Usefulness of the article: Copper, a strategic mineral that has been used for thousands of years, will become essential in the context of the ecological and digital transition. Strong growth in demand will change the current map of producers, raising fears of supply shortages for industries that use this resource. This study analyzes the issues that this strategic mineral will face.

Summary:

- Copper production is highly uneven, with Chile clearly leading the way among producing countries.

- Copper has a wide range of applications, in both cyclical industries and industries with low variation.

- Global production is rising sharply, particularly due to the ecological transition, which requires large quantities of ore for certain technologies.

- Global demand is also expected to increase sharply, with a risk of ore shortages by 2055.

- However, new discoveries of resources could redefine global production.

With approximately 2.1 billion tons in proven reserves, copper is a metal in high demand by various industries. While the majority of demand comes from China, new economic sectors such as soft mobility will consume more in the coming years. The importance of this mineral will therefore be confirmed by the ecological transition, to such an extent that some experts estimate that resources could run out by 2055. However, new discoveries are likely to change the current production landscape, with potentially significant deposits in Central Asia, an area that has yet to be extensively explored.

1. Production concentrated in a few countries with demand coming mainly from China

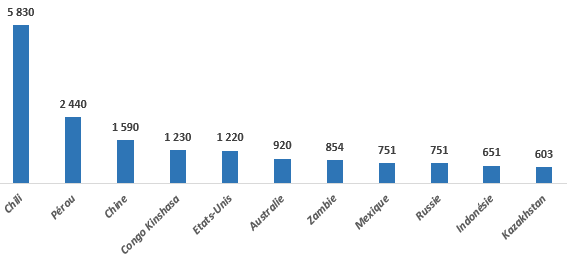

With production of 20.4 million tons in 2018, copper is considered a strategic metal by manycountries, given its crucial importance to certain industries.

Ore extraction is very unevenly distributed across the globe, with Chile alone accounting for around 28% of global production (followed by Peru with 12% of production). China, while controlling a large part of ore refining activities (38.5% of global refining in 2018), ranks third in terms of extraction.

Top 10 Copper Producers in the World in 2018 (in thousands of tons)

Source: United States Geological Survey

Chile, in addition to having the highest production in the world, has proven reserves estimated at 200 million tons, or more than 30 years of production at the current rate (Peru and Australia come next with 87 million tons each in proven reserves). However, this production could be affected in the coming years, as copper ore requires large amounts of water to be refined. The Chilean authorities have announced that the mining industry will see its water extraction permits restricted, particularly in regions of the country subject to severe water stress. To overcome this constraint, the industry plans to use seawater to meet growing demand, with a 290% increase in seawater use expected between 2016 and 2028.

This adaptation will be essential, given that in 2019, copper accounted for 10% of the country’s GDP, 7.8% of its tax revenue, and 9.8% of national employment (approximately 800,000 direct and indirect jobs). Taking into account the entire copper value chain (i.e., from raw copper extracted from a mine to refined copper), it accounts for 45% of the country’s exports.

Chile’s economic health therefore depends, in part, on its copper exports. Demand for this mineral is driven by consumption in emerging countries, particularly China, which alone consumes around 50% of global production (compared to 22% in 2008) to meet its enormous need for raw materials to support its industrial boom. The country produced around 1.6 million tons in 2019, but this quantity remains insufficient, forcing it to import the shortfall (more than 8 million tons/year).

To curb these massive imports, China has been focusing on ore recycling for more than 10 years in order to be less dependent on other producing countries. In 2017, China purchased more than half of the world’s copper waste, but China’s share of this trade has been declining for the past decade, particularly with the increase in waste recycling and ore processing capacity in the country. Driven by the country’s economic development, Chinese imports of copper scrap more than doubled between 2000 and 2008, peaking at 5.6 Mt before the global financial crisis, but have been declining steadily since then. In 2018, 2.4 Mt of copper waste entered the Chinese market, a 32% drop compared to 2017, and approximately 1.5 Mt in 2019, a 58% drop compared to 2017. Chinese imports of copper scrap also declined following the Chinese government’s announcement in August 2018 that it would impose a 25% tax on scrap imports from the United States. This decision was made in the context of the trade war between the two countries.

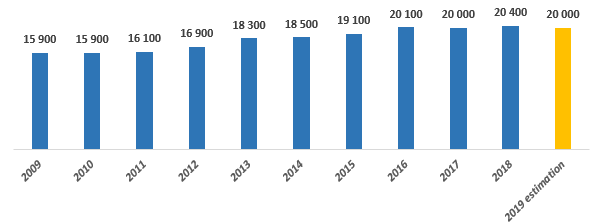

To meet the growing global demand for copper, production has increased by more than 20% in 10 years.

Global copper production between 2008 and 2019 (in thousands of tons)

Source: United States Geological Survey

However, the factors determining copper demand are set to change in the coming years, with demand no longer driven solely by massive industrial growth but also by the ecological transition, which will require significant quantities of copper, particularly for the transport sector.

2. A mineral that will become increasingly important with the ecological transition

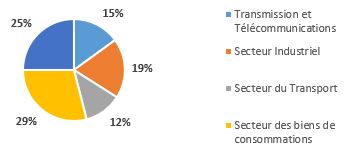

To date, 29% of global copper consumption comes from the « consumer goods » sector (household appliances, air conditioning and refrigeration equipment, industrial and commercial electronics, and IT). In second place is the construction sector (with 25% of consumption), which is mainly dependent on the Chinese market, the largest in the world.

Copper consumption by industry (in 2015)

Sources: International Wrought Copper Council and International Copper Association

It is also possible that future demand drivers will be geographical, with a decline in demand in China, particularly due to the slowdown in its economic growth over the last ten years. In 2019, 51% of copper was used by China, followed by the rest of Asia (19%), Europe (17%, led by Germany), the Americas (12%), and Africa and Oceania (1%). Strong economic growth in Africa and Southeast Asia is expected to change the current configuration.

As part of the ecological transition, the transport sector will require larger quantities of copper, particularly with the rise of electric mobility. Indeed, it takes around 80 kg of copper to build a battery-powered electric vehicle[1], compared with around 23 kg for a standard combustion engine vehicle. In fact, Wood Mackenzie, a British consulting firm specializing in the commodities sector, predicts that copper demand for transportation will increase by 7.5 million tons by 2040.

It is difficult to accurately estimate copper requirements for each sector between now and 2050. However, the French Institute of Petroleum and New Energies (IFPEN) and the Institute for International and Strategic Relations (IRIS) jointly launched the GENERATE project in 2019, which aims to estimate future copper requirements based on two scenarios: global warming of 2°C and global warming of 4°C. The conclusions are clear: both scenarios will require the discovery of new deposits in order to meet rapidly growing demand, mainly driven by the transportation sector. A 2°C rise would require a 2.55-fold increase in known global reserves in 2017, and a 2.2-fold increase for a 4°C rise. This will require a significant effort in exploration to identify new resources, otherwise the resource will run out by 2055.

To date, 44% of the global exploration budget is allocated to South America, followed by Africa (12%), the United States (10%), Australia (9%), Southeast Asia/Pacific countries (5%), and Canada (4%). This active exploration remains focused on countries that already have significant reserves and wish to further develop them. To meet the high demand caused by global warming, it will be necessary to direct investment towards new regions, particularly Central Asia, which remains a largely unexplored region.

3. Prospecting will increase in response to pressure on resources combined with waste recovery

The United States Geological Survey estimates the world’s potential copper reserves at 3.5 billion tons (including technically and economically exploitable land and sea resources). Central Asia is believed to hold 14% of these resources, with Kazakhstan alone accounting for around 5% (the country produced around 603,000 tons in 2018). A mining project is currently under development in Afghanistan, with production scheduled to start in 2022 and reserves estimated at 11,000 tons.

In addition to Central Asia, two countries in South and Central America are planning to develop their mining industry:

- Colombia, whose precisely exploitable quantities are still unknown, wants to develop its resources and increase its current small production of 10 kT per year.

- Panama, which is expected to produce 375,000 tons by 2023, compared to current production of around 175,000 tons. Production will eventually account for 4% of the country’s GDP.

It is difficult to accurately identify all the countries that have implemented mining policies aimed at exploiting copper ore. An alternative solution is to focus on recycling the resource, which can be recycled indefinitely without any loss of performance or properties.

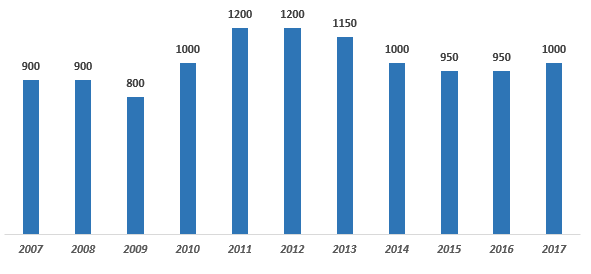

Recycled copper meets 33% of global demand, with around 9.7 million tons in 2018. The United States is the world’s leading producer and exporter of copper waste, with 1 million tons exported in 2017. The main destination for these exports is China, which alone accounts for 72% of US exports. The rest is shipped mainly to Canada, Germany, and South Korea.

US exports of copper scrap (in kT)

Sources: US International Trade Commission and BRGM Copper Report 2019

With China’s current copper recovery rate at 60%, US exports are expected to be less focused on China over the next 10 years.

It is highly likely that industrialized countries will develop copper ore recycling in order to be less dependent on imports. China has opted for tax incentives, such as a reduction in VAT, for companies using recycled copper. Ultimately, improvements in recycling technologies, public policies put in place to encourage the circular economy, and strong demand for copper should help to structure the recycling market.

Conclusion

Demand for copper will increase significantly, regardless of the various scenarios predicted for global warming. Changes in the determinants of demand will have a profound impact on the future ore market. New clean and electric mobility solutions will consume more copper, which will certainly require the recycling market to be organized in order to meet the increase in demand. The United States has a strong capacity for action as the leading producer of recycled copper. China is actively developing its domestic market against the backdrop of a trade war with the United States. Indeed, new discoveries of deposits may not be sufficient, and the resource could run out by 2055.

Bibliography

Bureau of Geological and Mineral Resources (BRGM), Final Report, Copper: review of global supply in 2019; http://infoterre.brgm.fr/rapports//RP-69037-FR.pdf

Mineral Info, Global trade in copper and aluminum scrap has been transformed by Chinese environmental measures and Sino-American trade tensions: http://www.mineralinfo.fr/ecomine/commerce-mondial-dechets-cuivre-daluminium-ete-transforme-mesures-environnementales

Les Yeux du Monde, Copper: Peru’s new gold: https://les-yeux-du-monde.fr/actualite/amerique/32341-le-cuivre-nouvel-or-du-perou

Invest in Wallonia, Chile: a key country for strategic minerals: https://www.awex-export.be/fr/medias/le-chili-pays-cle-pour-les-minerais-strategiques#_ftn1

The Conversation, Copper: what future for this metal that is essential to the energy transition? : https://theconversation.com/cuivre-quel-avenir-pour-ce-metal-essentiel-a-la-transition-energetique-119500

La Tribune des Métaux, Non-Ferrous Metals: China is recovering, copper prices are soaring: https://www.tribune-des-metaux.fr/non-ferreux-la-chine-se-releve-le-cuivre-s-envole.html

COMES, Factors determining metal prices, using copper and vanadium as examples: http://www.mineralinfo.fr/sites/default/files/upload/4_brgm-fondamentauxcu_v_finale_20190529.pdf

United States Geological Survey, Copper Statistics and Information: https://www.usgs.gov/centers/nmic/copper-statistics-and-information

[1] Seat reports that manufacturing an electric vehicle requires an average of 40 kg of copper for the battery, 10 kg for the motor, 20 kg for low-voltage wiring, 5 kg for high-voltage wiring, and more than 5 kg for other parts.

[2] A 4°C warming would require fewer copper resources due to more drastic changes in transportation.