—despite obvious diplomatic and technical difficulties. This also remains a crucial interest for the financial industry. The coming months will be decisive in this regard.

Bibliography

Aglietta, M., & Rigot, S. (2012). Long-term investors, financial regulation, and sustainable growth. Revue d’économie financière, (4), 189-200

Aglietta, M., Espagne E., and B. Perrissin-Fabert. « A proposal to finance low carbon investment in Europe. » France Stratégie: Paris ( 2015).

Aglietta M.; Espagne E., “Climate and Finance Systemic Risks: more than an analogy? The climate fragility hypothesis”, Working Paper CEPII, April 2016.

Andersson, M., Bolton, P., & Samama, F. (2014). Hedging climate risk. Columbia Business School Research Paper, (14-44).

Autorité des marchés financiers, Press release, “On Climate Finance Day, the AMF affirms its commitment to sustainable finance,” December 11, 2017. Available online.

Boot A., Schoenmaker D., Climate change adds to risk for banks, but EU lending proposals will do more harm than good, Bruegel, January 16, 2018.

Campiglio, E. (2016). Beyond carbon pricing: The role of banking and monetary policy in financing the transition to a low-carbon economy. Ecological Economics, 121, 220-230.

Carney Mark, “A Transition in Thinking and Action,” International Climate Risk Conference for Supervisors, De Nederlandsche Bank, April 6, 2018. Available online.

Direction générale du Trésor & Autorité de contrôle prudentiel et de résolution, “L’évaluation des risques liés au changement climatique dans le secteur bancaire,” February 2017.

Etienne Espagne, 2016. « Climate Finance at COP21 and After: Lessons Learnt, » CEPII Policy Brief 2016- 09, 2016 , CEPII

European Commission (2018), EU Action Plan for Sustainable Finance.

European Systemic Risk Board (2016). Too late, too sudden: transition to a low carbon economy and systemic risk. Report of the advisory scientific committee. No. 6.

Financial Stability Board, Final Report: Recommendations of the Task Force on Climate-related Financial Disclosures (June 2017)

Hourcade, J. C., Fabert, B. P., & Rozenberg, J. (2012). Venturing into uncharted financial waters: an essay on climate-friendly finance. International Environmental Agreements:Politics, Law and Economics, 12(2), 165-186.

Lemmet S., Ducret P., “Pour une stratégie française de la finance verte” (Towards a French green finance strategy), Report submitted to Nicolas Hulot and Bruno Le Maire, December 2017.

London School of Economics, Gratham Research Institute on Climate Change and the Environment,“Green doesn’t mean risk-free: why we should be cautious about a green supporting factor in the EU,” December 18, 2017.

Schoenmaker Dirk, Van Tilburg Rens,“Financial risks and opportunities in the time of climate change,” Bruegel Policy Brief, April 2016.

Schoenmaker Dirk, Van Tilburg Rens,“What role for financial supervisors in addressing environmental risks?”, January 2016.

Villeroy De Galhau F. (2015). Climate change: the financial sector facing 2°C trajectories – Speech, CEPII-France Stratégie Climate Finance Platform.

Weitzman, M. L. (2009). On modeling and interpreting the economics of catastrophic climate change. The Review of Economics and Statistics, 91(1), 1-19.

[1]Intergovernmental Panel on Climate Change, created in 1988 by the World Meteorological Organization and the UN.

[2]Recall the success of the Montreal Protocols in 1987, the Rio Conference in 1992, and the publication of the Stern Reviewon Economics of Climate Change byeconomist Nicholas Stern in 2006.

[3]A sharp deterioration in financial stability characterized by contagion and the spread of shocks due to the impacts of climate change.

[4]Garrett Hardin, in » Tragedy of the Commons » (1968), highlighted the collective phenomenon of overexploitation of common resources when they are considered public goods (characterized as non-rival and non-exclusive).

[5]« Financial policymakers will not drive the transition to a low-carbon economy. Our efforts cannot substitute for those of governments who have direct responsibilities to deliver the policies to achieve their Paris commitments. The good news is that governments are now establishing the policy frameworks, and the private sector is beginning to allocate capital accordingly. Our efforts will help smooth the transition prompted by these actions. With better information and risk management as the foundations, a virtuous circle is being built with better understanding of tomorrow’s risks, better pricing for investors, better decisions by policymakers and a smooth transition to a low carbon economy, » Mark Carney, at the International Conference of Supervisors on Climate Risk (April 6, 2018).

[6] This graph highlights the risk scenarios that financial institutions will face depending on the trajectory of greenhouse gas emissions over the period 2014-2100. If measures to combat global warming are implemented in a +2°C scenario (i.e., limits on future CO2 emissions), then we will see a sharp decline in the current trajectory and the emergence of mainly transition risks. However, the adverse scenario consists of a « hard landing » due to the late adjustment of economic policy through the introduction of constraints on carbon-intensive energy use. If current emissions are not drastically reduced, then the +2°C limit will be reached by 2040 and financial institutions will face mainly physical risks.

[7]The UNEP Finance Initiative was founded as a partnership between the United Nations Environment Programme and 200 financial institutions worldwide to encourage the financial system to effectively mobilize capital towards a green and inclusive economy.