On December 12, 2014, FitchRatings decided to downgrade France’s sovereign rating from AA+ to AA, with a stable outlook.

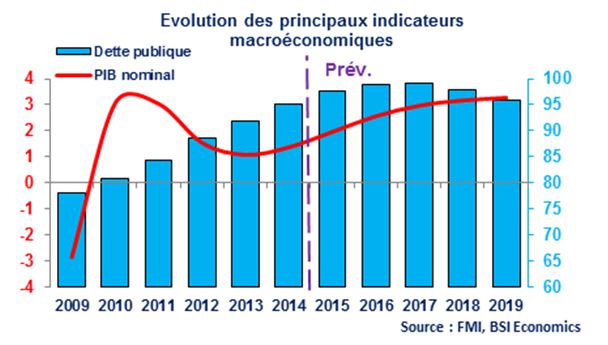

The lack of significant improvement in public finances since the fall of 2014 and the presentation of the 2015 budget prompted FitchRatings to downgrade France’s sovereign rating by one notch to AA. Despite additional budget announcements (€3.6 billion, or 0.2% of GDP), the deficit forecast for 2015 is expected to be 4.1% of GDP, similar to the 2013 level. As such, Fitch does not rule out the possibility that the European Commission will impose a fine on France (0.2% of GDP) in spring 2015, during the country’s next budget review. Thus, in a context of weak nominal growth, public debt is expected to peak at nearly 100% of GDP in 2017 before beginning a gradual decline.

Furthermore, the agency is concerned about the short-, medium- and long-term growth outlook. First, in the short and medium term, only the depreciation of the euro and the fall in oil prices will drive economic activity. Consumption will remain subdued by high unemployment, at 10.5%. Then, in the long term, the impact of reforms is considered insufficient to restore competitiveness and stimulate potential growth, estimated by FitchRatings at 1.5% per year. Furthermore, the agency questions the government’s ability to implement all the structural reforms that would unleash growth. In addition, the postponement of budgetary targets jeopardizes France’s credibility in terms of public finances.

However, the agency highlights certain positive aspects to justify the stable outlook accompanying France’s rating: i) access to financial markets, which guarantees low interest rates and sound debt management (average debt maturity of 7 years), ii) the government’s multiple announcements regarding the continuation of economic, territorial, and social reforms, iii) the good financial health of private agents, both households (low debt and high savings) and banks, as evidenced by the positive results of the fall 2014 bank stress test, iv) the strengthening of the European governance framework, which limits the risk of direct contribution by the French state.

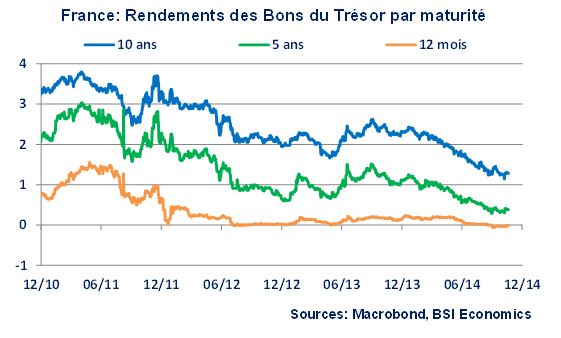

As expected, the markets did not react to this announcement, as French sovereign rates remained stable at historically low levels. Today, France is a prime example of the lack of reaction following a downgrade of sovereign issuers. This decorrelation, or even negative correlation, can be explained by the massive liquidity available on the markets, the potential future purchase of sovereign debt by the ECB, and France’s credit rating, which remains highly prized by investors.

In addition, it should be noted that FitchRatings, like other agencies, is much more pessimistic about the impact of the Responsibility Pact than the OECD. As a reminder, the OECD estimated the effects of all the reforms undertaken by the government (Responsibility and Solidarity Pact and reduction in labor costs via the CICE, labor market reform, competition via the Macron law, territorial reform) at +0.3 percentage points of growth over five years and +0.4 percentage points over ten years. FitchRatings’ interpretation shows the lack of certainty surrounding the reform package. However, while the agency is being realistic in its projections, it seems reasonable to assume that the scenario put forward by the government, and supported by the OECD, would enable France to meet its main challenges, which are to stimulate growth (by restoring competitiveness and creating jobs) in order to reduce the burden of public debt in the long term.