· In France, the pension system is based on the pay-as-you-go principle, which promotes intergenerational solidarity. Contributions paid by workers and their employers are redistributed to retirees in the form of retirement pensions.

· Mandatory retirement has two main components: the basic pension (mandatory general scheme – CNAV/MSA) and the supplementary pension (Arrco, Agirc);

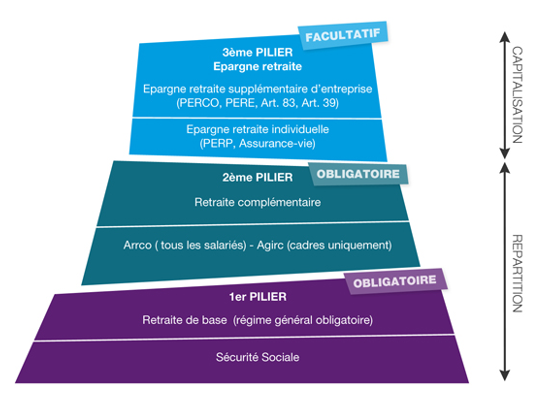

· Retirement in France has three pillars: the basic pension and the supplementary pension are the first two mandatory pillars based on distribution, and retirement savings are the third optional pillar based on capitalization.

The French pension system, established in 1945, is based on the principle of distribution, which promotes intergenerational solidarity. It is characterized by a multiplicity of schemes governed by specific regulations and managed by public bodies, a total of 35 pension organizations, to which all working people are affiliated.

Over the years, the French pension system has undergone a number of reforms aimed at consolidating it, and one of these reforms introduced a degree of capitalization via supplementary pensions. Today, retirement in France consists of three pillars: the mandatory pay-as-you-go pension, which is made up of two elements: the basic pension (general scheme), which comprises thefirst pillar, and the supplementary pension, which is managed by different organizations depending on the employee’s status and comprises the second pillar of the pension system. The third pillar, which is optional, consists of supplementary capitalization pensions via regulated savings products (individual and collective) dedicated to retirement, known as retirement savings.

The pension system in France

The French pension system is based on the principle of distribution[1], which promotes solidarity between generations: contributions paid by workers and their employers are redistributed to retirees in the form of retirement pensions.

The pay-as-you-go pension system in France is also characterized by the presence of a multiplicity of schemes: some are intended for private sector employees, others for civil servants, liberal professions, or farmers. So-called « special » schemes[2] complete the system.

The schemes are governed by specific regulations. They are managed by public bodies, a total of 35 pension organizations, to which all working people are affiliated.

In France, the compulsory pay-as-you-go pension system has two main components: the basic pension and the supplementary pension:

1. The basic pension is the mandatory general scheme (CNAV/MSA) created in 1945. At the time, it was planned that all other schemes would also be affiliated to it, but some schemes retained their autonomy (special schemes, self-employed and civil servants), as these professions decided to keep their pre-war pension schemes, which were more favorable than the general scheme. Nevertheless, since the numerous reforms, all these schemes have tended to converge but remain distinct.

2. Supplementary schemes were introduced in 1947 to cover the shortfall in pensions from the general scheme for certain professional categories (particularly executives), which became the AGIRC. Non-executives had to wait until 1957 for the introduction of their ARRCO supplementary scheme, and non-civil service employees had to wait until 1971 for the introduction of IRCANTEC[1]. The two supplementary pension components for employees under the general scheme became compulsory in 1972.

The French pension system worked well during the 30 glorious years, but since the 1980s it has shown weaknesses due to structural demographic factors such as the decline in the birth rate and, in particular, the increase in life expectancy.

In the medium to long term, the viability of the pay-as-you-go pension system depends essentially on maintaining the balance between the number of active workers and retirees. However, for cyclical reasons, but above all for structural reasons such as the baby boom, increased life expectancy, and the aging of the population (according to INED, by 2030, people over the age of 60 will represent 30% of the population), it is not certain that this balance can be maintained.

Furthermore, the decline in replacement rates[3] makes it necessary to build up supplementary retirement savings. The replacement rate varies according to pension schemes, individual careers, and income levels in particular; the higher the income, the lower the replacement rate. This system was designed so that people with the lowest incomes lose less than those with higher incomes when they retire. According to the DRESS[4], half of private sector employees who have worked for their entire career (40 years of continuous employment) receive a pension corresponding to less than 73.8% of their net salary at the end of their career.

Over the years, reforms have been introduced to consolidate the system and try to overcome the difficulties of the pay-as-you-go system and the lack of future income. Thus, a degree of capitalization has been introduced via regulated savings products dedicated to retirement, as part of supplementary retirement plans with individual or collective products, known as retirement savings.

The three pillars of retirement in France (focus on the private sector)

First pillar – the basic pension, i.e., the mandatory general scheme:

The general Social Security scheme (CNAV – Caisse nationale de l’assurance vieillesse des travailleurs salariés) and the agricultural workers’ scheme (MSA – Mutualité sociale agricole) are pay-as-you-go schemes intended for all workers in the public and private sectors, as well as the self-employed. These schemes are universal and compulsory, and each applies to only a fraction of the population: employees in the private sector, industry, commerce, and services; non-tenured civil servants and local government employees; civil aviation flight crew; liberal professionals; artisans; merchants; and authors of original works.

The amount of the basic retirement pension is calculated on an annual basis[1] and according to several parameters: income, duration, and amounts of contributions paid throughout the working life.

Second pillar – mandatory supplementary pension:

These supplementary schemes are managed by separate organizations. Employees are required to contribute to them. This supplementary pension provides a pension in addition to the basic pension.

Depending on their status, employees contribute to:

· ARRCO: The Association for the Supplementary Pension Scheme for Employees, intended for non-executives and executives in the private sector;

· AGIRC: The General Association of Retirement Institutions for Executives, intended solely for executives in the private sector;

· IRCANTEC: The Supplementary Pension Institution for Non-Permanent Civil Servants and Local Authority Employees, for non-permanent employees in the public sector (contract workers, temporary workers, etc.).

They also operate on a pay-as-you-go basis, the only difference being in the calculation of the pension: while the basic schemes, with the exception of those for the liberal professions, operate on an annuity basis, the supplementary schemes operate on a points basis[2]. Each year, points are awarded based on the amount of contributions paid. At the time of retirement, the number of points accumulated is multiplied by the value of these points in euros.

Third pillar: collective or individual retirement savings

Basic and supplementary pensions can be supplemented by an additional pension. There are collective and individual savings plans that offer savers the opportunity to build up savings to compensate for the drop in income when they retire.

Conclusion

The issue of retirement, and in particular its financing, is a subject of concern for all French people. We are all aware that the pension system will not be able to guarantee the same level of pension payments as in the past. The viability of the pay-as-you-go pension system is being called into question: with the number of retirees on the rise and far fewer contributors, in addition to cyclical and structural reasons, the balance of such a system does not seem assured.

Supplementary pension contracts and products complement the basic and mandatory supplementary pension schemes, forming what is known as the third pillar of retirement: collective and individual retirement savings. A second article will attempt to briefly describe these supplementary retirement savings plans.

· Didier Le Menestrel, Damien Pelé, « Retraite, bâtissons notre avenir » (Retirement: building our future), Editions Cherche Midi, June 2015

· Technical Center for Provident Institutions (CTIP), « La retraite supplémentaire collective des salariés » (Supplementary collective retirement for employees), September 2013

· Ingrid Labuzan, « PERP or LIFE INSURANCE: which to choose for your savings? », Que choisir.com, January 2015

· Christian Bourreau, « The three pillars of retirement and the case of France, » Courriers des retraités, December 2012

· Franck von Lennep, « The replacement rate of salary by retirement income is decreasing over the generations, » DRESS, July 2015

· AFG « Association Française de la Gestion Financière » (French Financial Management Association), http://www.afg.asso.fr/index.php/fr/epargne-salariale/lepargne-au-sein-de-lentreprise

· La retraite en clair: information and news website on retirement, http://www.la-retraite-en-clair.fr/

· « The pay-as-you-go system is deteriorating, » Amundi 2016

· « The pension system in France: an overview, » Humanis

· « The different pension schemes, » Ministry of Social Affairs and Health

[1]An annuity is the right to receive a retirement pension that is acquired when you have contributed for a full year. Acquired rights are most often expressed in quarters. One annuity corresponds to four quarters of old-age insurance. Annuities are used by pension funds to calculate the amount of the retirement pension. This method of calculation contrasts with that of points-based schemes, which calculate the pension based on the number of points acquired each year in relation to the contributions paid. http://www.retraite.net/definition-annuite,l102.html

[2] Supplementary pension = sum of points awarded X value of the point on the date of retirement. The price of a pension point, known as the reference salary, varies according to the average salary of contributors to the Arrco and Agirc schemes in the previous year. Its evolution is decided each year by the social partners, representatives of employer and trade union organizations, and managers of supplementary pension schemes https://www.amundi-ee.com/entr/home_ret_pquoi_repde_sysfr

[1] Following the merger of Ipacte and Igrante. Ipacte (1949) was for non-tenured executives in the public sector, and Igrante (1960) was for non-tenured non-executives in the public sector.

[2] The « papy boom » refers to people from the baby boom generation who are now reaching retirement age.

[3] For the COR (Conseil d’Orientation des Retraites), the replacement rate is the ratio between the amount of the pension and the last income received from work. The net replacement rate takes into account pension amounts and salaries net of social security contributions (including CSG).

[4] Franck von Lennep, « The replacement rate of salary by retirement income is decreasing over the generations, » DRESS, July 2015

[1] In contrast, the capitalization system is based on the accumulation of capital according to savings possibilities and/or the desired level of benefits: workers contribute to build up capital to constitute a pension and entrust it to an organization that invests it in the financial markets until retirement age.

[2] Today, there are just over fifteen (when Social Security was created in 1945, there were more than a hundred).