Usefulness of the article : this article outlines the main points of demographic transition and explains why it is likely to impact our pension system and the activities of life insurers in the coming years.

Summary:

- Demographic transition refers to the shift from a traditional system where fertility and mortality are high and roughly balanced, to a system where birth and death rates are low and also balanced[1].

- The advances in healthcare since the beginning of the industrial revolution have led to a demographic transition in developed countries, the consequences of which are extremely welcome but nevertheless pose financial challenges for the balance of pension systems and the balance sheets of life insurers.

- In France, the aging of the population resulting from the demographic transition poses problems for the balance of pension schemes. To remedy this imbalance, the government wants to encourage households to build up individual pensions, in addition to a pension reform that appears to be aimed at postponing retirement.

- The possible expansion of individual retirement products should increase the involvement of life insurers in pension management. The marketing of the PER may cause solvency problems for insurers if life expectancy increases substantially.

The industrial revolution that began in Europe at the end of the18th century gave rise to a large number of technical innovations that led to significant health and socio-economic progress. Overall, these advances have significantly improved human living conditions worldwide, giving rise to a phenomenon that research institutes specializing in population studies refer to as the « demographic transition. »

This demographic transition has had multiple consequences on the structure and evolution of the world’s population. These consequences include issues related to the distribution of food resources and land use. Beyond these issues, the implications of demographic transition also pose financial problems.

In developed countries such as France, they pose a threat to the financial stability of pension funds and, to a lesser extent, to the balance sheets of life insurers selling retirement savings products.

The aim of this article is first to characterize this demographic transition: what exactly are we talking about? What are the repercussions? The second part will explain why life insurers are more involved in this issue than any other financial institutions. Finally, thethird part will provide an overview of the potential impacts of demographic transition on the business of life insurers.

1. The demographic transition: what are we talking about?

According to INED[2], « demographic transition refers to the shift from a traditional system where fertility and mortality are high and roughly balanced, to a system where birth and death rates are low and also balanced. » Its theoretical model is often represented by the graph below.

It shows the pre-transition phase described by INED, with an annual birth and death rate of around 40 per 1,000 inhabitants, followed by a transition phase with high birth rates and a decline in mortality, ending with a phase known as « post-transition. » The latter characterizes the modern demographic regime in which developed countries currently find themselves, with annual birth and death rates below 10 per 1,000 inhabitants.

The demographic transition that began in the early19th century, at the time of the industrial revolution, is now complete in most countries around the world. In fact, it has been complete for over a century in some developed countries. Although it still provokes much debate in 2022, discussions in academic circles and the media focus more on the consequences of the transition than on the transition itself.

Indeed, the first notable consequence of the demographic transition is a considerable increase in the world’s population. The graph below shows that between 1950 and 2020, the number of people on Earth tripled and is expected to almost quadruple by 2050. This trend is also evident in France, although it is slightly more nuanced. The population has grown from around 40 million in 1950 to 65.5 million in 2022, an increase of more than 60%[5]. According to INED, it is expected to continue growing until 2050 and then stabilize.

The second major consequence of demographic transition is the aging of the population, which is particularly evident in developed countries where life expectancy has increased the most in recent decades, while the birth rate has continued to decline. In France, for example, the number of people aged over 65 rose from 4 million in 1950 to around 13 million in 2022 and is expected to reach 18 million in 2050[6]. This situation is often referred to as the « grandparent boom. »

These developments are not without consequences for economic activity and pose particular difficulties for the management of the French pay-as-you-go pension system. They also risk having potential repercussions on the activity of life insurers.

2. Impact of demographic transition on the French pension system

In France, the pension system implemented since 1945 is a pay-as-you-go system. It is based on the principle of intergenerational solidarity between working people who pay contributions and retirees who receive benefits. It contrasts with the funded pension system in Anglo-Saxon countries, where each person contributes individually to their pension.

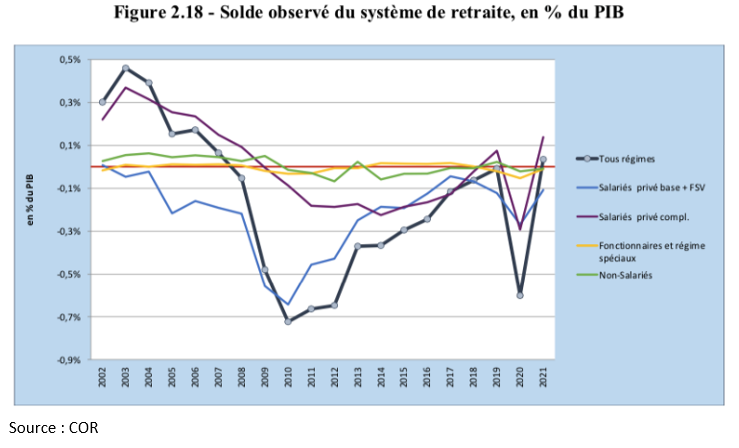

For several years now, the system has been in deficit, as shown in the graph below, taken from the latest report by the Pension Advisory Council (COR).

Since 2007, the system’s balance (all schemes included) has been in deficit, with a low point around 2010.

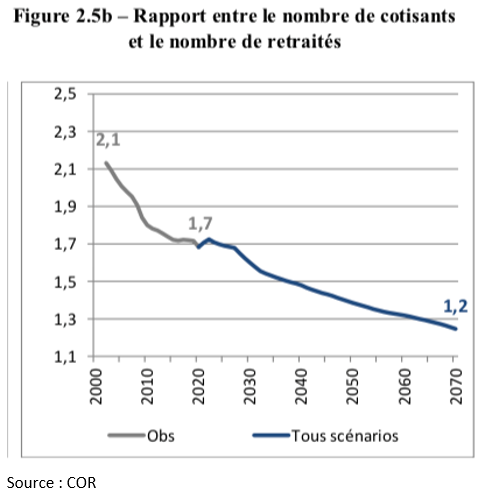

The origin of this deficit is mainly due to a structural factor, namely the aging of the population caused by demographic transition. In several of its recent reports, the COR has emphasized that, as a result of population aging, the ratio of contributors to retirees has fallen by 0.4 points in 20 years and is expected to fall by a similar amount between now and 2070. There will therefore be fewer and fewer contributors (people in work) to finance the benefits of retirees, who will be increasingly numerous.

In addition to this major structural factor, the economic climate has also contributed to increasing the deficit of the schemes. Indeed, in periods of economic tension, such as during the 2008 crisis or the 2020 crisis (linked to COVID-19), the unemployment rate rose sharply, which logically led to a decrease in the number of people in work. During these periods, there were therefore fewer contributors for the same number of retirees, all other things being equal. As a result, the benefits to be paid remained stable, but the contributions used to finance them decreased, which automatically increased the deficit.

In an attempt to curb the structural problem of the deficit, several corrective reforms were carried out between the late 1980s and the early 2000s. These reforms notably made it possible to index retirement pensions to prices instead of wages, as had previously been the case. As wages generally rise faster than prices, these reforms ultimately paid off for the schemes, as they mitigated the increase in pensions over the years, which in turn gradually reduced the deficit. As a result, in 2021, the schemes returned to a positive balance with a surplus of €900 million, and the COR even forecasts a surplus of €3.2 billion by the end of 2022. Nevertheless, the longer-term outlook remains much less optimistic, with the advisory board forecasting a deficit of between 0.5 and 0.8 percentage points of GDP between 2022 and 2032.

To avert this new threat, the current government wants to carry out a reform whose main objective is to raise the retirement age in order to increase the number of contributors. According to the COR’s latest report, this reform could help maintain stable spending and offset the effects of an aging population.

In addition to this reform, the government also wants to encourage workers to contribute individually (through capitalization) to their retirement in order to gradually reduce households’ dependence on the pay-as-you-go pension system. While life insurance has been the savings product of choice for the French for several decades, individual retirement products are « much less popular. »

At the end of 2019, assets held in life insurance products amounted to more than €1.7 trillion, while assets held in retirement products amounted to around €240 billion. In order to attract more savers to individual retirement products, the government has therefore created, as part of the PACTE law, a new product called the PER (Retirement Savings Plan), which has been marketed by French life insurers since the end of 2019. A detailed description of this new product is beyond the scope of this article, but it is worth noting that it offers greater flexibility than previous retirement products (PERP, PERCO, Article 83, Madelin contracts), making it more attractive.

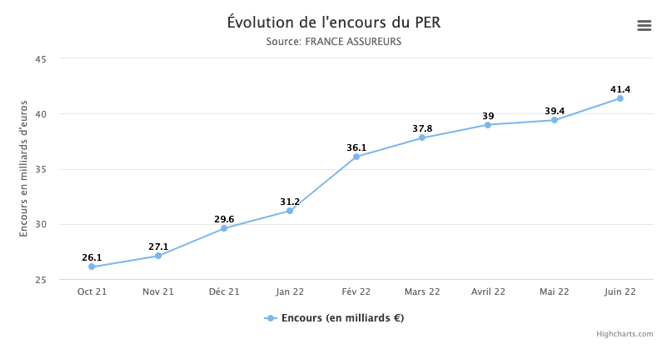

In mid-2022, the attractiveness of this product seems to be confirmed if we look at the evolution of outstanding amounts in the graph below.

By creating this new retirement product, the government intends to implicitly transfer part of the longevity risk[8] that weighs on the current retirement system to life insurers. Indeed, if the product is as successful as expected, the role of insurers in managing household pensions should be strengthened. The outstanding amounts of retirement products managed on their balance sheets should increase, along with the risks and opportunities that this entails. It would therefore be relevant to consider the potential impact of this new market on their activities.

3. What are the risks associated with the new PER for life insurers?

The PER was launched on October1, 2019 by French life insurers. Unlike pay-as-you-go pensions, it is a funded pension product. Its fundamental principles are the same as those of older pension products (PERP and others) that are no longer available. Policyholders make individual contributions throughout their lives, in amounts and at frequencies that they can define[9]: insurers refer to this as the « accumulation phase. » Once they reach retirement age, they can choose between a lump sum payment, where all the accumulated capital is returned by the insurer at the time of retirement, and an annuity, where the insurer pays the insured a monthly annuity (for example) until the end of their life; this is the « payout phase. »

Although such a pension system does not, in principle, pose any problems in terms of public finance management, it can nevertheless give rise to certain financial risks for the accounts of the managing bodies, particularly if the life expectancy of the insured increases more than anticipated.

In order to determine the amount of pensions they will have to pay to their insured persons in the future, life insurers use « mortality tables. » These tables are regulated in France, and insurers are required to use them to calculate their rates and provisions. They are compiled by INSEE (the French National Institute for Statistics and Economic Studies) on the basis of past demographic observations and forward-looking estimates[10]. If the life expectancy derived from these mortality tables proves to be lower than that actually observed in the future, life insurers may encounter certain financial difficulties.

The main difficulty is that their solvency will deteriorate. If this hypothesis proves to be true, insurers will have set aside less in their balance sheets than they will have to pay out to policyholders. Their margins may therefore erode or even result in losses on contracts. These losses will be directly absorbed by equity capital, which, all other things being equal, would have a negative impact on their solvency ratio and, in extreme cases, could even lead to bankruptcy or the withdrawal of their license. To avoid this problematic situation, European regulations have strengthened the capital requirements that insurers must meet in order to operate, so that they can cope with potential risks, such as the longevity of policyholders.

The second difficulty that could arise from an error in estimating life expectancy in mortality tables would be to see the balance sheets of certain insurers in a situation of « under-matching. » Unlike solvency risk, this risk is linked to changes in the calibration of benefits to be paid and not to increases in those benefits, which makes it less problematic. In order to manage their balance sheets, insurers use a technique commonly known as « cash flow matching. » To implement this technique, the insurer attempts to invest the funds collected in such a way as to match the cash inflows from investments with the cash outflows related to commitments to policyholders.

However, the potential extension of insurers’ commitments due to the aging population (or increase in life expectancy) implies a potential outflow of cash flows over a longer period. If the horizon for cash outflows lengthens, insurers will begin to encounter difficulties in finding financial products on the market that allow them to adequately match their assets and liabilities. Most of the money collected through retirement (or savings) products is invested in French debt, which has a duration[11] of around seven years. If life expectancy continues to increase in the coming years, this problem of « asset-liability matching » is likely to become much more acute. Funds will therefore be invested in maturities that are far too short in relation to the horizon of their commitments.

However, this risk must be put into perspective. Firstly, life insurers have become familiar with it in recent years, as it already existed for life insurance products and PERPs[12].

Secondly, this risk does not materialize in the event of a lump-sum withdrawal, which is an option offered by the PER and was not included in the range of older products. If the insured chooses this option, the entire capital acquired is returned to them upon retirement. In this case, there is therefore no issue related to life expectancy.

Finally, it should also be noted that more specific solutions exist to manage this type of risk. The insurer may, for example, call on a reinsurer. They will then have to pay a premium to the reinsurer, who will cover part of any claims that become too large. The insurer may also turn to the financial markets. In recent years, risk management specialists have developed market solutions to enable insurers to manage longevity risk. For example, they may enter into swap contracts or use securitization.

The aging population therefore poses a risk for life insurers, but this risk appears to be fairly well managed today, given the existing management mechanisms and the knowledge of market players on the subject.

Conclusion

The demographic transition that is causing the aging of the population in France is creating financial difficulties for the government in managing a deficit-ridden pay-as-you-go pension system. The new PER was created to encourage households to contribute individually to their retirement savings with the help of their insurance companies. This situation is a game changer for insurers and increases their involvement in managing household retirement savings. While this new situation does involve risks, insurers have already identified them and appear to have solutions in place to address them.

It is also important to remember that the marketing of the new PER is not only a source of threats for insurers, but also a source of commercial opportunities and new profit centers that will undoubtedly offset the risks associated with an aging population.

References:

Data on demographic transition:

Figures on retirement savings:

https://cleerly.fr/per/chiffres-cles

Publication on longevity risk:

https://www.cairn.info/revue-d-economie-financiere-2017-2-page-107.htm

Coverage of longevity risk:

COR Annual Policy Report:

https://www.cor-retraites.fr/index.php/node/595

Information on the PACTE law:

https://www.economie.gouv.fr/loi-pacte-croissance-transformation-entreprises#

[1] Source: National Institute for Demographic Studies (INED)

[2] National Institute for Demographic Studies.

[3] Several researchers estimate that the demographic transition was completed in 1926 in the United States, in 1910 in the United Kingdom, and more recently, in 1980 in Bangladesh.

[4] Metropolitan France

[5] Figure to be qualified due to the numerous migratory flows during this period

[6] Source: INED

[7] Sources: FFA, Cercle de l’épargne

[8] Risk linked to population aging.

[9] Only in the context of individual retirement savings plans.

[10] For life annuity transactions, insurers are required to use the TGH-TGF 05 tables.

[11] Or average maturity

[12] However, the problem is less serious for life insurance, as customers can surrender their policies at any time, which reduces the duration of liabilities.

[13] A longevity swap is an exchange of cash flows between two parties. One party pays a cash flow based on a fixed mortality rate and receives a cash flow based on a variable mortality rate, and vice versa for the other party. The first party is therefore covered if the mortality rate of its portfolio increases unexpectedly.

[14] Securitization allows longevity risk to be transferred to investors through the issuance of financial securities on the markets (often bonds).