Abstract :

· Biomass resources, although renewable, are limited. Priority is therefore given to food uses, with energy uses being the lowest priority.

· Biomass currently accounts for a very small share of the electricity sector, leaving significant room for growth in production in the coming years, as the costs of producing and integrating biomass are relatively low compared to its competitors, wind and solar power.

· Biofuel production in the transport sector has grown rapidly in recent years, but biofuels are still not very profitable compared to conventional fuels.

· The future of biomass in the French energy mix will depend on market conditions and pricing systems, which are currently inconsistent and difficult to interpret.

The bioeconomy has been the focus of considerable attention from public policymakers for the past decade, as it aims to respond to the new challenges posed by the depletion of fossil fuels, population growth, and the intensity of global warming. The development of the bioeconomy relies on the use of biomass as a raw material for the manufacture of a multitude of products (energy, chemicals, materials, and food). Biomass resources, while renewable, are limited and localized, which raises the major problem of prioritizing needs and managing conflicts of use. The aim of this article is not to answer this question, but rather to shed light on some of the economic and political issues surrounding the long-term use of biomass for various energy applications in France.

Biomass production: outlook and projections

Biomass includes all organic matter of plant or animal origin, the main sources of which are forests, crops, and waste. It is traditionally used for many purposes: food, materials (lumber, insulation); industry (paper, chipboard, etc.); textiles (cotton, wool, etc.), chemicals (latex, dyes, etc.) and energy (electricity, heating, biofuels)[1].

Biomass is often classified as a renewable material because it is produced through the continuous process of cultivation, harvesting, and replanting. In the ideal case, where we manage to maintain a balance between production and consumption, biomass is indeed a renewable material, with a renewal rate that can be measured in « years » for crops and « decades » or more for forests. However, with current population growth and future food and energy needs, it seems that we are currently far from being able to maintain a good balance. Biomass will therefore become non-renewable if wood is harvested faster than it grows (which is the case in several African regions), if large-scale deforestation takes place, and if soils become increasingly degraded or depleted.

By 2050, according to the 2012 report « Non-food uses of biomass, » there will theoretically be enough agricultural and forest biomass worldwide to meet food needs and contribute to energy needs. Nevertheless, biomass resources and uses appear to be inefficient and highly asymmetrical at the regional and subregional levels. This is the case, for example, in the so-called Southern countries, where the most productive biomass is found (thanks to a wide variety of plants) but where, by 2050, there will also be an additional two billion people to feed from land that will experience a sharp decline in productivity due to climate change. At the regional level, there will be an imbalance between available biomass and potentially higher demand in the coming decades. In France, although resource limits have not yet been reached thanks to the availability of land and water, soil fertility, and the protection of ecosystem services and ecosystems themselves, the notion of « prioritizing biomass needs » has emerged in public debate.

There is currently no multi-criteria analysis of usage hierarchies: with food as a priority, or maximization of added value, sustainability, efficiency, or security of supply? (Colonna et al., 2014). Let’s look, for example, at the « volume-value added » relationship of the production process in different sectors (Figure 1).

Figure 1. Volume-value added ratio of bioproducts

Source: Biocore

If we rank uses simply on the basis of maximizing added value, energy (biofuels, heat, and electricity) will be the least prioritized use, as it requires a large volume of biomass to produce relatively low added value. In France, for example, according to the notion of a « hierarchy » of uses set out by the Grenelle Environment Forum and the National Sustainable Development Strategy, energy is ranked last in order of priority: food/biofertilizers/materials/molecules/liquid fuels/gas/heat/electricity.

The place of biomass in the French energy mix

In 2014, renewable energies accounted for 9.4% of France’s final primary energy consumption (equivalent to 22.4 Mtoe out of a total of 256.5 Mtoe), including wood energy (39%) and biofuels (11.6%). As for electricity production, biomass accounts for a very small share (1.4%). Of the 18% share of renewable energies, biomass represents only 7.6% – or 7.5 TWh out of a total of 98.5 TWh of electricity production from renewable sources in 2014.

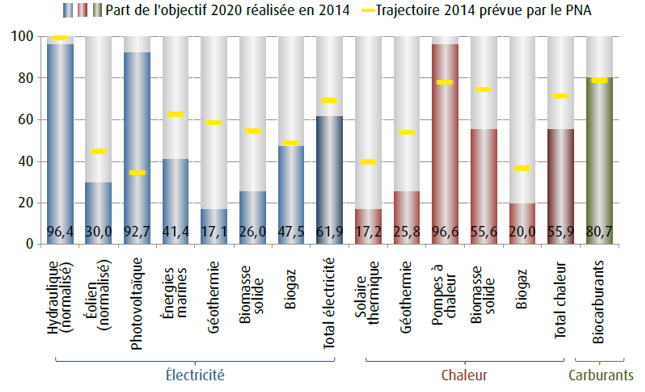

Directive 2009/28/EC sets France a target of 23% of energy produced from renewable sources in gross final energy consumption by 2020. France’s planned trajectory for achieving this target is set out in the National Action Plan (NAP) for renewable energy. If we look at the share of 2020 targets achieved in 2014 by sector (Figure 2), with the exception of photovoltaics and heat pumps, which slightly or significantly exceed the trajectory planned for 2014, all sectors are behind the trajectory set out in the NAP.

Figure 2. Share of 2020 targets achieved in 2014, by sector (in %)

Source: SOeS

The delay is significant for solid biomass in electricity and heat production: to achieve the planned target, biomass-based electricity production must be quadrupled and biomass-based heat production must be doubled by 2020. As for biofuels (biodiesel and bioethanol), there was a positive gap between actual production and the planned trajectory in 2014, and a further 705 Ktoe would be needed to achieve the target of 3,660 Ktoe set for 2020.

Between 2020 and 2050, the place of the biomass sector in the French energy mix will depend on market conditions, which are currently strongly influenced by French energy policy. The latter has long been marked by a desire to protect consumers from tensions in the energy world, which translates into a policy of price freezing, regardless of costs, market realities, and financing needs (for more details).

Biomass: the energy of the future?

It is difficult to predict whether biomass could be the energy of the future since, on the one hand, it is not primarily used for energy production (particularly for electricity and heat) and, on the other hand, the French pricing system (based on regulatory tools) is currently far from being a consistent and interpretable signal for manufacturers and consumers to make their investment or consumption choices.

Let us first look at the electricity sector, where the use of biomass in electricity production does not seem urgent. First, we would tend to give absolute priority to food uses of biomass. Secondly, among non-food uses, energy is not only a sector that produces the lowest added value while using a large volume of biomass compared to other sectors, but there are other renewable energy sources in the electricity sector with strong development potential and no conflict of use (e.g., photovoltaics or wind power).

Indeed, the French electricity system has an exceptional advantage thanks to its nuclear-based electricity balance (75%). Renewable energy currently accounts for around 18% of the electricity mix, with a large proportion (12.5%) coming from hydropower, which has almost reached its maximum capacity. Potential projects are systematically contested due to the conflicts of water use they generate or their impact on the environment (biological continuity, sediment transport, etc.). Development potential is shifting more towards photovoltaic, wind, and biomass energy. While there is room for growth in the production of these three sources, there are few reasons to believe that this potential will be realized without social (social acceptability issues), political (uncertainty, lack of interpretable signals) and economic constraints (imbalances between supply and demand, between real costs and prices).

The French electricity system today is characterized by overcapacity[1] thanks to the large capacity of its nuclear power plants. The 2014 energy transition bill sets a target of reducing the share of nuclear power in electricity production from 75% to 50% by 2025, but does not provide any trajectory for the evolution of electricity consumption. This leaves a great deal of ambiguity as to the feasibility of the target of increasing the share of renewable energies to 40% of electricity production.

Let us assume that the energy future we are building is based on a scenario of very low growth in electricity demand. The shift from 75% to 50% nuclear power would mean that an equivalent substitute of 88.5 TWh would have to be found in ten years (total electricity production from renewable sources was 31 TWh excluding hydroelectricity in 2014). This share, plus the decrease in the share of coal and gas, would have to be replaced by renewable energies, mainly solar, wind, and, as a last resort, biomass. This leaves a promising and ambitious potential for the biomass sector:

· Promising because , unlike solar and wind power, which are intermittent and unpredictable resources, biomass could be mobilized for regular and predictable electricity capacity: the cost of integration into the electricity system linked to grid management is relatively low. The cost of production is also estimated to be lower than other types of renewable energy: €56/MWh compared to €114/MWh for solar photovoltaic and €62/MWh for onshore wind power, according to the Court of Auditors’ estimate of the costs of the nuclear power sector (lowest levels).

· Ambitious because , despite the relatively low production and integration costs, the gap between actual costs and current politically blocked electricity tariffs could discourage any attempt to invest in this sector (see a previous article on this subject by clicking here).

In the transport sector, biomass is far from being the main use, but it is the one that has seen the most significant development in recent years. Biofuels (biodiesel and bioethanol) are the only green competitors to conventional fuels such as gasoline or diesel (excluding electric vehicles). Unlike the use of biomass in the electricity sector, which requires additional investment in infrastructure and the electricity transmission system, biofuels can be incorporated into conventional fuels without radically challenging current transport sectors and technologies, from production to distribution.

As for the long-term future of biofuels, assuming constant soil yields and technological innovation, the issue of biofuel production costs is a key factor. The production costs of bioethanol and biodiesel are currently too high for biofuels to compete with conventional fuels without active government support, with the exception of Brazilian industries based on sugarcane ethanol. For example, the additional cost of ethanol produced in Europe or the United States compared to gasoline is around 50 to 80%, and the additional cost of biodiesel compared to petroleum diesel is also significant, at around 30 to 75% (OECD-FAO 2008). The competitiveness of biofuels is largely dependent on the prices of fossil fuels, which are highly volatile, making it difficult to calculate the long-term economic profitability of biofuels. In theory, rising crude oil prices make biofuels more profitable, but when oil prices rise, biofuel production costs also increase, since ethanol production itself consumes energy due to the high level of mechanization in agriculture.

Conclusion

In recent years, non-food uses of biomass have received increasing attention. In the energy sector, its use is seen as a potential way to help reduce greenhouse gas emissions and dependence on fossil fuels.

While there is currently scope for developing electricity, heat, and biofuel production from biomass resources, numerous political and economic constraints make it difficult to exploit this potential. In this regard, it would be necessary for the energy pricing/tariff system to reflect market realities in order to provide a consistent and interpretable signal for investment or consumption in the years to come.

Reference

Colonna, P., Tayeb, J., & Valceschini, E. (2015). New uses for biomass. Le Déméter, 275-305.

The Commissioner-General for Sustainable Development, Key figures on renewable energies – 2015 edition

Mission report « Non-food uses of biomass, » Ministry of Ecology, Sustainable Development, and Energy, Ministry of Agriculture, Agri-Food, and Forestry, Ministry of Industrial Renewal, 2012.

[1]Total installed capacity in France in recent years was around 128 GW, while peak demand was around 102 GW.

[1]Biomass accounted for 90% of energy sources until 1800.