Abstract :

- Socially responsible investment (SRI) is growing in parallel with the concept of corporate social responsibility (CSR) thanks to the increasing importance of sustainable development.

- « SRI aims to reconcile economic performance with social and environmental impact by financing entities that contribute to sustainable development. By influencing governance, SRI promotes a responsible economy. »

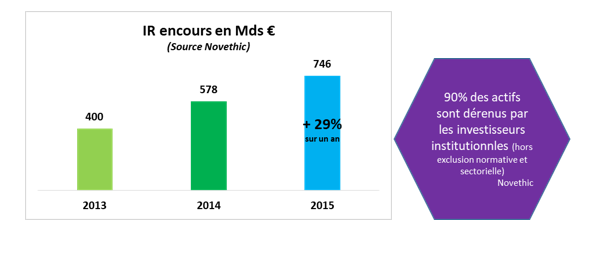

- At the end of 2015, the total assets under management in the responsible investment market in France amounted to €746 billion.

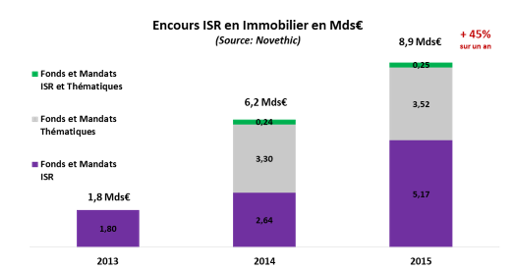

- Real estate is a sector that is heavily involved in sustainable development issues. The assets under management declared as SRI and/or thematic in the Novethic study reached €8.9 billion, an increase of +45% over one year (between 2014 and 2015), which is rather encouraging and demonstrates the growing interest of real estate managers and investors in integrating ESG criteria into their responsible investment strategy.

.jpg)

Awareness of environmental, social, and governance issues, changing consumption habits among current generations, regulatory incentives, technological disruption… there are many reasons why institutional investors, managers, and individuals are increasingly interested in integrating ESG practices into their investment strategies. Between financial performance and a genuine desire to contribute to addressing environmental and other issues, socially responsible investment is on the rise in France.

After introducing the concept of sustainable development, its application to businesses (CSR), and its transposition to the financial sector for responsible investment (SRI), this article explains the different approaches used by investors and management companies to analyze their issuers, followed by a brief summary of existing labels and regulatory incentives for more « sustainable » finance. Finally, it focuses on SRI in real estate investment.

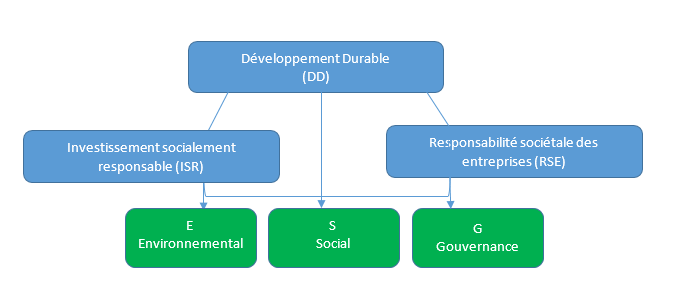

I.Sustainable Development, ESG, CSR, and SRI: Brief Background and Concepts

Socially responsible investment (SRI) is growing in parallel with the concept of corporate social responsibility (CSR) thanks to the increasing importance of the concept of sustainable development.

The official definition of sustainable development was established in 1987 in the Brundtland Report published by the World Commission on Environment and Development: » Sustainable development is development that meets the needs of the present without compromising the ability of future generations to meet their own needs. » Two concepts are inherent in this notion: the concept of « needs, » and more particularly the essential needs of the most disadvantaged, to whom the highest priority should be given, and the idea of the limitations that the state of our technology and social organization impose on the environment’s capacity to meet current and future needs. »[1]

Sustainable development must be economically efficient, socially equitable, and ecologically tolerable. Its objective is to define models that reconcile three pillars taken into account simultaneously by communities, businesses, and individuals: the environment, society, and the economy, and to find a long-term viable balance between these three issues. The interdependence between these three pillars is the central theme chosen by the Bruntland Commission.

In addition to these three issues, there is a fourth that plays a cross-cutting role: governance, which involves the participation of all stakeholders—elected officials, businesses, and citizens—and is essential to the definition and implementation of sustainable development policies.

This macroeconomic concept of sustainable development is a constantly evolving process in which the exploitation of natural resources, investment choices, and institutional and social changes are aligned and consistent with both the future and current needs.

The transposition of sustainable development objectives for businesses is Corporate Social Responsibility (CSR), a microeconomic concept that involves the voluntary contribution of businesses to sustainable development. The definition given by the Ministry of Ecological and Solidarity Transition is as follows: « CSR is a concept in which companies integrate social, environmental, and economic concerns into their activities and interactions with their stakeholders on a voluntary basis. »

Socially Responsible Investment (SRI), on the other hand, involves applying sustainable development practices to the financial sphere. It is a method of managing financial investments that takes into account non-financial criteria in addition to financial criteria. SRI systematically integrates ESG pillars into management methods.

There is a link between CSR and SRI: the more investors are encouraged to integrate non-financial criteria (Environmental, Social, and Governance – ESG) into their investment selection, the more companies will be encouraged to adopt and improve their CSR policies.

All these concepts are based on three pillars: E S G

ESG istherefore a universal acronym used by the financial community to refer to the pillars of sustainable development as applied to the sector. They constitute the criteria for SRI’s extra-financial analysis. They are used to assess companies’ responsibility towards the environment and their stakeholders.

E – Environment: covers issues related to the impact of human activities on nature and the resulting environmental risks, such as climate change, pollution, waste management, deforestation, etc.

S – Social: refers more to the organization of human relations, including accident prevention, staff training, human rights, social relations, labor law, and social dialogue, among others.

G – Governance: an essential criterion that ensures alignment of interests between investors and company managers. It verifies issues such as the independence of the board of directors, internal control procedures, compliance with ethical rules and the law, etc.

II.The responsible investment (RI) market in France: definition, types of management

A. Some figures on the French RI market[2]

According to Novethic, the Responsible Investment (RI) market in France was worth €746 billion at the end of 2015, up 29% on 2014. This includes all management that incorporates Environmental, Social, and Governance (ESG) criteria, excluding exclusions alone. This market is largely dominated by institutional investors, who hold 90% of it.

B. SRI: what is it?

Several definitions have been given to SRI, some more official than others, using different terminology. In this article, we will use the definition of SRI developed by the French Financial Management Association (AFG) and the Forum for Responsible Investment (FIR). This definition is more precise and clearly highlights the links mentioned above between CSR and SRI based on the three pillars of sustainable development.

« Socially responsible investment (SRI) is an investment that aims to reconcile economic performance with social and environmental impact by financing companies and public entities that contribute to sustainable development, regardless of their sector of activity. By influencing the governance and behavior of stakeholders, SRI promotes a responsible economy. »

SRI not only involves the systematic integration of ESG criteria analysis into management and investment processes, but also represents a medium/long-term strategy that complements traditional financial analysis, enabling investors to play a more proactive role in the economy without sacrificing financial performance, as the objective remains to improve the risk/return ratio of investments by promoting a responsible economy in the long term.

According to the report by the French Financial Markets Authority (AMF) on socially responsible investment[3], SRI generally meets three main objectives:

- Investing according to a certain philosophy and in accordance with certain values;

- Investing while taking into account the risks and opportunities identified in the extra-financial analysis of issuers;

- Investing with the aim of having a positive impact on social, environmental, and governance issues.

More and more institutional investors, management companies, and individuals are attracted to SRI for a variety of reasons, including brand image and reputation, asset performance, and more.

Nevertheless, both institutional and individual investors see SRI as an opportunity to have a positive impact on society by exercising their social responsibility, reducing risks, and increasing the quality of their assets. It is possible to reconcile economic performance with social and environmental criteria and invest in companies that contribute to sustainable development.

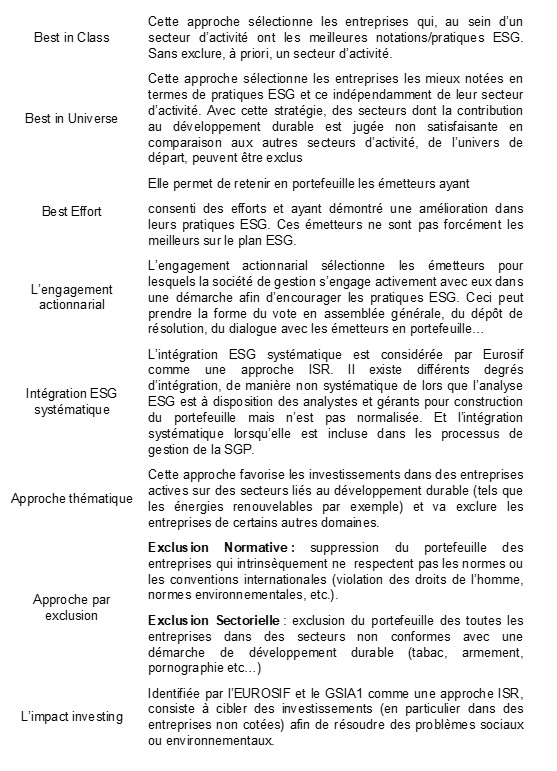

C. What are the different approaches or types of SRI management?

Approaches, types of management, strategies… different terms that express the same intention, that of schematically classifying SRI funds. The issuers represented in an SRI fund are all selected on the basis of their compliance with ESG practices, which is already a positive strategy in itself. These issuers are also selected according to the approach adopted by the management company.

The following table presents a non-exhaustive list of the main categories of SRI approaches, most of which are taken from the AMF report of January 2015[4] and other sources cited in the bibliography.

III.Development of socially responsible investment: regulatory initiatives

At the international level, socially responsible investment began to take shape in 2006 thanks to the six Principles for Responsible Investment (PRI) published by the United Nations. These principles encourage investors to integrate ESG issues into their portfolio management and to report on their practices[5].

Aimed at the financial sector in general, the principles are based on voluntary commitment and encourage investors to integrate, in the broadest sense, Environmental, Social, and Governance (ESG) issues into their portfolio management.

This applies to asset owners, investment portfolio managers, and professional services partners.

The six principles are as follows[6]:

- Consider ESG issues in investment analysis and decision-making processes;

- Be active investors and take ESG issues into account in shareholder policies and practices;

- Require the entities in which they invest to disclose appropriate information on ESG issues;

- Promote acceptance and implementation of the Principles among asset management stakeholders;

- Work together with financial sector stakeholders to increase the effectiveness of the application of the Principles;

- Report individually on their activities and progress in applying the Principles.

A.Labels

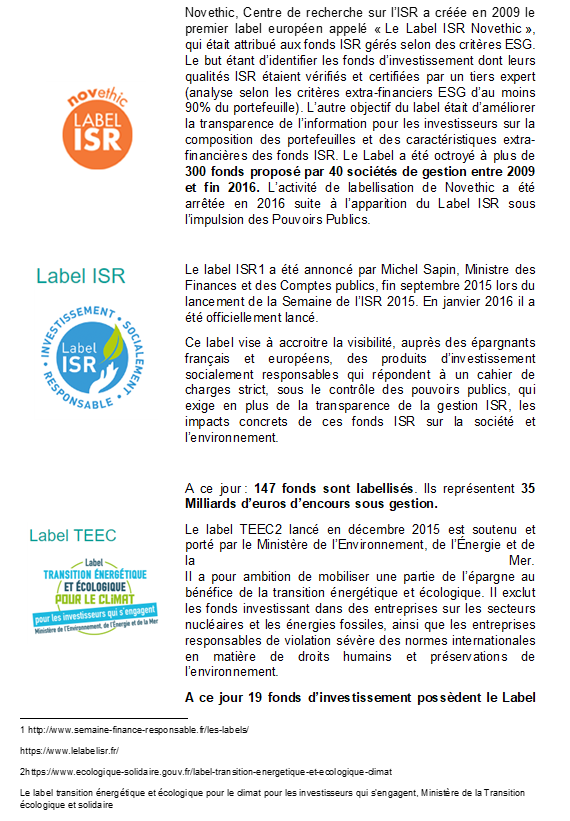

In France, the Novethic Label was introduced in 2009 to promote funds whose ESG qualities and practices have been verified. Then, at the end of 2015, two state-supported labels were introduced: the public SRI label and the Energy and Ecological Transition for the Climate (TEEC) label for funds financing the green economy. Since 1997, the Finansol Label has supported the financing of activities that are socially and environmentally beneficial. Below is a non-exhaustive list of labels:

B. Articles 224 and 225 of the Grenelle II law

Articles 224 of the Grenelle II Act (July 12, 2010)

Introduces for the first time the obligation for open-ended investment companies and management companies to mention in their annual reports and in their documents intended to inform their subscribers the methods used to take into account criteria relating to compliance with social, environmental, and governance objectives in their investment policy.

Management companies specify the nature of these criteria and how they apply them in accordance with a standard format established by decree on January 30, 2012.

Article 225 of the Grenelle II Law

Since 2001, with the application of the New Economic Regulations Act (NRE), listed companies have been required to include information in their management reports on the « social and environmental consequences of their activities and their societal commitments to sustainable development. »

Article 225 of the Grenelle 2 Act (July 12, 2010) and its implementing decree of April 24, 2012 extend the obligations to unlisted French companies with an average number of employees exceeding 500 and a balance sheet total or net turnover exceeding €100 million.

In 2017, the system was modified and strengthened by the transposition of the European Directive on the disclosure of non-financial information. Now a European system, it requires companies to report on their non-financial performance, while also focusing on more material issues.

C. Article 173 of the Energy Transition for Green Growth Act (TECV), the impetus for responsible finance

Article 173 (paragraph VI) of the Law on Energy Transition for Green Growth (TECV), of August 17, 2015, requires portfolio management companies and institutional investors to provide their subscribers with information on how environmental, social, and governance (ESG) criteria are taken into account in their investment policy, as well as the means put in place to participate in the energy and ecological transition[9]. This transparency requirement is an extension of Article 224 of the Grenelle II law, which is more demanding on the environmental pillar, specifically on the issue of climate change. Neither the text of the law nor its decree provide guidelines or a methodology to be followed for this reporting, thus giving investors freedom of interpretation and action, depending on their sector and activities. The aim is to understand how investors integrate ESG criteria into their investment strategies, but also to identify and disseminate best practices in order to steer investments towards more responsible and environmentally friendly assets.

The decree provides for two types of information: information relating to the investor’s ESG policy and information relating to the investor’s consideration of ESG criteria in their investment strategy.

France is asserting its leadership position by becoming the first country in the world to require investors to disclose information on their climate objectives and their contribution to combating climate change and preserving the environment.

IV.Responsible Investment in Real Estate

A. Real estate IR market figures in France

Thanks to a real awareness among investors and also encouraged by new regulatory obligations, ESG issues are rapidly spreading in real estate management.

According to a study by Novethic[11] and ASPIM on the responsible real estate investment market, there is a strong trend towards taking environmental and social issues into account. More than half of the management companies in the panel[12] have quantified improvement targets for environmental criteria, particularly energy.

Ninety percent of survey participants report that they incorporate building energy performance analysis into their management practices.

The assets under management declared as SRI and/or thematic in the study grew very strongly, with +45% growth between 2014 and 2015 to reach €8.9 billion. This is due not only to the collection of existing funds but also to the creation of new funds, confirming the momentum of the SRI trend.

Funds and real estate mandates declared as exclusively SRI represent 58% of total assets under management, almost doubling between 2014 and 2015 to reach €5.17 billion. Thematic real estate funds and mandates also recorded an increase in assets under management (+7% year-on-year) to €3.5 billion, while assets under management in the last category of SRI and thematic funds and mandates remained stable despite a slight increase (+4%) year-on-year to €0.25 billion.

With a focus on ESG criteria and driven by regulations, in particular Article 173 of the TECV law, it is hoped that investments in SRI funds will continue to grow in the coming years.

B. Real estate and SRI practices

Real estate is a sector that is heavily involved in sustainable development issues. Several regulatory incentives relating to the environment have pushed and forced the sector to transform itself and contribute to the energy and ecological transition.

It is estimated that the real estate and construction sectors account for 44% of energy consumption in France. Buildings are responsible for 25% of greenhouse gas emissions[13].

Areas for improvement focus mainly on taking environmental criteria into account in the real estate investment sector, although social criteria are increasingly being integrated (mobility, access, comfort of residents)[14].

The difficulty of integrating criteria that promote sustainable development into the real estate investment sector lies in the indirect nature of the relationship between investors and the sector’s ESG performance[15].

Investors invest through external fund managers, who themselves use independent property managers to manage real estate and manage tenant relations. In this part of the chain, it is sometimes necessary to also use service providers to provide security, cleaning and maintenance, waste management, and energy services, among others.

However, tenants are independent companies which, once the lease has been signed, are free to use the real estate as they wish. Furthermore, there is a relationship of rivalry and power between tenants and landlords that has a detrimental impact on the eco-efficiency of real estate. Without a contract that provides for shared savings between tenants and landlords, there is no real incentive for eco-efficient behavior.

Finally, the nature of real estate investment vehicles does not allow a single investor to be the sole or principal owner of a property or real estate portfolio, which reduces their influence on management strategy.

However, it is important to note that institutional investors dominate the SRI market in real estate, and they are uniquely positioned to overcome the difficulties mentioned above, as they benefit from direct relationships with real estate fund managers, property managers, tenants, and various service providers. This privileged position gives them significant influence over the promotion of and compliance with ESG practices.

Investors also have an impact on the underlying assets, i.e., the buildings. They can influence environmental performance through their choice of new construction and renovations, and through their direct relationships with various stakeholders, they can improve the environmental performance of existing buildings. Social criteria in real estate can be measured by their influence on the structure of a city, the dynamism of a neighborhood, urbanization, and also compliance with labor laws and employee protection.

In real estate, whether by applying an ESG rating to asset acquisitions, selecting assets on the basis of social utility, or implementing sector exclusions, ESG approaches are quite varied and depend on the type of asset and ownership structure[17]:

- Direct investment:investors’ ESG approaches are based on environmental and social ratings of buildings, which are used to improve the existing stock. ESG practices are implemented through work on buildings and technical installations and through dialogue with service providers, integrating non-financial clauses into management and maintenance contracts, and with tenants to inform them and involve them in the ESG approach.

- Indirect investment in unlisted funds: investors’ ESG approach is based on analyzing the non-financial performance of portfolios, setting quantified improvement targets, and effectively reducing environmental and social risks through impact analysis, including the assessment of managers’ social and governance policies.

- Indirect investment in companies in the sector through the holding of shares and bonds: investors begin by selecting the real estate companies with the best ESG performance ratings, referring to specialized platforms such as GRESB (Global Real Estate Sustainability Benchmark). They can also monitor the performance of the buildings managed in order to engage in dialogue with managers with a view to improving ESG practices.

The transparency requirement established by Article 173 of the TECV law does not apply to OPCIs and SCPIs. However, in order to assess the ESG risks and opportunities of their investment strategies, investors must collect relevant information from the asset management companies or issuers with which they work. By extension, managers of real estate funds and listed real estate companies will have to contribute and be required to provide information on their ESG and climate practices. This need for information will have a rather positive impact on real estate sector management and ESG practices.

C. Some data on the integration of environmental and social criteria by real estate managers (Source: Novethic, data as of end-2015)[18]

In concrete terms, the majority of real estate management companies have already integrated the analysis of asset energy performance as a management standard. Ninety percent of respondents to the survey conducted by Novethic and ASPIM reported having formalized a responsible investment policy, particularly with regard to energy, water, and waste.

For the real estate sector, two types of non-financial criteria analysis have been identified: at the time of acquisition and during management and operation.

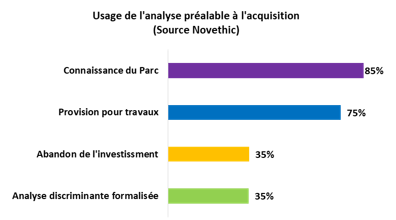

In addition to regulatory requirements, 55% of respondents combine an analysis of social and environmental criteria for some of their acquisitions, with 25% of the sample conducting a systematic ESG analysis.

In 85% of cases, pre-acquisition analyses focus primarily on understanding the building stock and potential, 75% on assessing the provisions to be allocated to future works, and 35% on abandoning the investment.

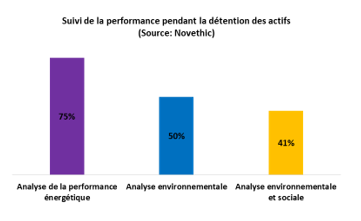

During the holding period (analysis during management and operation), 75% of real estate managers assess the energy performance of the real estate portfolio. This analysis, based on the study of bills or meters, etc., makes it possible to monitor eco-efficiency and identify areas for improvement. 41% of the real estate funds surveyed combine monitoring that takes both social and environmental criteria into account.

An increase in the ability to quantify improvement objectives was noted between 2014 and 2015, with 55% of investors surveyed in 2015 quantifying these objectives, compared to 25% in 2014. Energy performance is one of the improvement targets that more than doubled between 2014 and 2015, followed by waste and water management, social issues, and finally certification.

Playing a key role in the ESG approach, real estate managers act as traditional managers but also as interlocutors for stakeholders and analysts of the underlying assets. They therefore have the power to directly influence the implementation of ESG initiatives in their working environment, particularly with a view to improving the performance of their portfolio.

Sixty percent of the sample reported having incorporated ESG clauses into contracts with property managers, who were selected based on their ESG practices (for 25% of respondents). They are committed to providing tenants with environmental charters and best practice guides to raise awareness of sustainable development initiatives.

The various data are rather encouraging and demonstrate the growing interest of real estate managers and investors in integrating ESG criteria into their responsible investment strategy. Nevertheless, as is the case in other investment sectors, the lack of standardization of practices makes it difficult for investors to interpret ESG initiatives. Standardizing practices would make it easier for all stakeholders to understand the various environmental, social, and governance initiatives undertaken by real estate players and would enhance the effectiveness of the actions implemented to contribute to the energy transition.

Conclusion

Sustainable finance is a major issue that the European Commission has made one of its priorities. It is essential to adapt public policies towards a greener and more sustainable economy. To this end, on March 8, 2018, it published an action plan aimed at designing a new financial framework for Europe to promote transparency, integrate sustainability into risk management, and redirect capital flows towards a sustainable economy and sustainable investments. These actions are in line with the climate objective of the Paris Agreement and also with the Capital Markets Union initiative.

According to the report[19], two conditions must be met for sustainable finance:

- Improve the financial system’s contribution to sustainable and inclusive growth by financing society’s long-term needs;

- Strengthen financial stability by integrating environmental, social, and governance (ESG) factors into investment decision-making.

In France, similar and complementary initiatives are also emerging. In particular, the Banque de France is increasingly integrating SRI into its scope and, in March 2018, published a Responsible Investment Charter[20] that affirms France’s exemplary role in the development of a balanced and sustainable economy.

Responsible finance is thus widely supported at both the French and European levels, ensuring its future dynamism.

Bibliography

- « ESG-Climate Approaches of Real Estate Managers » Guide on taking into account the requirements of Article 173-VI of the Energy Transition Law in real estate, OID and PWC; December 2017

- The different forms of SRI, NOVETHIC https://www.novethic.fr/isr-et-rse/comprendre-lisr/les-differentes-formes-de-lisr.html

- AMF report on socially responsible investment (SRI) in collective management, November 2015

- The essentials of SRI real estate, Novethic – September 2015

- Responsible Investment in Real Estate, French market figures for 2016, Novethic-ASPIM study

- Building a responsible real estate portfolio. Review of current practices of signatories to the UNEP Finance Initiative and PRI; UNEP Finance Initiative and PRI

- Responsible investment: multiple and complementary approaches. AGEFI in partnership with Amundi Asset Management

- How are SRI funds structured? LCL Banque et Assurances https://www.lcl.com/guides-pratiques/isr-epargne-solidaire/investissement-socialement-responsable/approches-isr.jsp

- 2015 figures for responsible investment in France, Novethic

- What does ESG mean? The acronym has become the standard for defining what sustainable investment is. http://www.morningstar.fr/fr/news/148936/que-signifie-esg-.aspx

- The asset management industry is shifting towards SRI, Option Finance, Special Edition No. 56 – April 30, 2018

- Guide – Energy Transition for Green Growth Act. Application of Article 173 to management companies (Implementing Decree No. 2015-1850 of December 29, 2015), AFG – October 2016

- http://www.semaine-finance-responsable.fr/les-labels/

- https://www.lelabelisr.fr/

- https://www.ecologique-solidaire.gouv.fr/label-transition-energetique-et-ecologique-climat

- https://www.ecologique-solidaire.gouv.fr/loi-transition-energetique-croissance-verte

- The energy and ecological transition label for climate action for committed investors, Ministry for Ecological and Solidarity Transition.

- http://www.finansol.org/pourquoi-un-label/

- GRESB SNAPSHOT France 2017

- Communication from the Commission to the European Parliament, the European Council, the Council, the European Central Bank, the European Economic and Social Committee, and the Committee of the Regions – Action Plan Financing Sustainable Growth; Brussels, March 8, 2018

- The European Commission unveils part of its action plan to boost green finance, Novethic, March 2018

- Thanks to Audrey Hyvernat, SRI Director at AFG, for her help with this topic.

[2]2015 figures for Responsible Investment in France, Novethic

[5]« ESG-Climate Approaches by Real Estate Managers » Guide on taking into account the requirements of Article 173-VI of the Energy Transition Law in real estate, OID and PWC; December 2017

[8]“ESG-Climate Approaches for Real Estate Managers” Guide on taking into account the requirements of Article 173-VI of the Energy Transition Law in real estate, OID and PWC; December 2017

[9]Source: Ministry of Ecological and Solidarity Transition 2015, www.ecologique-solidaire.gouv.fr/loi-transition-energetique-croissance-verte

[10]Exposure to climate risk, measurement of greenhouse gas emissions from assets held, compliance with the objective of reducing global warming, and contribution to an energy and ecological transition. Source: « ESG-Climate Approaches of Real Estate Managers » Guide on taking into account the requirements of Article 173-VI of the Energy Transition Law in real estate,OID and PWC; December 2017

[11]Responsible Investment in Real Estate, French market figures for 2016; Novethic.

[12]20 of the leading real estate fund management companies operating on the French market, managing €90 billion in assets as of December 31, 2015, Novethic.

[13]: « ESG-Climate Approaches of Real Estate Managers » Guide on taking into account the requirements of Article 173-VI of the Energy Transition Law in real estate,OID and PWC; December 2017

[15]Building a Responsible Real Estate Portfolio. Review of Current Practices of Signatories to the UNEP Finance Initiative and PRI; UNEP Finance Initiative and PRI

[16]Real Estate Investment Trusts (OPCI), Real Estate Investment Companies (SCPI), etc.

[17]The essentials of SRI real estate, Novethic – September 2015

[18] Responsible Investment in Real Estate, French market figures for 2016, Novethic-ASPIM study

[19]Communication from the Commission to the European Parliament, the European Council, the Council, the European Central Bank, the European Economic and Social Committee, and the Committee of the Regions – Action Plan on Financing Sustainable Growth; Brussels, March 8, 2018